Analysts at DZ Bank just put their stamp of approval on one of Wall Street’s most-watched AI names, launching coverage of Palantir Technologies (NASDAQ:PLTR | PLTR Price Prediction) with a Buy rating and a $175 price target. A fresh initiation carries a different weight than a routine target hike. It means a new institutional voice has taken the time to build a model, evaluate the bull and bear cases, and publicly back the stock.

For Palantir shareholders, that matters. The stock has long been a battleground, with bulls pointing to the Artificial Intelligence Platform (AIP) and accelerating commercial traction, while skeptics flag a forward P/E ratio of 118x. DZ Bank is now firmly in the bull camp. For related coverage, see our recent Palantir stock analysis.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| PLTR | Palantir Technologies | DZ Bank | Initiation | N/A | Buy | N/A | $175 |

The Analyst’s Case

DZ Bank didn’t publish extensive commentary alongside its rating, but the $175 target signals clear confidence in Palantir’s AI-driven growth trajectory. The call aligns with the broader bullish narrative that has powered the Palantir stock story over the past year.

That narrative rests on hard numbers. Palantir closed fiscal 2025 with revenue of $4.475 billion, up 56% year over year, and management guided 2026 revenue to $7.182 to $7.198 billion, representing roughly 61% growth. The company’s Rule of 40 score hit 127% in Q4 2025, a rare combination of growth and profitability.

Company Snapshot

Palantir builds enterprise software platforms, including Gotham, Foundry, and AIP, serving both U.S. government and commercial customers. The company carries a market capitalization of roughly $365 billion and has become a flagship name in the AI software space.

In Q4 2025, Palantir’s U.S. commercial revenue grew 137% year over year to $507 million, while U.S. government revenue climbed 66% to $570 million. That dual-engine momentum is central to the bull thesis.

Why the Move Matters Now

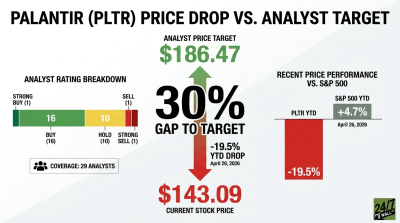

PLTR stock closed at $152.62 on April 22, meaning DZ Bank’s $175 target sits comfortably above recent trading levels. It also lands below the broader Wall Street consensus target of $186.47, positioning DZ Bank as constructive without being the most aggressive voice on the Street.

That’s a meaningful framing. The stock trades well off its 52-week high of $207.52, and valuation remains the central bear argument. A measured Buy rating with a sub-consensus target acknowledges the growth story while respecting multiples.

What It Means for Your Portfolio

For retirement-focused investors, the DZ Bank initiation adds another pillar to the Palantir bull case without changing the fundamental calculus. The company is delivering rare growth and profitability together, yet the stock’s elevated multiple means volatility is likely to remain the norm.

The sensible approach for long-term investors is moderation. Current holders may view the fresh Buy rating as validation, but those considering new positions could weigh scaling in over time rather than committing capital in one move. With 17 Buy, 10 Hold, and 2 Sell ratings on the Street, Palantir stock remains a classic divided name, and DZ Bank’s vote tilts the ledger a bit more firmly toward the bulls.