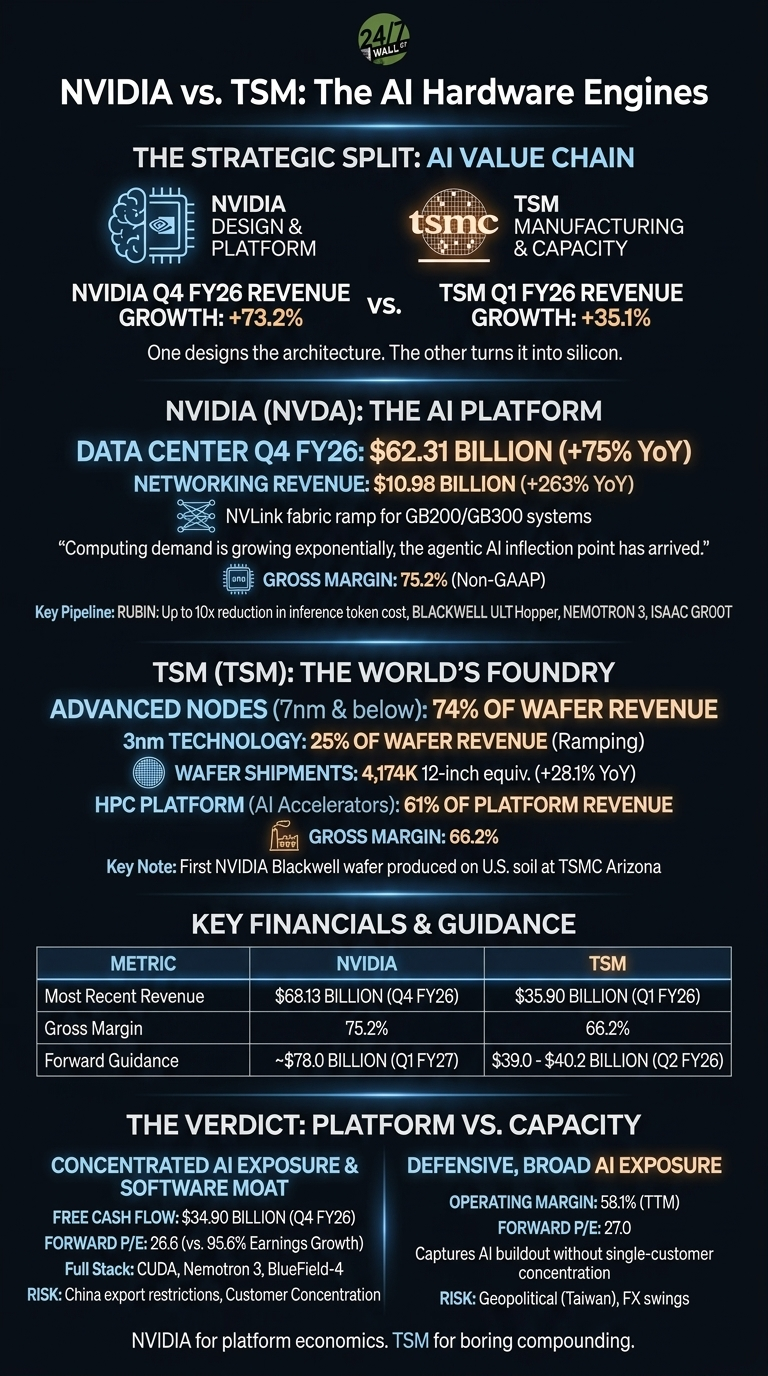

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) and Taiwan Semiconductor Manufacturing (NYSE:TSM) just delivered the two most consequential earnings reports in AI hardware. NVIDIA closed fiscal 2026 with a 73.21% revenue surge, while TSMC, the foundry that physically builds those chips, posted 35.1% growth.

One designs the architecture. The other turns it into silicon. Their results show how AI dollars are splitting along the value chain.

Blackwell Networking Surges. 3nm Wafers Carry Taiwan.

NVIDIA’s Data Center segment hit $62.31 billion, but the wild card was networking, which jumped 263% year over year as NVLink fabric ramped for GB200 and GB300 systems. Jensen Huang framed the moment bluntly: “Computing demand is growing exponentially, the agentic AI inflection point has arrived.” Gaming also held up at $3.72 billion, helped by Blackwell consumer parts.

| Business Driver | NVIDIA | TSMC |

| Main Growth Engine | Data Center compute and NVLink | 3nm and 5nm leading-edge wafers |

| Gross Margin | 75.2% | 66.2% |

| Forward Quarter Guide | ~$78.0 billion | $39.0 to $40.2 billion |

TSMC’s mix tells the manufacturing side. Advanced nodes (7nm and below) made up 74% of wafer revenue, with 3nm alone at 25%. HPC, the platform housing AI accelerators, accounted for 61% of platform revenue. Wafer shipments climbed 28.1%, a useful read on real unit demand rather than pricing alone.

Platform Owner vs. Capacity Owner

The strategic split runs deeper than the headline numbers. NVIDIA is selling a full stack: Rubin (which Huang says delivers an order-of-magnitude lower cost per token over Blackwell), CUDA, Nemotron 3, BlueField-4, and Isaac GR00T for robotics. The multiyear Meta partnership spanning millions of Blackwell and Rubin GPUs shows where pricing power lives.

TSMC’s bet is physical: capex of NT$350.76 billion last quarter, Arizona ramping (the first Blackwell wafer rolled off U.S. soil there), and a 2nm pipeline. Notably, NVIDIA carries $95.2 billion in supply commitments, much of which flows to TSMC. They are partners.

Risks diverge too. NVIDIA’s Q1 FY27 outlook explicitly excludes any Data Center compute revenue from China, a real revenue hole that guidance still beats through. TSMC carries Taiwan geopolitical risk and FX swings (USD/NTD moved 32.88 to 31.59).

The Next Test Is Rubin Pull-Through

I want to see whether Rubin instances at AWS, Azure, Google Cloud, and Oracle generate the same hyperscaler enthusiasm Blackwell did. Watch TSMC’s Q2 guide too: $39 to $40 billion with operating margin of 56.5% to 58.5% implies leading-edge utilization stays near full.

Why I Lean Toward TSMC for the Boring Compounding

If you want concentrated AI exposure with the deepest software moat, NVIDIA still owns the room. Free cash flow of $34.9 billion in a single quarter is staggering, and the forward P/E of 26.6 looks reasonable against 95.6% earnings growth.

Personally, I lean TSMC. Every credible AI roadmap, including NVIDIA’s Rubin, runs through Hsinchu. Trading near a forward P/E of 27 with 58.1% operating margins, TSMC captures the AI buildout without single-customer concentration.

For turnaround-style mandates, neither name screens cleanly. That said, for defensive AI exposure, TSMC stands out. For platform economics, NVIDIA stands out. I would only change my view if leading-edge utilization in Taiwan slipped, or if Google’s TPU pulled meaningful share from CUDA workloads.