Plug Power (NASDAQ:PLUG) stock is up 10% in Monday’s session, climbing from $2.78 to $3.07 and reclaiming the psychologically significant $3 level for the first time in recent weeks. That’s not a trivial threshold for a stock that spent much of the past year trading below a dollar.

The move comes on a confluence of bullish catalysts: a recent contract win, active institutional investor outreach, and improving revenue momentum. The central question, as always with Plug Power, is whether today’s enthusiasm reflects durable progress or another head fake in a stock that’s burned shareholders before.

Contract Win Reignites Commercial Momentum

A recent contract win is drawing fresh attention to Plug Power’s electrolyzer business. The company has been building a commercial pipeline, and each new project award adds credibility to the argument that hydrogen infrastructure is moving from concept to deployment at scale.

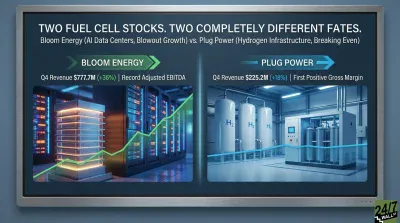

That commercial traction matters because it speaks directly to the revenue trajectory investors are watching. Plug Power reported full-year 2025 revenue of $709.92 million, up 13% year over year, and the most recent quarter showed a 18% year-over-year revenue increase to $225.2 million, beating the consensus estimate of $217.3 million.

Perhaps the most significant milestone embedded in Plug Power’s results was a positive gross margin of 2% in Q4 2025, a dramatic swing from -123% in Q4 2024. For a company that has operated with deeply negative margins for years, that inflection point is the financial foundation the bull case rests on.

Investor Outreach Signals a Trust-Building Campaign

Alongside the contract news, Plug Power has been working to rebuild confidence with institutional investors. The company’s CFO and investor relations team participated in an RBC non-deal roadshow in Toronto and Montreal on April 7 and 8, meeting directly with institutional stakeholders to walk through the business strategy and path to profitability.

New Plug Power CEO Jose Luis Crespo has also taken an unconventional approach to retail investor engagement. Crespo hosted a Reddit AMA on April 16, engaging directly with individual investors about the company’s direction, cost-cutting initiatives, and its positioning in the hydrogen economy. That kind of direct outreach signals management is serious about rebuilding trust across the full investor base, not just on Wall Street.

The profitability roadmap Crespo has laid out for Plug Power is specific and publicly committed: positive EBITDAS by Q4 2026, positive operating income by end of 2027, and full profitability by end of 2028. Those are measurable milestones investors can hold management accountable to.

Analysts Remain Cautious Heading Into Earnings

Wall Street isn’t fully on board yet. The analyst consensus for PLUG stock sits at a “Hold” rating, and the consensus EPS estimate has declined 1% over the past month, reflecting measured skepticism ahead of the upcoming earnings print. That’s worth keeping in mind when sizing any position around today’s momentum.

Susquehanna raised its Plug Power stock price target from $2.50 to $2.75 while maintaining a Neutral rating, and RBC Capital raised its target from $1.50 to $2.75 with a Sector Perform rating. Those upgrades acknowledge the improving picture, but neither firm is pounding the table. The consensus analyst price target sits at $2.83, which is actually below where PLUG stock is trading right now.

The risks are real and worth noting. Plug Power carries an accumulated deficit of $8.2 billion, posted a net loss of $1.63 billion in fiscal year 2025, and recorded approximately $763 million in non-cash asset impairment charges in Q4. The gross margin improvement is encouraging, but the company is still a long way from generating free cash flow.

The Turnaround Debate

Context matters enormously here. PLUG stock is up 238% over the past year, a remarkable recovery from a 52-week low of $0.69. The bulls see a multi-year base forming after years of destruction, with the gross margin inflection as the turning point.

The bears point to the five-year chart, where PLUG stock is still down 90% from its 2021 highs. That’s a sobering reminder of how much shareholder value has been destroyed and how many “comeback” rallies have faded. You should consider this stock if you believe the gross margin improvement is sustainable and the profitability roadmap is credible. If you’re skeptical of both, the risk profile remains elevated. For more on the broader clean energy turnaround theme, see our recent coverage of hydrogen stocks gaining momentum in 2026.

Watch for whether Plug Power stock holds above $3 into the close, and whether upcoming earnings can validate the commercial momentum driving this rally. That earnings print will be the real test of whether the hydrogen comeback narrative has legs.