Shares of Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) are down roughly 7% in Thursday afternoon trading, changing hands near $142 after starting the session at $152.62. The slide comes despite a fresh $300 million contract with the U.S. Department of Agriculture and a new Buy initiation from DZ Bank.

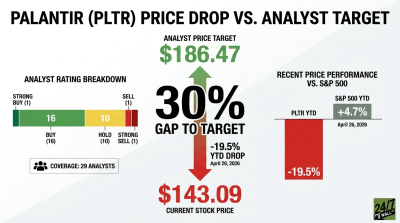

The pullback is striking given the backdrop. Palantir’s year-to-date performance now sits at -14%, even as the stock remains up 62% over the last 12 months. Retail traders are weighing whether today’s dip is a gift or a warning.

The broader tape offers little cover. The major U.S. market indexes are down less than 1%, so this is a stock-specific and sector-specific move tied to enterprise software weakness rather than any macro shock.

The USDA Win and DZ Bank’s Bullish Call

Palantir’s $300 million USDA agreement covers modernization of farm operations and extends the company’s already dominant federal footprint. It builds on a Q4 segment where U.S. government revenue grew 66% year over year to $570 million.

DZ Bank initiated coverage today with a Buy rating and a $175 price target, flagging Palantir’s growth trajectory while acknowledging rich valuation. That target sits below the broader analyst consensus target of $186.47, yet still implies meaningful upside from current levels.

Institutional flows are also mixed on PLTR. M&T Bank boosted its stake by 88% in the latest quarter, while insiders offloaded over 1 million shares worth roughly $137.7 million in the last 90 days.

ServiceNow’s Plunge Drags Enterprise Software Lower

The real pressure on Palantir appears to be sympathy selling. ServiceNow (NYSE:NOW) stock is crashing 17% today after the company’s Q4 2025 print beat on revenue at $3.57 billion and EPS at $0.92, yet shares were punished on mix-shift guidance concerns.

Reddit’s r/stocks is flooded with posts like “NOW beats revenue and in line with EPS but drops 15% after earnings”. Traders are openly asking whether today “triggers another wave of the SaaSpocalypse” across enterprise AI names. For more on today’s broader tape, see our coverage of the recent SPY and QQQ rally to new highs.

Bull Case vs. Bear Case for Palantir

The bull case remains intact on paper. Palantir’s Q4 Rule of 40 score hit 127%, revenue grew 70% year over year to $1.406 billion, and FY2026 guidance calls for 61% revenue growth. CEO Alex Karp calls Palantir “an n of 1” in scaling operational leverage from AI.

The bear case is just as clean. PLTR stock trades at a P/E ratio of 242x, insider selling has accelerated, and today’s sector revaluation shows how quickly rich-multiple names can reset. Polymarket is currently assigning a 99% probability that PLTR closes lower today.

What to Watch Into the Close

The prediction markets tell a split story. Polymarket’s week-ending contract assigns an 88% probability that PLTR stock finishes the week above $137, which implies limited additional downside if enterprise software stabilizes. An internal AI model target of $155.36 points to modest recovery potential.

For retail investors weighing the dip in Palantir, the framework is straightforward. Watch for whether shares defend the $140 level into the close, and whether the next round of enterprise software earnings stabilizes the sector. If the commodity cognition thesis and government AI spending look like multi-year tailwinds, this pullback fits a scale-in-slowly playbook at a moderate position size.

On the other hand, if SaaS multiples still have room to compress alongside names like ServiceNow, waiting for clearer evidence of sector stabilization could be the more disciplined call. Palantir’s next earnings print will likely be the decisive catalyst.