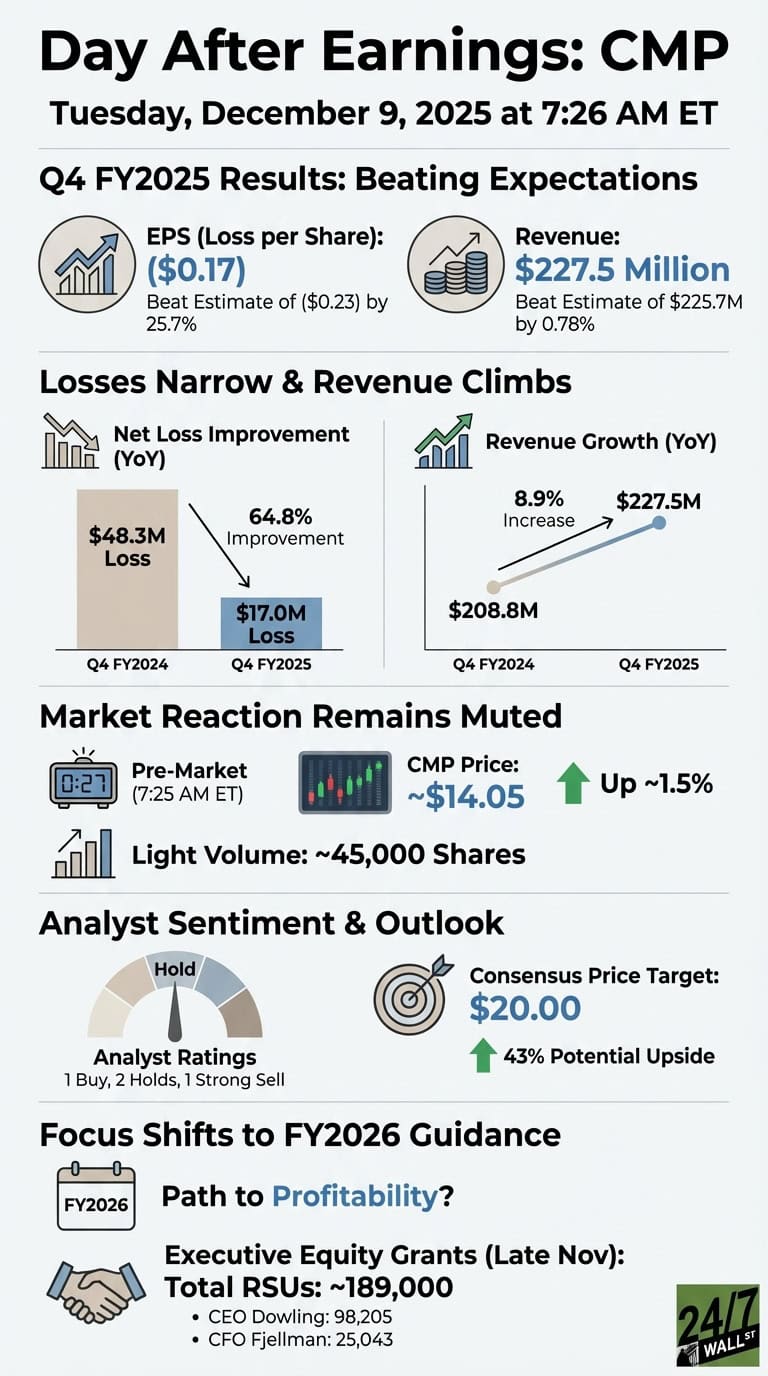

Yesterday we were watching whether Compass Minerals could stabilize its bottom line after a brutal fiscal 2024. The company delivered Q4 FY2025 results after the close on December 8, beating expectations on both EPS and revenue. This morning, shares are trading around $14.05 in pre-market, up roughly 1.5% from Friday’s close of $13.57.

Losses Narrow as Revenue Climbs

Compass Minerals reported a loss of $0.17 per share for Q4, beating the consensus estimate of a $0.23 loss by 25.7%. Revenue came in at $227.5 million, topping the $225.7 million estimate by 0.78%. More importantly, the quarter showed meaningful improvement versus the prior year. Net losses narrowed to $17.0 million from $48.3 million in Q4 FY2024, a 64.8% improvement. Revenue climbed 8.9% year over year from $208.8 million.

The company has been unprofitable for two consecutive fiscal years. FY2024 ended with a $206.1 million net loss. Sequential quarterly results have been volatile, with Q2 FY2025 revenue hitting $494.6 million during peak winter de-icing season before dropping to $214.6 million in Q3. Q4’s $227.5 million figure suggests stabilization heading into the new fiscal year.

Market Reaction Remains Muted

Despite the beat, pre-market trading has been light with only around 45,000 shares changing hands before 7:25 AM ET. The modest 1.5% gain suggests investors are taking a wait-and-see approach. Friday’s session showed typical volatility for CMP, with shares ranging from $13.23 to $13.92 before settling at $13.57. The stock has been notably quiet in after-hours and pre-market sessions, indicating no major institutional repositioning yet.

Analyst sentiment remains mixed, with one buy rating, two holds, and one strong sell. The consensus price target sits at $20.00, suggesting 43% upside from current levels if the turnaround gains traction.

Focus Shifts to FY2026 Guidance

We covered the setup before the print, noting the company’s high beta of 1.57 and recent executive equity grants totaling roughly 189,000 restricted stock units across leadership in late November. CEO Edward Dowling received 98,205 RSUs, while CFO Peter Fjellman was granted 25,043 units. These grants occurred two weeks before earnings as part of the standard compensation cycle.

Investors will want to watch whether management provides detailed FY2026 guidance and addresses the path back to profitability. Operating margins remain thin at 0.99% on a trailing twelve-month basis. With no earnings call transcript available yet, we’ll update if management commentary surfaces or if the stock’s early move shifts materially through the morning session.