Dylan Patel, founder and chief analyst at SemiAnalysis, laid out a blunt thesis on the Invest Like the Best podcast (EP.468): “People are like, oh, the memory story is overplayed. Everyone gets it. And it’s like, no, no, no, you don’t get it. DRAM will double or triple from here still, because that’s how much capacity is required.” He argues that even though memory makers started responding to demand signals in late 2025, “the true incremental supply doesn’t come till ’28”, and fabs can only add 20% to 30% of capacity per year.

The stakes are real. If you chase this call at the wrong point in the cycle, you can be right on the thesis and still lose half your money when supply catches up. Memory is the most cyclical corner of tech, and the stocks move like it.

The Verdict: Directionally Right, Dangerously Late for Naive Buyers

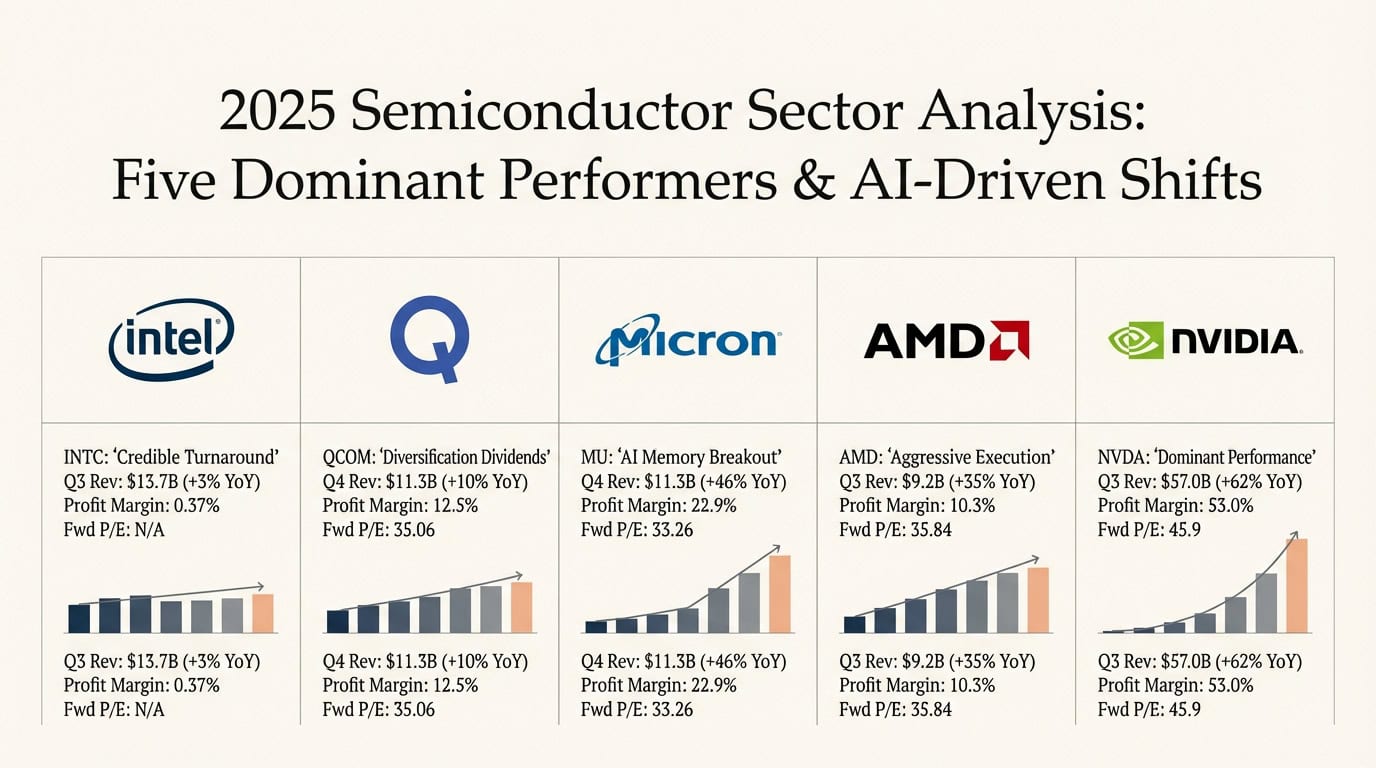

Patel’s supply math is sound. The counterweight is price. Micron Technology (NASDAQ:MU | MU Price Prediction) trades near $481 after a 596% one-year run and a 71% year-to-date gain. The market has already absorbed a large piece of the supercycle.

The concept to learn is commodity cycle pricing. DRAM is a near-commodity product. When demand outruns supply, prices can rise in triple-digit percentages, exactly what Patel notes is happening now versus TSMC’s single-digit price increases. Gross margins balloon because variable cost barely changes. Micron’s cloud memory unit did $5.28 billion in Q1 FY26 at a 66% gross margin, and company GAAP gross margin jumped from 38% to 56% year over year. Guidance calls for $18.70 billion in Q2 revenue at a 68% non-GAAP gross margin.

Run the scenario. If DRAM contract prices truly double again and Micron’s operating margin holds near 68%, trailing EPS of $21.21 could realistically push past $40. At a 15x multiple, that math supports the bull case. If supply arrives in 2028 and prices normalize, the same share count produces a fraction of those earnings, and the stock re-rates downward on both earnings and multiple. That is how memory investors lose 60% in a year after being right on the cycle.

Who This Call Fits, and Who Gets Hurt

The thesis fits investors with a multi-year horizon who buy the picks-and-shovels layer rather than the commodity producer. ASML (NASDAQ:ASML) sits on a $45.06 billion backlog with fiscal 2026 revenue guided to €36 to €40 billion. Applied Materials (NASDAQ:AMAT) saw DRAM climb to 34% of semiconductor systems revenue. Lam Research (NASDAQ:LRCX) just printed record revenue of $5.84 billion and guided June to $6.60 billion. These suppliers get paid whether prices stay high or capacity overshoots.

The call hurts the late-cycle retail buyer who piles into Micron options after a parabolic move. Reddit sentiment on MU is running at 81 to 85, with WallStreetBets threads celebrating 420-strike calls up 169%. That is the profile of euphoria at a cycle peak.

What To Actually Do With This

- Size by cycle position. Micron’s forward P/E of 8 looks cheap only if 2027 earnings hold. Model a normalized-margin case at 35% gross margin and see what EPS looks like. That is your downside.

- Prefer the equipment layer for duration. ASML, Applied Materials, and Lam Research capture TSMC’s capex ramp, which Patel pegs at $100 billion by 2028 versus $56 billion this year. Equipment orders stretch years and smooth the memory-price cycle.

- Stagger entries. Cost-averaging into a commodity cycle beats a single lump at peak sentiment. The difference between buying Micron at $70 a year ago and $487 today is the entire debate.

Patel is right that supply cannot catch up before 2028. He is also describing exactly the conditions that historically precede the next glut. Own the cycle with your eyes open: buy the shovels, respect the math, and do not confuse the back half of a run with the front.