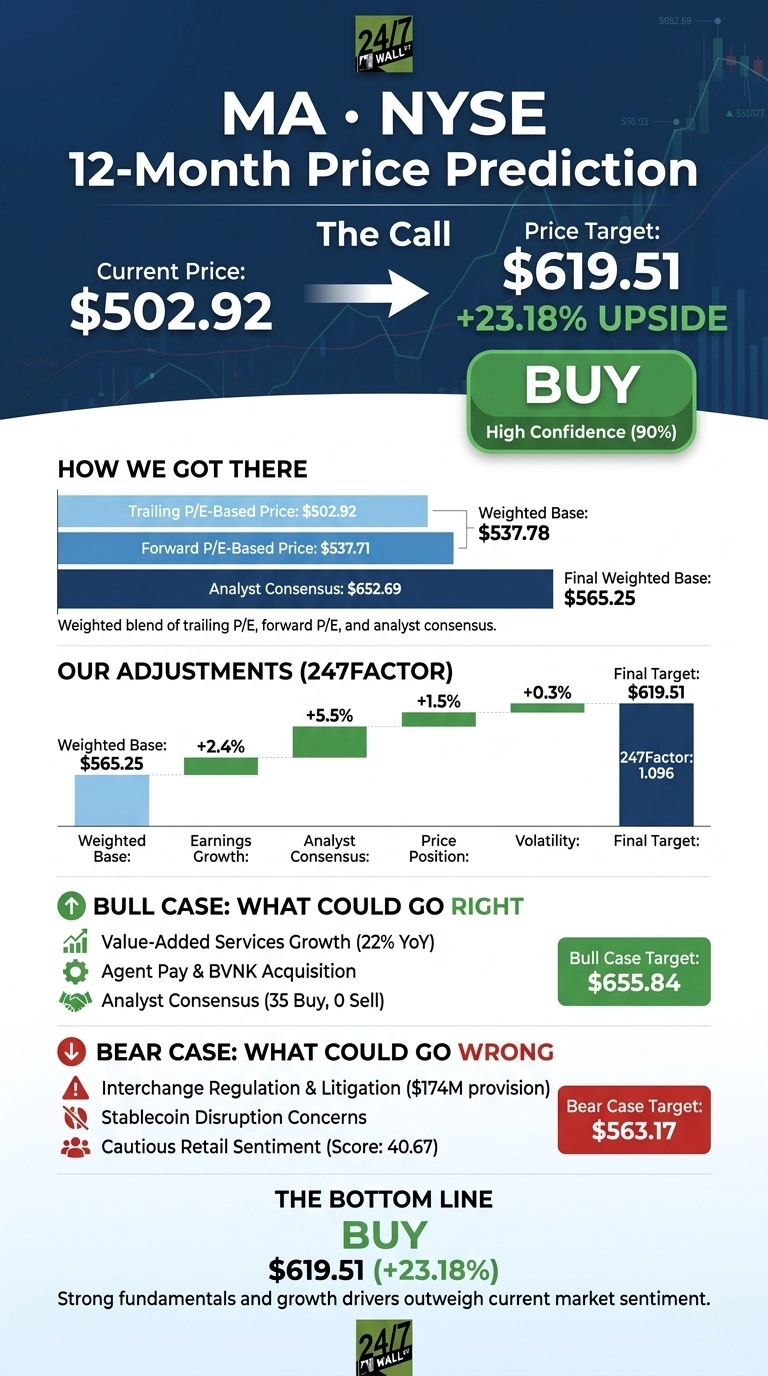

Our Mastercard (NYSE:MA | MA Price Prediction) thesis is straightforward: the stock has corrected meaningfully in 2026, but the underlying business is accelerating. The 24/7 Wall St. price target for Mastercard is $619.51, implying 23.18% upside from the current price of $502.92.

Our recommendation is buy at 90% confidence, the high end of our scale.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $502.92 |

| 24/7 Wall St. Price Target | $619.51 |

| Upside | 23.18% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Reset Quarter Despite a Beat

Mastercard is down 11.62% year to date and 7.69% over the past year, despite trading just 9% below its 52-week high of $599.05 and well above the 52-week low of $479.68. Shares fell 4.25% on the Q1 earnings report despite a clear beat.

Q1 2026, reported April 30, 2026, delivered adjusted EPS of $4.60 versus $4.41 consensus, on revenue of $8.40 billion, up 15.83% YoY. Cross-border volume rose 13%, value-added services grew 22%, and adjusted operating margin expanded to 60.8%, even after absorbing a $202 million restructuring charge.

The Case for $650+

Bulls have a clean story. Mastercard delivered a fourth consecutive EPS beat, FY 2025 revenue grew 16.42% to $32.79 billion, and value-added services have compounded at 22% to 26% for several quarters.

Agent Pay positions MA inside the agentic commerce stack, and the BVNK deal converts a stablecoin threat into a stablecoin product line. Wall Street is aligned: 35 Buy ratings against 3 Holds and zero Sells, with a Street target of $652.69. Our bull case scenario points to $655.84 by May 2027, a 30.41% total return.

The Risks Worth Watching

Bears point to interchange regulation, U.S. merchant class litigation (a $174 million Q4 2025 provision), Pillar 2 minimum tax pressure, and stablecoin disintermediation.

Counterfactually, the $202 million restructuring charge weighed on Q1 margins yet operating margin still expanded 150 basis points, and the BVNK acquisition reframes the stablecoin risk as an opportunity. Our bear case lands at $563.17, still 11.98% above today.

Why MA Looks Compelling Here

The 24/7 Wall St. price target of $619.51 reflects a high-quality compounder trading at a multi-year sentiment trough while fundamentals accelerate. With 90% model confidence and the bear case still positive, the asymmetry favors patient buyers.

The setup looks constructive if cross-border volume holds double-digit growth and VAS stays above 20%. The thesis weakens if interchange litigation produces a material settlement or stablecoin adoption visibly cannibalizes switched transactions.

Mastercard Price Prediction 2026-2030

Looking further out, here is where our 24/7 Wall St. price target model projects Mastercard could trade, assuming current trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $619.51 |

| 2027 | $695 |

| 2028 | $780 |

| 2029 | $855 |

| 2030 | $936.67 |

These projections assume Mastercard sustains roughly 13% annualized returns. Significant deviation could come from interchange reform or accelerated agentic and stablecoin adoption.