The SPDR Bloomberg High Yield Bond ETF (NYSEARCA:JNK | JNK Price Prediction) has become a common stop for income investors looking beyond Treasuries, pairing a forward yield near 6.5% with monthly distributions. This article evaluates whether that payout is durable heading into a 2026 credit cycle where narrowing spreads and rising default expectations are pulling in opposite directions.

How JNK Actually Pays You

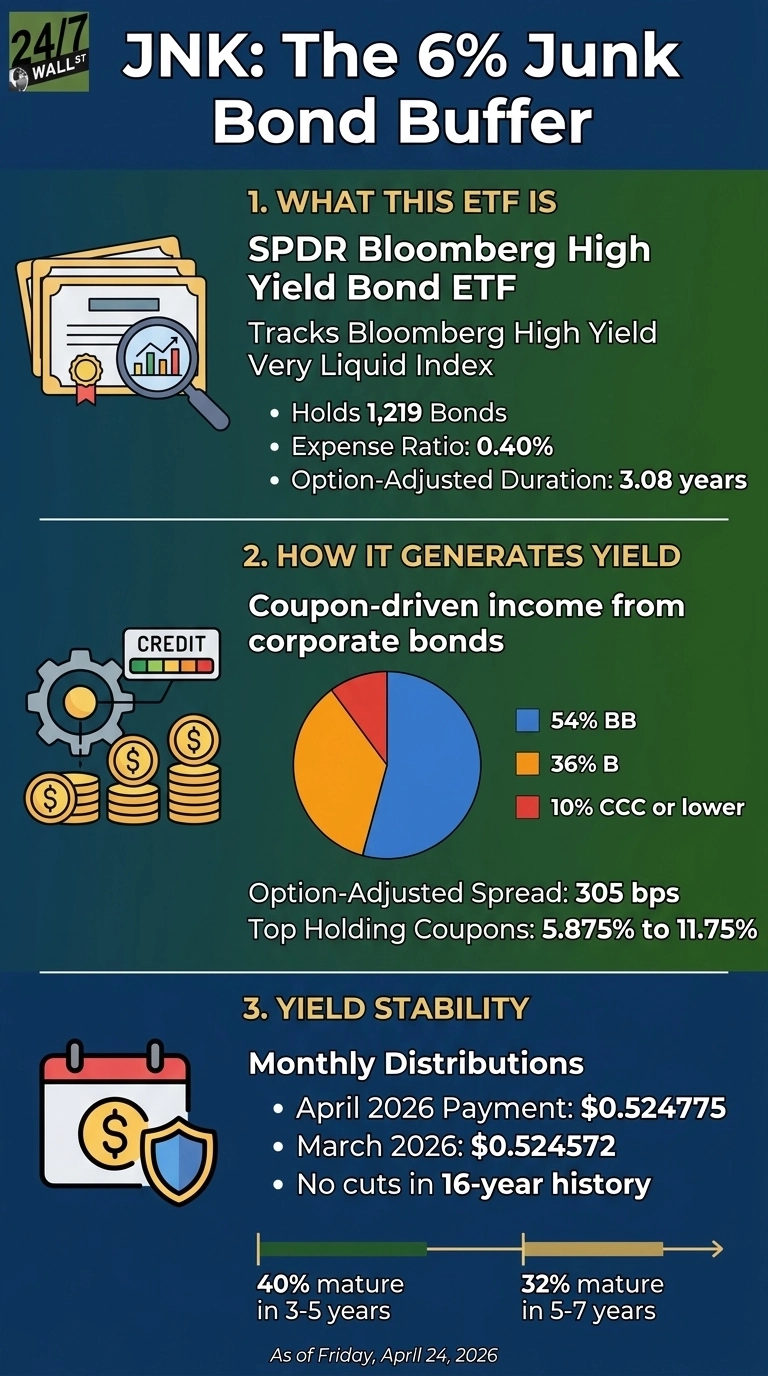

JNK tracks the Bloomberg High Yield Very Liquid Index, holding 1,219 bonds at an expense ratio of 0.40%. The income is purely coupon-driven: investors collect interest payments from below-investment-grade corporate issuers, net of fees. There are no options overlay, no leverage, and no derivative engineering. Corporate bonds make up roughly 100% of the portfolio, with coupon rates in the top holdings ranging from 5.875% to 11.75%.

Monthly payouts have remained within a tight band, with the April 2026 distribution at $0.52478 per share, following $0.524572 in March and $0.560093 in February. Regular monthly payments across 2025 ranged from $0.527 to $0.539, and there were no cuts in the 16-year history.

Credit Quality and the Spread Cushion

The rating ladder is where dividend safety lives for a bond ETF. JNK’s quality mix breaks down as 54% BB, 36% B, and 10% CCC or lower, with essentially no investment-grade exposure. The fund’s option-adjusted spread is 305 basis points and option-adjusted duration is 3.08 years, a relatively short profile that limits rate sensitivity.

With the 10-year Treasury at 4.3% and the Fed Funds upper bound near 4% after 75 basis points of cuts since October 2025, lower refinancing costs favor weaker issuers. The 10Y-2Y spread at 0.51% remains positive, removing the immediate recession flag.

Where the Risk Really Sits

Sector concentration is the pressure point. JNK carries 16% in Consumer Cyclical, 14% in Communications, and 14% in Energy, with over 40% in cyclical sectors overall. Individual issuers include EchoStar, DISH Network, and WULF Compute. The refinancing window is narrow: 40% of bonds mature in 3 to 5 years and 32% in 5 to 7 years, concentrating rollover risk into 2029 to 2032.

Corporate fundamentals are supportive for now, as Total corporate profits reached $4,352.1 billion in 2025Q4, up 9.6% year over year. The cracks show up in specific sectors: Transportation profits fell 22% year over year, and Wholesale fell 22% year over year, both of which overlap with JNK’s cyclical exposure. Market consensus anticipates rising default rates in 2026, and the VIX spike to 31.05 on March 27, 2026, already produced one test of spread resilience before normalizing to 19.31.

Total Return Reality

Price performance has cooperated. JNK trades at $96.92 against a 52-week range of $94.19 to $98.24, with a one-year total return of about 10% and a YTD gain near 1%. That YTD figure beats the high-yield category’s roughly -1%. The $9.10 billion market cap and an average daily trading volume of 7.26 million shares confirm that liquidity is not the constraint.

Verdict on the 6% Buffer

The payout itself looks reasonably durable in the near term. The coupon income is contractual; the fund has delivered steady monthly payments for years; the duration is short; and falling rates are taking some pressure off lower‑rated issuers. The real risk sits in the price, not the income stream. A roughly three‑percent spread and close to ten percent in CCC‑rated bonds don’t leave much room if defaults pick up the way many expect.

JNK works for investors who want monthly income and are comfortable with the day‑to‑day swings that come with high‑yield credit. Anyone treating it like a stand‑in for Treasuries is signing up for a very different kind of risk than the yield alone might suggest.