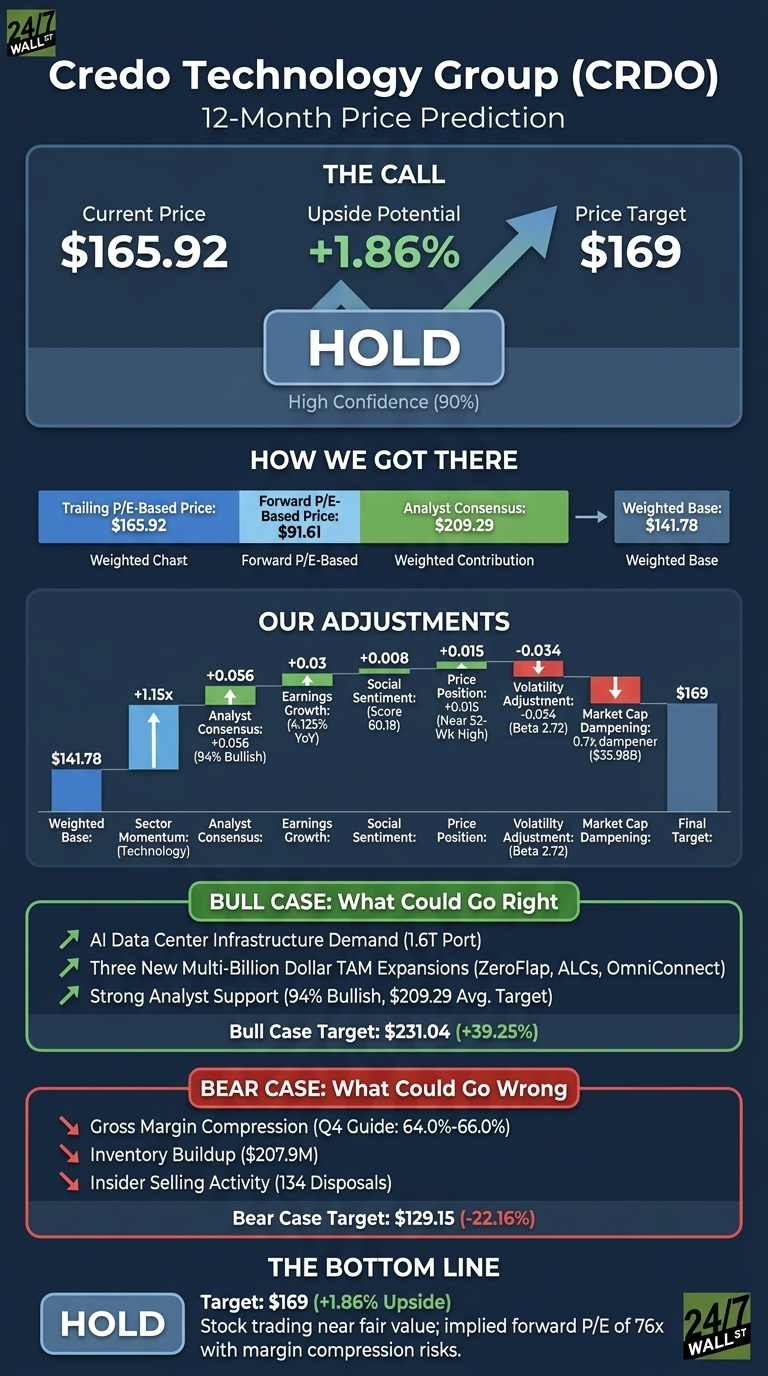

Credo (NASDAQ: CRDO | CRDO Price Prediction) has been one of the wildest rides in the AI infrastructure trade. After ripping 285.5% over the past year and another 74.21% in the last month, the connectivity chip designer is brushing up against its 52-week high. Our 24/7 Wall St. price target for Credo is $169, implying just 1.86% upside from $165.92. That earns a hold rating with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $165.92 |

| 24/7 Wall St. Price Target | $169 |

| Upside | 1.86% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Record Quarter, Then a Sharp Pullback

Credo is up 15.31% YTD, but trading has been violent. Shares fell 9.49% over the past week and 8.08% in the most recent session alone, leaving CRDO roughly 2% below its $213.80 52-week high.

The fundamentals justify the rally. In Q3 FY2026, reported March 2, 2026, Credo posted revenue of $407.01 million, up 201.5% YoY and beating estimates by 5%. Non-GAAP EPS came in at $1.07 versus a $0.9407 consensus, a 13.75% beat.

Operating income surged 471.21% YoY and the cash pile expanded to $1.22 billion. CEO Bill Brennan flagged “three new multi-billion dollar TAM expansions through ZeroFlap optics, ALCs, and OmniConnect” as the next leg of the story.

Why Bulls See $230+

The bull case is straightforward: AI buildouts are not slowing. Credo’s AECs, retimers, optical DSPs, and SerDes chiplets sit inside hyperscaler racks where 1.6T port adoption is just starting.

The $209.29 Wall Street consensus reflects 15 Buy ratings against just 1 Hold, and our bull-case scenario projects $231.04 over the next twelve months, a 39.25% total return.

What Could Go Wrong

The bear case has teeth. Q4 FY2026 guidance calls for non-GAAP gross margin of 64%-66%, meaningful compression from Q3’s 68.6%.

Inventory ballooned to $207.9 million, and insider selling has been relentless: 134 disposal transactions over the past three months from CEO Brennan, CTO Cheng, and CFO Fleming, with zero purchases.

Bulls would counter that much of this activity reflects scheduled 10b5-1 plans, with coordinated sales on April 5 at identical $101.45 prints. Hyperscaler concentration also remains a concern. Our bear-case scenario lands at $129.15, a 22.16% decline.

Hold for Now

I land on hold. The 24/7 Wall St. price target of $169 sits essentially where Credo trades today, with 90% confidence in that range. The deciding factor is the implied 76x forward multiple against guided margin compression.

I’d be a buyer here on a pullback toward $140 or a Q4 earnings report that holds gross margin north of 66%. I’d stay on the sidelines if margins fall below 64% or if hyperscaler order velocity decelerates into the June 1, 2026 earnings release.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $169 |

| 2027 | $178 |

| 2028 | $185 |

| 2029 | $192 |

| 2030 | $197.50 |

These projections track our base-case five-year trajectory of 3.55% annualized returns. Significant upside toward the $362.07 bull-case finish would require Credo’s ZeroFlap, ALC, and OmniConnect lines to scale into material revenue contributors.