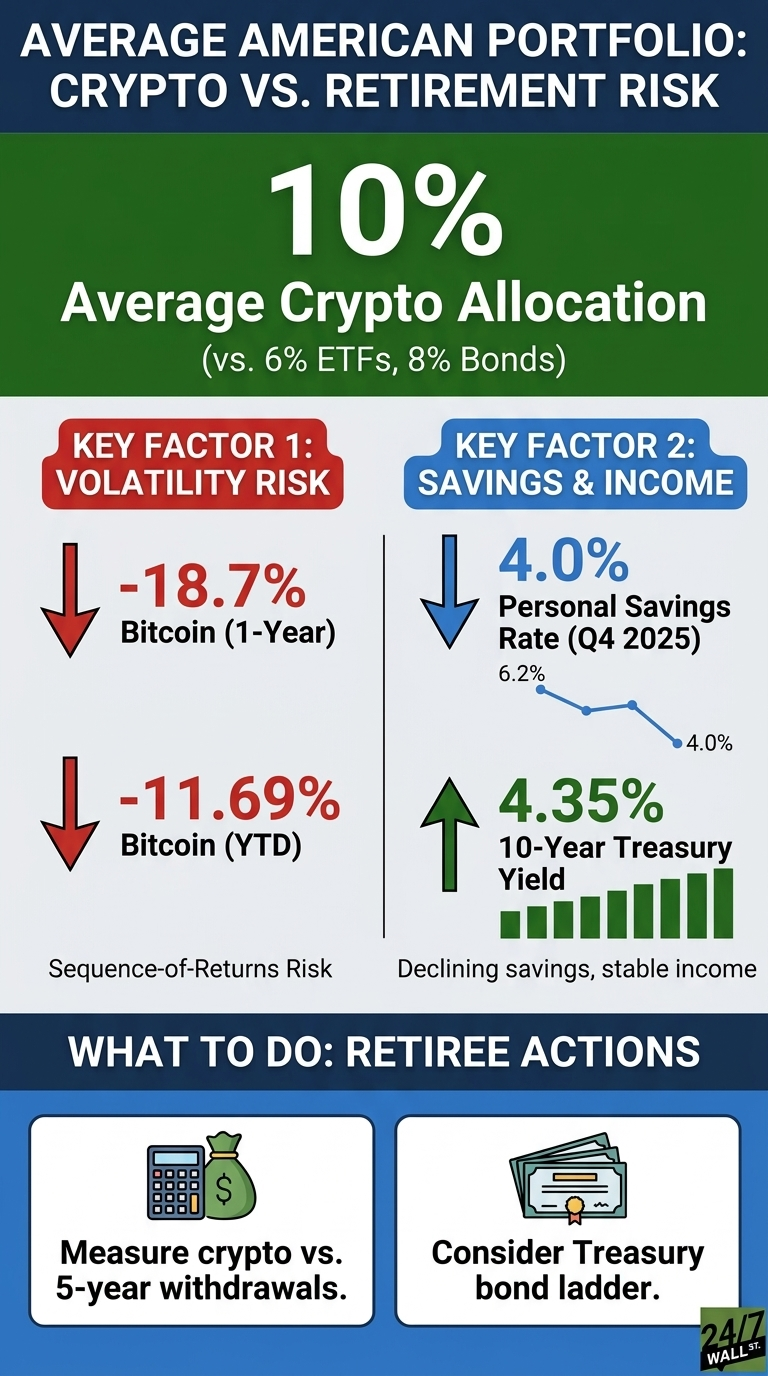

The Charles Schwab Modern Wealth Survey 2025 found that cryptocurrency now accounts for 10% of the average American investor’s portfolio, compared with 6% for exchange-traded funds and 8% for bonds. For investors in their accumulation years, that mix is a question of preference. For retirees and those within a decade of retirement, the composition introduces a different kind of math, one tied to the timing of withdrawals and the volatility of the assets being sold.

The Shift in Average Allocations

According to Schwab, 35% of investors currently hold crypto, and 65% of those holders plan to increase their allocation over the next 20 years. The average investor’s portfolio now carries more digital asset exposure than ETF exposure, a structural change from how household portfolios were typically built a decade ago, when index funds and bonds dominated retail allocation.

The mean and median tell different stories: If ten investors each hold 2% in crypto and an eleventh holds 90%, the average jumps without describing what most people actually own. The 10% figure from Schwab reflects the full distribution, including investors with concentrated positions. For a retiree comparing themselves to the benchmark, the relevant question is whether their allocation aligns with their withdrawal timeline rather than the average.

Why Sequence of Return Changes the Calculus

Bitcoin trades at $76,346.98 as of April 28, 2026, down 11.69% year-to-date and down 18.7% over the past year, despite a one-month rally of 17.15%. Ethereum is at $2,296.66, down 22.48% year-to-date and down 16.83% over five years. A retiree who needed to fund expenses by selling either asset in recent months would have realized those losses in cash, regardless of the long-term trajectory.

The order in which gains and losses occur matters more than the average return when an investor is drawing down a portfolio, a dynamic known as sequence-of-returns risk. The CBOE Volatility Index reached 31.05 on March 27, 2026, a level associated with elevated fear, before declining 42% over the following month to 18.02. Retirees holding volatile positions during such spikes face the choice of selling at depressed prices or cutting spending until markets stabilize.

The Income Side of the Tradeoff

The 10-year Treasury yield sits at 4.35%, with a 12-month average of 4.232%. A retiree holding $500,000 in 10-year Treasuries would generate roughly $21,750 in annual interest, paid on a fixed schedule and backed by the federal government. The yield curve is positively sloped, with the 10-year minus 2-year spread at 0.57%, indicating that longer-dated bonds currently pay more than short-term instruments.

Inflation complicates the picture further, as the Consumer Price Index rose to 330.293 in March 2026, up from 320.302 in April 2025. A 4.35% Treasury yield against persistent inflation produces a positive but narrow real return. Bitcoin’s 18.7% one-year decline occurred amid elevated CPI, complicating the inflation-hedge case for digital assets during that period.

Savings Capacity Is Tightening

The personal savings rate fell from 6.2% in the first quarter of 2024 to 4.0% in the fourth quarter of 2025, even as per capita disposable personal income rose from $63,638 to $67,648. Households are saving a smaller share of a larger income, so the composition of what gets saved carries more weight. A 10% average crypto allocation within investment portfolios, drawn from a shrinking pool of savings, concentrates volatility in the portion of the portfolio meant to fund future spending.

Consumer sentiment registered 53.3 in March 2026, in the pessimistic zone. That backdrop has coincided with Fed funds rate cuts from 4.5% in September 2025 to 3.75% in April 2026, lowering yields on cash and short-term instruments and prompting some investors to move toward higher-volatility alternatives.

Considerations Often Discussed for Retirees and Pre-Retirees

- The crypto share of total liquid net worth, including holdings in retirement accounts, brokerage accounts, and self-custody wallets, can be measured against expected withdrawals over the next five years.

- A bond ladder using Treasury maturities of 2, 5, and 10 years is one approach that locks in the current 4.35% 10-year yield for a portion of fixed-income needs.

- Rebalancing after large crypto moves, rather than on a fixed calendar, is another approach, with positions trimmed when allocations drift above a target by a set percentage.