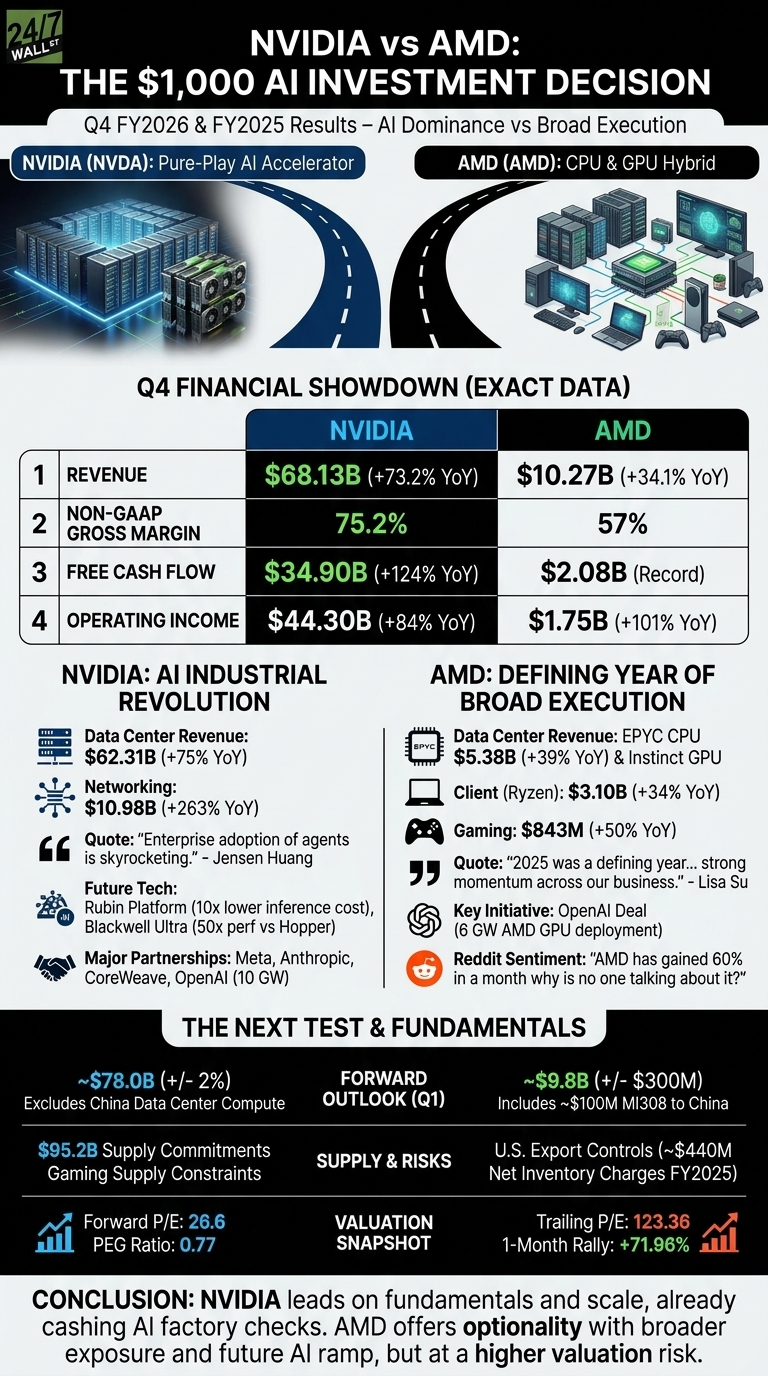

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) and AMD (NASDAQ:AMD) closed the books on blockbuster quarters. NVIDIA posted $68.13 billion in Q4 FY2026 revenue on 73.21% growth. AMD followed with $10.27B and 34.1% YoY. Both ride the same AI wave, yet their businesses, margins, and customer mix tell very different stories.

Blackwell Prints Cash. AMD Builds Breadth.

NVIDIA’s Data Center segment alone generated $62.31 billion, with networking up a staggering 263% YoY as NVLink fabric ships inside GB200 and GB300 racks. Jensen Huang told investors that “enterprise adoption of agents is skyrocketing” and that customers are racing to fund the AI industrial revolution. The tone reads like a victory lap.

AMD’s Q4 was broader and scrappier. Data Center hit $5.38B (+39% YoY) on EPYC plus Instinct GPUs, Client jumped to $3.10B (+34%), and Gaming surprised at $843M (+50%).

Lisa Su called 2025 “a defining year for AMD” with record revenue and earnings. The diversification matters, because NVIDIA’s gaming and auto lines are tiny by comparison.

| Q4 Driver | NVIDIA | AMD |

| Revenue | $68.13B | $10.27B |

| Non-GAAP Gross Margin | 75.2% | 57% |

| Free Cash Flow | $34.90B | $2.08B |

| Anchor Customer | Meta, Anthropic, CoreWeave | OpenAI (6 GW) |

Pure-Play Accelerator vs. CPU and GPU Hybrid

NVIDIA is doubling down on full-stack accelerated computing, with Rubin promising 10x lower inference token cost than Blackwell, and partnerships spanning Meta, Anthropic, CoreWeave, and the DOE Genesis Mission. Margins reflect that pricing power.

AMD is playing a wider field. Helios rack-scale, MI450 ramps, EPYC Venice, and the headline OpenAI 6 GW deal anchor the AI roadmap, while Ryzen and Radeon keep cash flowing from PCs and consoles.

The cost is structural: 17.1% operating margin against NVIDIA’s 65%.

The Next Test Is China and Supply

NVIDIA’s Q1 FY2027 outlook of $78 billion explicitly excludes China Data Center compute, and supply commitments now sit at $95.2 billion. Gaming supply is also tight.

AMD guided to $9.8B for Q1 with only $100M in MI308 China revenue baked in, after eating $440M in inventory charges last year. I will keep an eye on whether MI450 ships on time in H2 2026 and whether Rubin’s economics actually show up at hyperscaler customers.

Why NVIDIA Leads on Fundamentals, While AMD Offers Optionality

On the numbers, NVIDIA carries the stronger fundamental case. The combination of 26x forward earnings, a 0.77 PEG, and $34.90B in single-quarter free cash flow is hard to argue with at this scale. Polymarket traders also lean bullish on May, with the $208 contract at 0.835 probability.

AMD looks more interesting for risk-tolerant investors who want optionality on the OpenAI ramp, but a 123 trailing P/E and 71.96% one-month rally make the entry uncomfortable. I would rather wait for MI450 shipments to prove the thesis than chase the chart. For now, only one of these two is already cashing the AI factory checks at scale.