Middle-market lending has shifted from bank balance sheets to specialized investment vehicles, creating opportunity for income investors willing to accept credit risk and volatility. VanEck BDC Income ETF (NYSEARCA:BIZD) packages that exposure into a single ticker yielding 12%, but its unusual structure demands closer examination.

What Makes This ETF Different

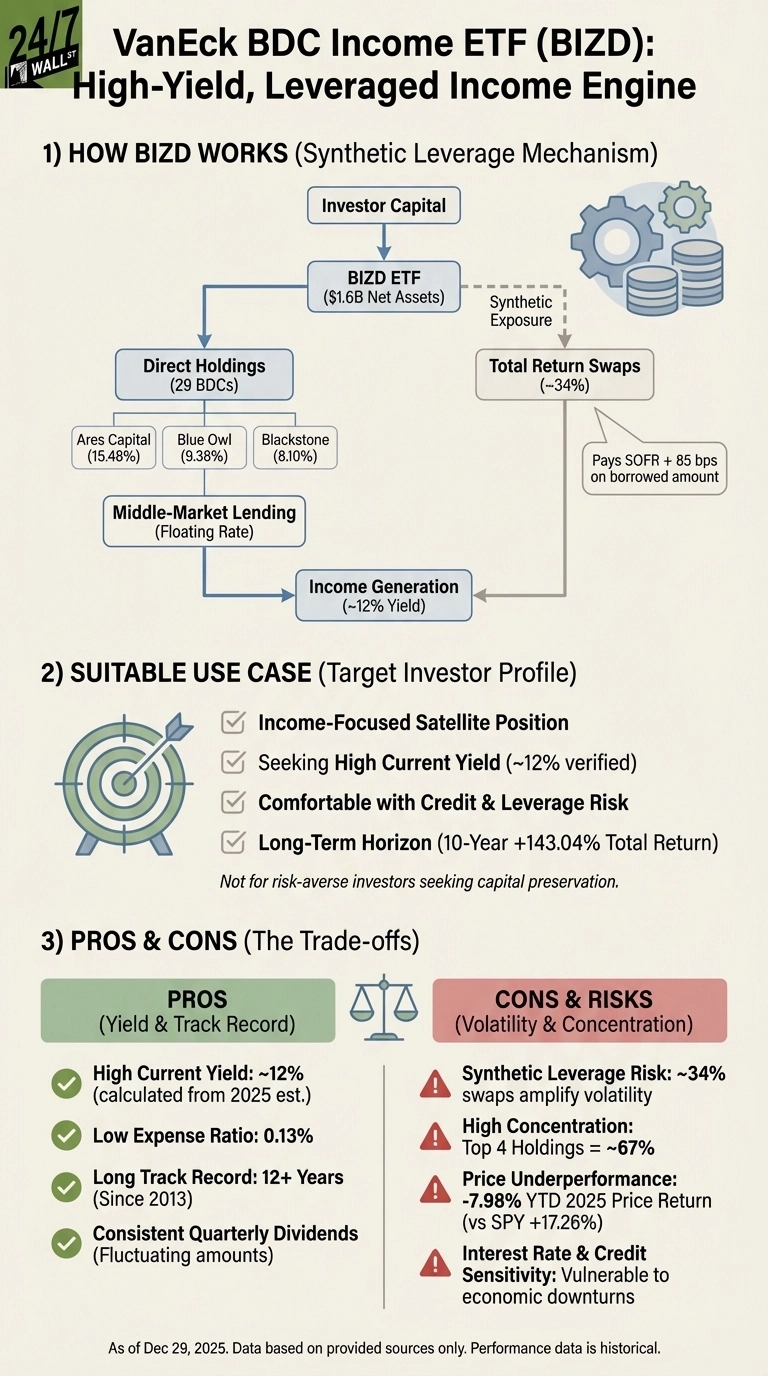

BIZD holds 29 individual BDCs plus total return swaps representing 34% of the portfolio. These synthetic positions provide leveraged exposure to BDC indexes while paying SOFR plus 85 basis points on the borrowed amount, amplifying returns in both directions.

The fund concentrates heavily in its top holdings. Ares Capital commands 15.5% of the portfolio, Blue Owl Capital 9.4%, and Blackstone Secured Lending 8.1%. Combined with swap positions, the top four exposures represent roughly two-thirds of assets. BIZD’s performance hinges on a handful of large BDCs performing well.

One Reddit investor in the r/dividends community raised concerns about the fund’s bond allocation, asking:

“What’s wrong with BIZD bonds allocation? I thought maybe it’s to reduce volatility but it fell more than PBDC that don’t have bonds at all.”

The Income Engine and Its Limits

BIZD generates its 12% yield from underlying BDC dividends, which come from interest income on middle-market loans. Most BDCs hold floating-rate debt, meaning income adjusts with interest rates. That provided a tailwind when rates rose but creates uncertainty as the Federal Reserve considers cuts.

Recent performance tells a cautionary story. The fund is down 8% year-to-date while the S&P 500 has gained 17%. Over the past decade, BIZD returned 143% compared to the S&P’s 244%. Quarterly dividends have ranged from $0.40 to $0.47 recently, showing variability as underlying BDC performance fluctuates.

The expense ratio of 0.13% is remarkably low, but the swap structure embeds additional costs through the SOFR-plus spread that don’t appear in the headline figure.

Who Should Consider This Position

BIZD fits portfolios seeking high current income from alternative credit exposure. Investors comfortable with middle-market lending risk and willing to accept price volatility for yield may find the 12% distribution attractive. The 12-year track record demonstrates dividend consistency even through market stress, though amounts fluctuate.

The fund works best as a satellite holding rather than core income position. Its concentration and leverage mean it should represent a modest allocation for investors diversifying beyond traditional bonds and dividend stocks.

Clear Risks to Understand

Three material tradeoffs accompany the high yield. First, swap-based leverage amplifies both gains and losses, adding volatility beyond individual BDC holdings. Second, concentration in the top four positions means idiosyncratic risk at Ares Capital or Blue Owl Capital directly impacts returns. Third, BDC dividends depend on portfolio company performance, and economic downturns that stress middle-market borrowers flow through to distributions.

Investors seeking capital appreciation or principal preservation should avoid BIZD. The 8% year-to-date decline demonstrates how quickly gains from yield can evaporate.

A Simpler Alternative Worth Considering

The Putnam BDC Income ETF (NYSEARCA:PBDC) offers similar BDC exposure without synthetic leverage. PBDC takes an actively managed approach to BDC selection. The fund holds 24 positions with less concentration than BIZD and no total return swaps.

PBDC’s active management allows tactical adjustments as credit conditions change, potentially smoothing returns during stress periods. The tradeoff is a shorter three-year track record compared to BIZD’s 12 years and slightly higher portfolio turnover at 31% versus 17%.

BIZD delivers on its 12% yield promise but requires accepting leverage, concentration, and significant price volatility in exchange for that income.