Palantir has whipsawed traders all year, but the latest Q1 earnings reset the conversation. Palantir (NASDAQ:PLTR | PLTR Price Prediction) just delivered another blowout quarter, raised full-year guidance, and absorbed multiple analyst upgrades, yet the stock still sits well below its 52-week high. Our model says that gap is an opportunity.

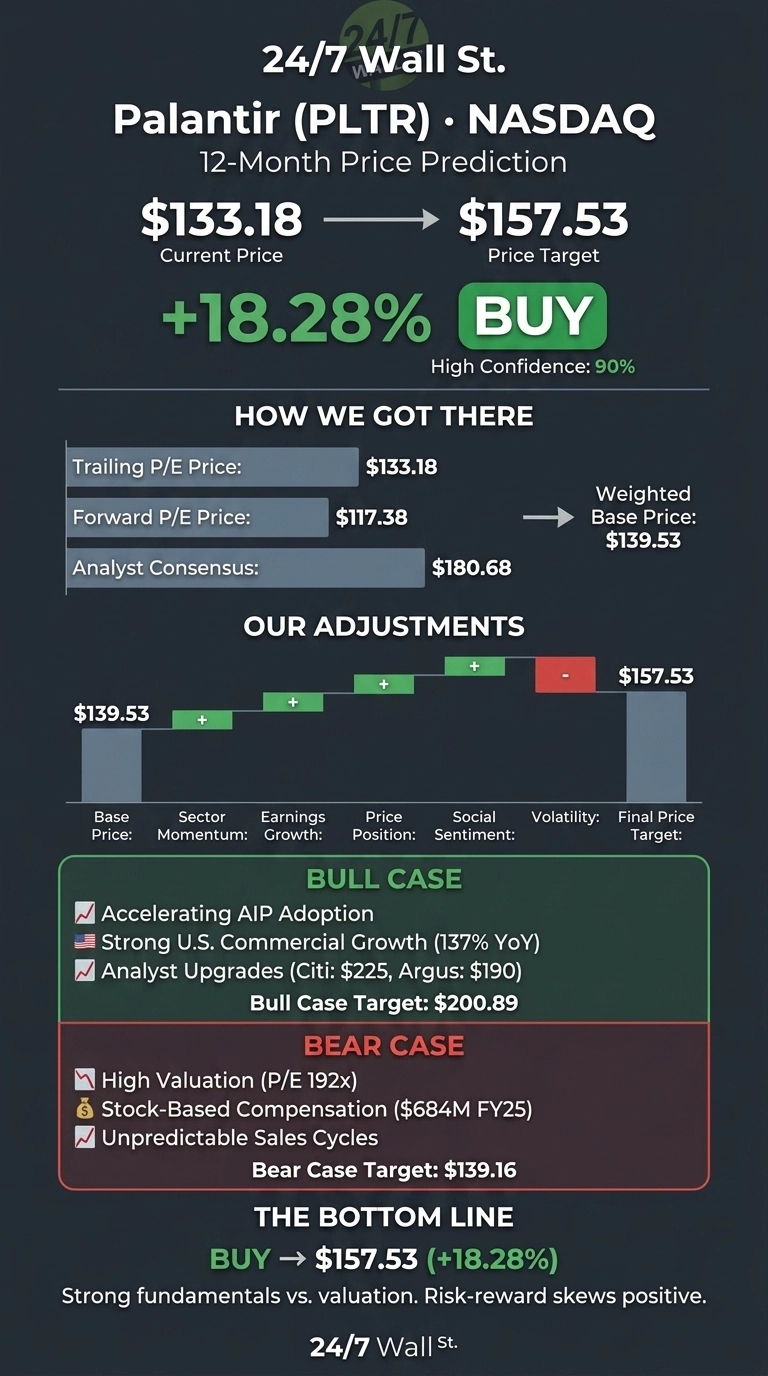

Our 24/7 Wall St. price target for Palantir is $157.53, implying meaningful upside from the current quote of $133.18. That works out to roughly 18.28% upside over the next 12 months. Our recommendation is buy, and our confidence in this forecast is high at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $133.18 |

| 24/7 Wall St. Price Target | $157.53 |

| Upside | 18.28% |

| Recommendation | BUY |

| Confidence Level | 90% |

The Q1 Earnings Report Reset the Story

Palantir is down 23.54% year to date and 8.45% over the past month, sitting 13% below its 52-week high of $207.52. That weakness is at odds with the operating story.

Q1 2026 delivered 85% YoY revenue growth and 104% U.S. revenue growth, with management raising full-year revenue guidance to 71% YoY growth and U.S. commercial guidance to 120% YoY growth.

Q4 2025 set the table: revenue of $1.41 billion (up 70% YoY), adjusted EPS of $0.25 beating consensus by 38.89%, and a record $4.262 billion in total contract value closed. CEO Alex Karp told investors, “Palantir’s Rule of 40 score is now an incredible 127%… We are an n of 1.”

The Case for $200+

Bulls have plenty to work with. Citi raised its price target to $225 from $210 with a Buy rating, citing accelerating AI demand in Palantir’s U.S. business. Argus upgraded the stock to Buy from Hold with a $190 target, raising FY26 EPS to $1.47 and FY27 to $1.94. The Wall Street consensus target sits at $180.68 with 19 Buy ratings.

If U.S. commercial keeps compounding at the 137% YoY pace seen in Q4 and AIP adoption broadens, our bull case points to $200.89 in 12 months, a 50.84% return.

The Risks Worth Watching

Palantir trades at a 192 P/E and a 149 price-to-free-cash-flow multiple. Any deceleration could compress the multiple sharply. Stock-based compensation hit $684 million for FY2025, and insider activity skews toward selling with 72 recent transactions, net selling. Polymarket traders are also cautious, with the most likely May close clustering around $132.

That said, bulls would argue heavy SBC is the cost of attracting elite engineering talent during a once-in-a-generation AI build-out, and the GAAP picture is improving fast: GAAP operating income jumped to $575.4 million in Q4, a 41% margin. Our bear case still gets to $139.16, only modestly below current levels.

The Bottom Line

Our price target of $157.53 with a buy rating reflects a stock that has corrected hard while fundamentals accelerated. The bull case rests on whether Palantir’s 120% U.S. commercial guidance is achievable. The bear case hinges on whether the 192 P/E is sustainable through any growth hiccup. On balance, the risk-reward skews positive in our model.

Palantir Price Prediction 2026-2030

Looking further ahead, here is where our model projects Palantir could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $157.53 |

| 2027 | $175 |

| 2028 | $195 |

| 2029 | $210 |

| 2030 | $224.91 |

These projections assume Palantir continues executing on AIP commercialization and government expansion. Significant upside or downside could result from AI adoption pace and any moderation in defense spending.