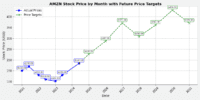

Micron Technology (NASDAQ: MU | MU Price Prediction) has gained 597.2% over the past year, closing May 1 at $542.21 after starting last May at $77.58. That is nearly a 7× move in 12 months, and the stock now trades roughly 1% from its all-time high of $545.91. For a retirement-focused investor watching from the sidelines, the question is honest and uncomfortable: is there still time, or did the AI memory trade already happen?

Let us consider the three lenses that actually matter.

Valuation: Cheap on Forward Numbers, Stretched on the Cycle

On the surface, Micron looks affordable. The trailing P/E is 26, and the forward P/E based on consensus is just 6. With forward EPS pegged at $58.05, that arithmetic looks irresistible. The catch is what those forward earnings assume: continued peak-cycle memory pricing. The 247Factor model strips that assumption out and lands on an implied forward multiple of 48 on more normalized earnings power, with a base-case fair value of $360.52 and 33.51% downside. Memory is the most cyclical pocket of semiconductors. Forward P/E ratios in this sub-sector look smallest right before they look wrong.

Forward Catalyst: The Bull Case Is Genuine

The fundamentals supporting this run are genuine. In Q2 FY2026, Micron posted revenue of $23.86 billion, up 196% year over year, with non-GAAP EPS of $12.20 against an $8.79 estimate. Q3 guidance calls for revenue of $33.5 billion and non-GAAP EPS of $19.15. The Cloud Memory Business Unit alone delivered $7.75 billion at a 74% gross margin. CEO Sanjay Mehrotra said order books are stretching into 2027 and called Micron “an essential AI enabler.” Wall Street agrees: nine Strong Buys, 30 Buys, four Holds, and one Sell rating, with a consensus target of $551.40. That is essentially the current price.

Risk and Entry: What the Downside Looks Like From Here

Here is where retirement money has to be honest. The stock carries a beta of 1.606, meaning sharper drawdowns than the broader market when sentiment turns. Every prior memory cycle has ended with 50%-plus drawdowns. Insiders have been sellers, with senior executives, including the chief business officer, chief people officer, and EVP of Worldwide Sales disposing of shares in April at prices ranging from $345.13 to $465.66. There has been no offsetting open-market buying. The dividend is a token $0.60 annual payout, offering minimal income against the volatility. The 247Factor base case sees the stock at $360.52 in 12 months and the bear case at $273.52.

The Verdict

For retirement-focused investors, the risk/reward of chasing Micron at current levels has narrowed considerably. The fundamentals are extraordinary, and Wall Street still sees a few dollars of upside, but a stock that has run 597% in a year, trades within 1% of its all-time high, depends on peak memory pricing, and carries a 1.606 beta has the profile of a momentum trade rather than a retirement allocation. The asymmetry has flipped: investors are now risking a cyclical drawdown to capture the analyst target’s slim remaining upside.

For retirement investors already holding Micron with large gains, position sizing becomes a relevant consideration. For those without exposure, the setup raises the question of whether a cycle reset offers a more favorable entry than current highs.