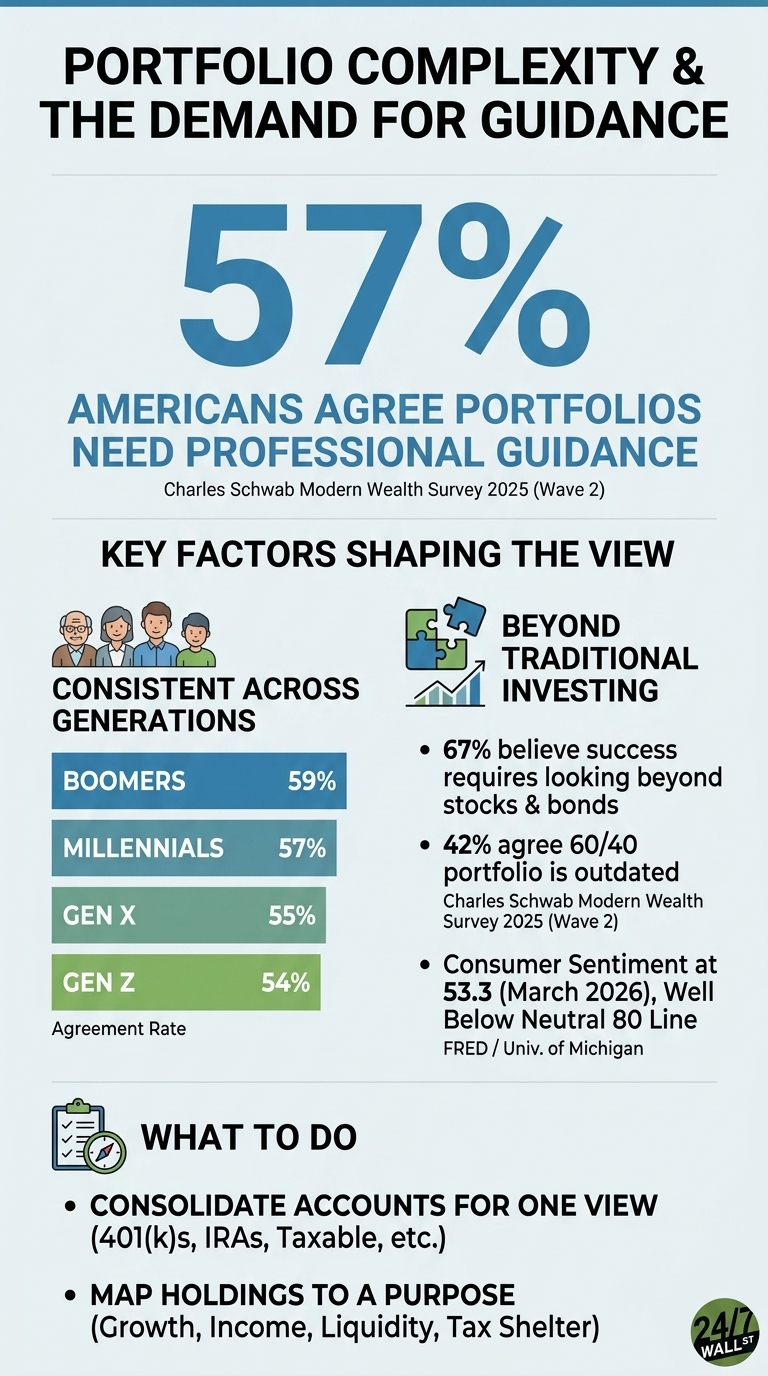

A Charles Schwab Modern Wealth Survey 2025 finding that 57% of Americans agree modern investment portfolios are more sophisticated and require more professional guidance sits at the center of a broader shift in how households manage retirement money. The figure spans age groups and aligns with measurable changes in product mix, account structures, and the tools retirees now use to generate income. This article looks at the benchmark, how the rise of complex income strategies fits in, and how the largest wealth platforms are absorbing the resulting demand.

A Generationally Consistent Benchmark

Schwab’s reading is unusually flat across cohorts: Gen Z at 54%, Millennials at 57%, Gen X at 55%, and Boomers at 59%. Households at both ends of the age spectrum are reporting the same thing about the number of moving parts in a typical portfolio, suggesting complexity is not confined to a single life stage or asset class.

The macro backdrop reinforces the read. University of Michigan consumer sentiment stood at 53.3 in March 2026, down 5.5% from February and well below the 80 line that separates pessimistic from neutral readings. Decisions made during stretches of low confidence tend to draw households outward for help.

Why the Tools Themselves Got Harder

Investing in bonds now extends well beyond a Treasury ladder and a total bond fund. 67% of Americans believe successful investing today requires looking beyond stocks and bonds, and 42% agree the classic 60/40 portfolio is outdated. That belief is showing up in product flows. Covered call ETFs, collateralized loan obligation funds, preferred stock funds, and multi-asset income vehicles each require the holder to understand option overwriting, credit tranching, call risk, and rebalancing rules that a plain-vanilla index fund does not entail.

The rate environment is part of the pull. The 10-year Treasury yield was 4.35% on April 27, 2026, with the 10-year minus 2-year spread at 0.57%. A modest curve makes traditional bond ladders less effective at funding retirement spending, pushing investors toward yield-enhancement strategies that require active oversight.

Operational Complexity Is Compounding

The household-level mechanics align with the survey: 61% of investors maintain multiple portfolios, with 54% citing different financial goals and 30% citing access to new investment products. Another 45% are interested in owning alternatives, and 33% are interested in event contracts. A retiree juggling a workplace 401(k), a rollover IRA, a taxable brokerage account, and a smaller alternatives sleeve is making cross-account allocation, tax-location, and withdrawal-sequence decisions that a single statement cannot summarize.

Where the Demand Is Landing

Charles Schwab (NYSE:SCHW | SCHW Price Prediction) reported total client assets of $11.77 trillion, up 19% year over year, with Managed Investing Solutions net flows growing 46% year over year in Q1 2026. CEO Rick Wurster framed it this way: “Clients continue to turn to us for more of their financial lives, helping wealth and banking solutions reach record levels.” Schwab trades at a P/E of 18.

BlackRock (NYSE:BLK) ended Q1 2026 with $13.89 trillion in AUM and $130 billion in quarterly net inflows, including $132 billion of record Q1 iShares ETF inflows. JPMorgan Chase (NYSE:JPM) reported Asset and Wealth Management client assets of $7.1 trillion, up 18% year over year, with $54 billion in long-term AUM net inflows.

Goldman Sachs (NYSE:GS) posted record Asset and Wealth Management AUS of $3.61 trillion and 32 consecutive quarters of long-term fee-based net inflows. T. Rowe Price (NASDAQ:TROW) saw the other side, with $56.9 billion of net client outflows in 2025 as fee compression and the shift toward ETFs and alternatives reshaped its mix.

How Households Are Responding

Across the major platforms, a clear pattern is emerging in how households deal with rising financial complexity. The first move is usually to pull all accounts into a single view: 401(k)s, IRAs, taxable accounts, HSAs, and any alternative sleeves, so that duplication, gaps, and drift across the household balance sheet become visible.

From there, positions are typically assigned a purpose: growth, income, liquidity, or tax shelter. Holdings that do not serve a clear purpose often become candidates for consolidation during the next rebalancing window. For income‑oriented products such as covered‑call ETFs, CLO funds, or preferred‑stock portfolios, investors weigh the specific risks, call exposure, credit sensitivity, and distribution variability against the yield to decide whether the oversight burden is worth it or whether a managed solution makes more sense.

Flows from Schwab, BlackRock, and JPMorgan point to a growing number of households choosing the managed route.