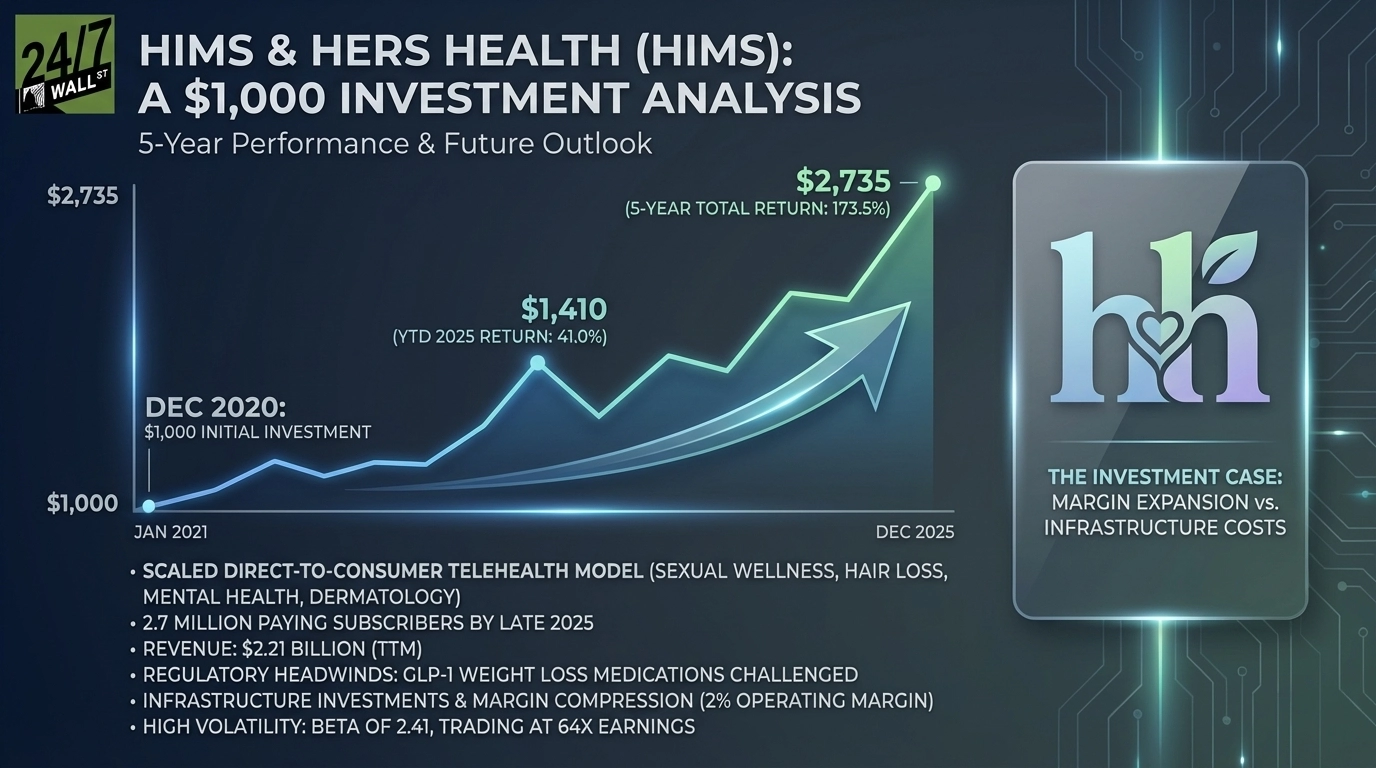

Hims & Hers Health (NYSE: HIMS) went public in January 2021 through a SPAC merger, positioning itself as a multi-specialty telehealth platform offering prescription medications, mental health support, and personal care products. The timing proved fortuitous: pandemic-era demand for virtual healthcare was surging, and the company’s direct-to-consumer model for sensitive health issues (sexual wellness, hair loss, dermatology) resonated with consumers seeking privacy and convenience.

The business scaled aggressively. Revenue jumped to $2.21 billion over the trailing twelve months, driven by subscriber growth that reached 2.7 million paying customers by late 2025. The company added roughly 700,000 subscribers in 2024 alone, though that pace slowed to around 480,000 in 2025 as regulatory headwinds hit its fastest-growing segment: GLP-1 weight loss medications.

That slowdown reflects real operational challenges. The FDA removed semaglutide from its drug shortage list, limiting Hims’ ability to sell compounded versions. A partnership with Eli Lilly fell through. Customer acquisition costs spiked as competition for GLP-1 customers intensified. The company poured capital into infrastructure: a $39 million peptide manufacturing facility, a $5 million lab acquisition, expanded compounding capacity, and new warehouse leases. Operating margins compressed from 6.5% at the start of 2025 to just 2% by Q3, even as revenue growth remained strong at 49% year-over-year.

Your $1,000 Became $2,735

A $1,000 investment in Hims at its public debut has delivered exceptional returns:

5-Year Return (Since Dec 2020)

- Initial Investment: $1,000

- Current Value: $2,735

- Total Return: 173.5%

- Annualized Return: 22.3%

1-Year Return

- Initial Investment: $1,000

- Current Value: $1,211

- Total Return: 21.1%

Year-to-Date 2025

- Initial Investment: $1,000

- Current Value: $1,410

- Total Return: 41.0%

The long-term performance reflects the company’s ability to execute on marketing (spending close to $1 billion annually) and build a recognizable brand. The stock hit $73 in 2025 before pulling back to $34 currently, highlighting the volatility inherent in a high-beta growth stock (beta of 2.41). Timing mattered: buying at the peak would have meant steep losses, while early investors who held through regulatory uncertainty were rewarded.

The stock trades at 64x earnings despite generating positive net income, suggesting the market prices in aggressive future growth rather than current profitability.

The Investment Case Centers on Margin Expansion

The bull case centers on whether infrastructure investments will expand margins toward management’s 12% target. Bulls point to diversification beyond GLP-1s—the platform offers mental health, dermatology, sexual wellness, and lab testing—along with improving unit economics showing customer payback periods under one year. The company has demonstrated the ability to scale marketing efficiently, with one analyst noting, “Hims has been terrific at scaling growth with near-perfect execution on the marketing front.”

Bears cite the 2% operating margin and forward P/E above 50x as valuation concerns. Insider selling in mid-December totaled over $11 million at prices above $36 per share. The convertible notes that could dilute shareholders if the stock crosses $70 by 2030 represent another risk factor investors are weighing.

The 173% five-year return came with significant volatility, and the stock’s beta of 2.41 suggests that pattern is likely to continue.