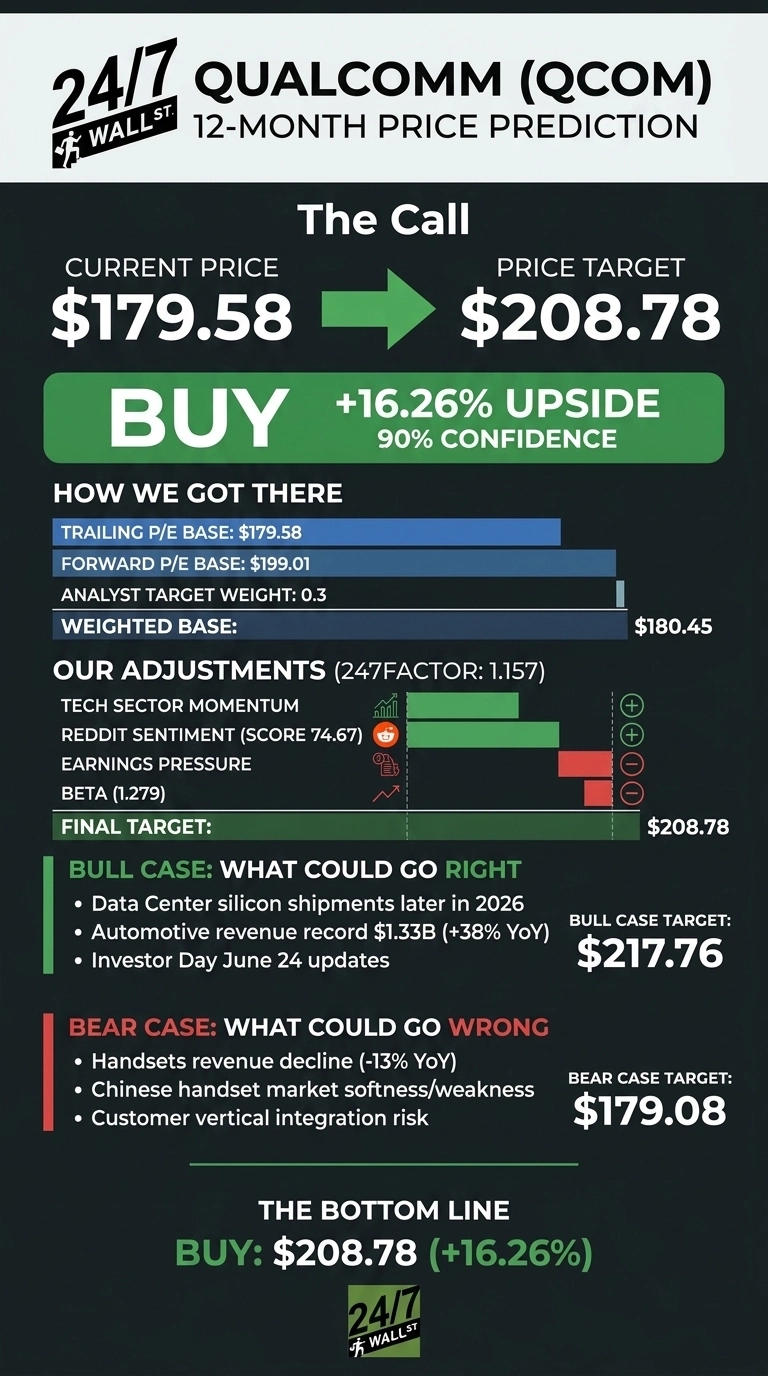

I’m opening with the verdict because the data deserves it. Qualcomm (NASDAQ:QCOM | QCOM Price Prediction) just delivered a Q2 FY26 beat, and our proprietary model now points meaningfully higher from here. Our 24/7 Wall St. price target for Qualcomm is $208.78, implying 16.26% upside from $179.58. The recommendation is buy with high confidence (90%).

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $179.58 |

| 24/7 Wall St. Price Target | $208.78 |

| Upside | 16.26% |

| Recommendation | BUY |

| Confidence Level | 90% |

A V-Shaped Recovery into Earnings

Qualcomm has staged a violent round trip. The stock fell from a December peak of $179.26 to a March low of $129.39, then ripped back, gaining 39.45% over the past month and 23.79% over the past year. Shares now sit 26% below the 52-week high of $203.60.

The catalyst was Q2 FY26 earnings on April 29, 2026. Revenue of $10.60 billion beat estimates by 0.18%, and non-GAAP EPS of $2.65 beat by 3.67%. Automotive set a record at $1.33 billion (+38% YoY) and IoT grew 9%, offsetting a 13% handset decline tied to memory supply constraints. The stock jumped 15.12% on the session.

The Case for $217 and Higher

Bulls have a clean thesis. CEO Cristiano Amon told investors Qualcomm is in a period of “profound industry transformation” with a leading hyperscaler custom silicon engagement on track for initial shipments later this calendar year.

The June 24 Investor Day is set to detail Data Center and Physical AI roadmaps. Diversification away from handsets is real: automotive plus IoT grew a combined 20% YoY. Capital return is aggressive, with $5.4 billion repurchased in H1 FY26 and a fresh $20 billion authorization. Our bull-case scenario reaches $217.76 over the next 12 months.

The Risks Worth Watching

The bear case starts with concentration. Handsets fell 13% YoY on memory supply pressure and Chinese OEM softness, and Q3 guidance of $9.2B to $10.0B revenue with non-GAAP EPS of $2.10 to $2.30 implies a sequential step-down.

Operating income fell 26% YoY, although bulls would note net income surged 162% on a one-time tax benefit and that management says Chinese handset revenue should bottom in Q3. Customer vertical integration risk remains, and the consensus analyst target of $150.10 sits below the current price, with 22 Hold ratings versus 11 Buy. Our bear-case scenario lands at $179.08.

Our Take on Qualcomm Here

The 24/7 Wall St. price target of $208.78 reflects a buy rating at 90% confidence. The tipping factor for me is the data center optionality: a hyperscaler ramp later in 2026, paired with record automotive growth, gives Qualcomm a credible path off handset dependency. The setup looks constructive if the June 24 Investor Day quantifies the data center opportunity. The thesis weakens if Q3 results show Chinese handset weakness extending into Q4 instead of bottoming.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $208.78 |

| 2030 | $291.02 |

These projections assume Qualcomm delivers on its data center ramp and FY29 revenue goals. Material upside or downside could come from the pace of hyperscaler adoption or a deeper handset cycle downturn.