Shares of Microsoft (NASDAQ:MSFT | MSFT Price Prediction) are down roughly 4% in Thursday afternoon trading, sliding to $415 from a prior close of $432.92. It’s the software giant’s worst session since early February, and the selloff is tied directly to a corporate first.

Microsoft is launching the first-ever voluntary employee buyout program in its 51-year history, offering exit packages to roughly 7% of its U.S. workforce. The news lands as the company is also pushing capital expenditures to unprecedented levels to build out Azure AI infrastructure.

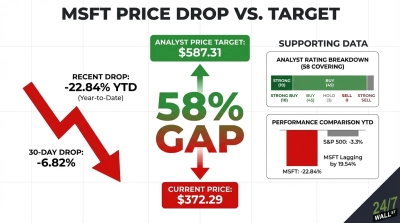

The stock is now down about 14% year to date, sharply underperforming the S&P 500. Investors are wrestling with whether Microsoft’s massive AI bet will pay off fast enough to justify the spending intensity.

A Historic Buyout Program at Microsoft

The buyout targets U.S. employees at the senior director level and below whose age plus years of service total 70 or more. Workers on sales incentive plans aren’t eligible, and Microsoft says eligible staff and their managers will get full details on May 7.

Amy Coleman, Microsoft’s chief people officer, framed the program as giving eligible employees “the choice to take that next step on their own terms, with generous company support.” The company is also loosening how managers reward staff, no longer requiring stock to be tied directly to cash bonuses.

This move doesn’t exist in a vacuum. Microsoft already eliminated more than 15,000 positions globally across multiple layoff rounds in 2025, and today’s program signals that the workforce reshaping is still in motion.

The $110 Billion AI Capex Backdrop

Microsoft’s spending on data centers, GPUs, servers, and networking gear has exploded. Capital expenditures hit $37.5 billion in fiscal Q2 (ended December 2025), a jump of roughly 66% year over year, and the company is on pace for $110 billion to $120 billion in total capex for fiscal year 2026.

That spend is feeding an Azure business still growing fast. Azure revenue climbed 39% year over year in Q2 FY2026, and Microsoft’s commercial remaining performance obligation ballooned to $625 billion, up 110% year over year. Microsoft Cloud crossed $51.5 billion in a single quarter for the first time.

CEO Satya Nadella has been blunt about the trajectory, telling investors Microsoft has “built an AI business that is larger than some of our biggest franchises.” The buyout, in this light, looks like a deliberate reshaping of the cost base to match the new AI-first operating model.

The Bull Case and the Bear Case

The bull case is straightforward: AI tools are starting to reshape knowledge work inside Microsoft itself, and a leaner, more flexible workforce could juice operating margins already sitting at a stout 47%. Analyst sentiment remains firmly constructive, with 55 Buy or Strong Buy ratings against just 3 Holds and zero Sell ratings, and a consensus target of $579.57.

The bear case is about timing. Investors are increasingly worried that Microsoft’s AI capex is running ahead of measurable productivity gains, and that today’s buyout is a tell that management sees margin pressure ahead. On Stocktwits, retail sentiment has shifted from “bullish” to “neutral” over the past 24 hours, a cooling that matches the broader caution across enterprise software names.

The prediction markets echo the short-term skepticism. Polymarket traders are pricing in a 100% probability of a down day for MSFT stock on April 23, even as they hold a 94% probability that Microsoft beats its upcoming quarterly earnings.

What to Watch Next

The next likely catalyst will arrive soon. Microsoft reports its Q3 FY2026 results on April 29, and the commentary on Azure growth, capex pacing, and any color on headcount plans will matter far more than the headline EPS beat. For more on how Big Tech is rethinking labor alongside AI spend, see our recent coverage of the AI capex cycle.

For retail investors, the framework is simple. If the thesis is that AI demand keeps scaling faster than costs, pullbacks like today’s can look like opportunities to accumulate at a forward P/E ratio of 22x. When the worry is that capex intensity is outrunning returns, it makes sense to wait for next week’s earnings call before adding exposure.

Either way, watch for whether Microsoft’s management frames the buyout as a one-time reset or the start of a longer-running efficiency drive. That distinction could define MSFT stock’s next leg.