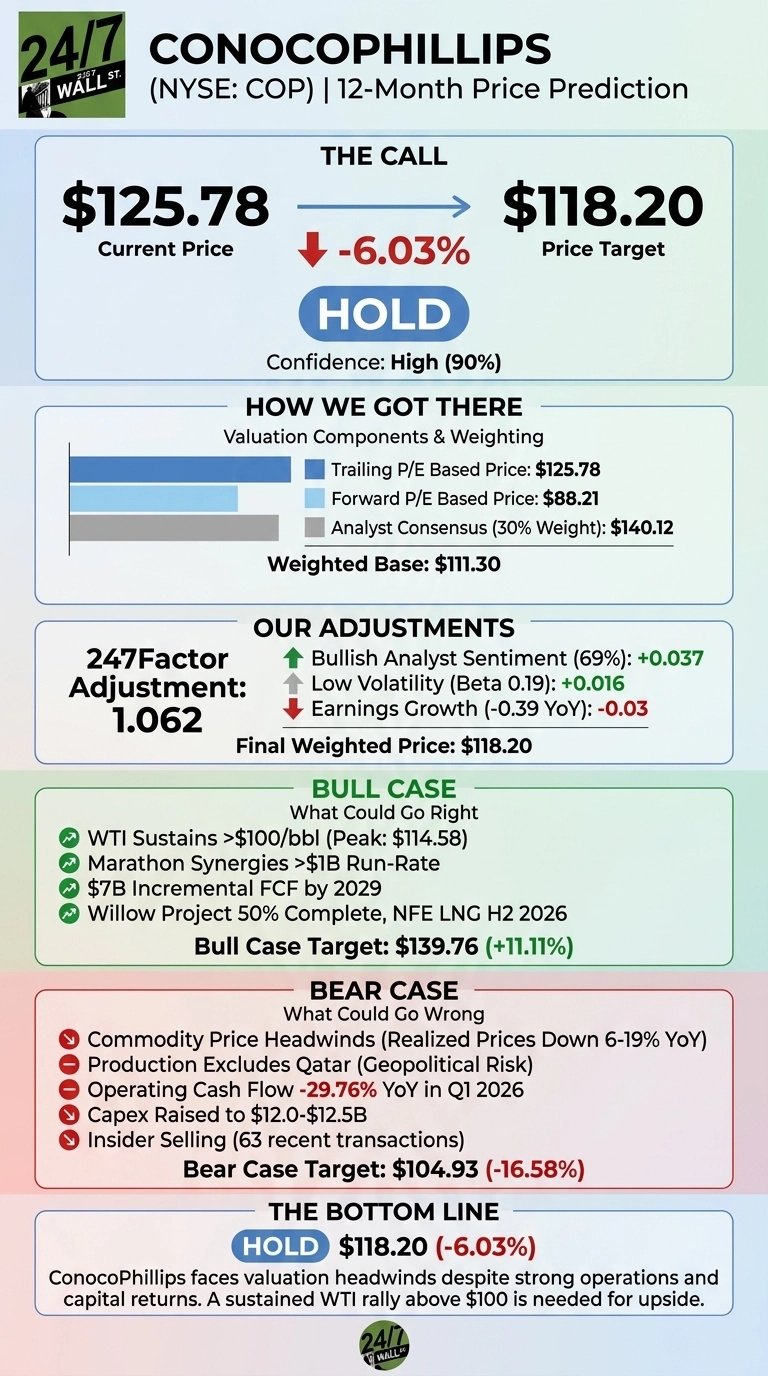

Our ConocoPhillips (NYSE:COP | COP Price Prediction) call comes on the heels of a mixed Q1 2026 earnings report, where adjusted earnings beat but revenue missed amid softer realized prices. Below is the verdict, the math, and the scenarios that could move it.

The 24/7 Wall St. Price Target for ConocoPhillips

Our 24/7 Wall St. price target for ConocoPhillips is $118.20 over the next 12 months, against a current price of $125.78. That implies roughly 6% downside, and our recommendation is hold. Confidence in the model output is High (0.9). The setup looks like a quality energy compounder trading slightly ahead of fundamentals after a 43.3% rally off October lows.

| Metric | Value |

|---|---|

| Current Price | $125.78 |

| 24/7 Wall St. Price Target | $118.20 |

| Upside/Downside | -6.03% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our 24/7 Wall St. price target sits below where COP trades today, and that deserves humility. Real upside could come from a sustained WTI move above $100/bbl (it printed $114.58 on April 7), or from Marathon synergies exceeding $1 billion run-rate. Treat our number as one datapoint. The bull case below outlines why ConocoPhillips could outperform our model.

A 46% One-Year Run Sets a High Bar

COP is up 35.39% YTD and 45.99% over one year, sitting just 3% off its 52-week high of $135.87. Q1 2026 delivered adjusted EPS of $1.89 versus $1.69 expected, but revenue of $16.054 billion missed by 2.14% and net income fell 23.13% YoY as average realized prices slipped to $50.36/BOE. Management still repurchased $1 billion of stock and declared a $0.84 dividend.

The Case for $140+

Bulls have a credible story. Wall Street consensus sits at $140.12, with 20 buy ratings against just 2 sells. Ryan Lance is targeting $7 billion in incremental free cash flow by 2029, with $1 billion per year from 2026 through 2028.

Add the Willow Alaska project at 50% completion, NFE LNG startup in H2 2026, and 45% of CFO returned to shareholders, and a re-rate toward $140 is plausible if WTI holds near $140.

What Could Go Wrong

The bear case starts with commodity sensitivity. Realized prices have fallen 6% to 19% YoY across recent quarters, and operating cash flow dropped 29.76% YoY in Q1 2026. 63 recent insider transactions have skewed toward selling. Capex was raised to $12 to $12.5 billion, and Qatar production is excluded from guidance amid Middle East conflict. A bear scenario lands near $104.93 (-16.58%).

Bulls would counter that the net income decline is largely tied to commodity price moves and one-time Marathon integration costs, while the capex bump funds high-return Permian activity and Willow.

Hold for Now

My 24/7 Wall St. price target stays at $118.20, hold, with high (90%) confidence. The tipping factor is valuation: COP trades near 52-week highs while earnings power has compressed. I would be a buyer here if WTI sustains above $100 and Q2 2026 confirms Marathon synergy run-rate. I would stay on the sidelines if realized prices retest the $42.46/BOE Q4 2025 level.

ConocoPhillips Price Prediction 2026-2030

Looking further ahead, here is where our model projects COP could trade, assuming current trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $118.20 |

| 2027 | $120.50 |

| 2028 | $122.00 |

| 2029 | $123.50 |

| 2030 | $124.87 |

These projections assume ConocoPhillips executes on Willow first oil in early 2029 and meets its $7 billion incremental FCF target by 2029. Significant upside or downside could result from sustained WTI moves outside the $60 to $100/bbl range.