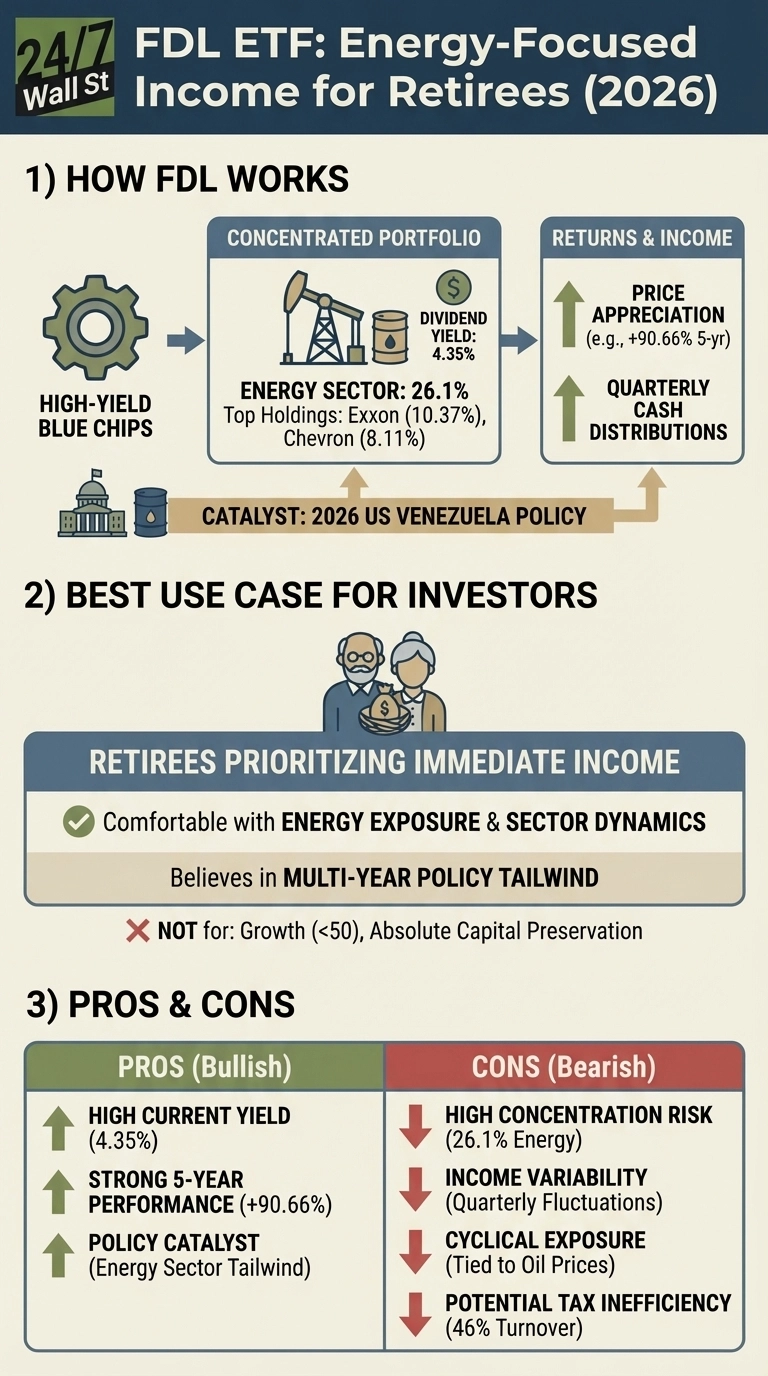

When retirement income depends on dividends that actually arrive, sector concentration stops being a flaw and starts looking like conviction. The First Trust Morningstar Dividend Leaders Index Fund (NYSEARCA:FDL | FDL Price Prediction) dedicates 26% of its portfolio to energy stocks at a moment when the Trump administration has announced indefinite control over Venezuelan oil sales. That timing matters for retirees seeking both income and appreciation in 2026.

An Energy Bet Disguised as a Dividend Fund

FDL delivers a 4.35% yield through concentrated positions in high-dividend blue chips. Exxon Mobil and Chevron alone represent 18.5% of the fund, with energy claiming over a quarter of total assets. Compare that to Vanguard High Dividend Yield ETF (NYSEARCA:VYM), where energy accounts for just 8.3% and no single sector exceeds 21%. FDL’s 0.43% expense ratio sits between passive and active strategies.

The return engine runs on actual cash distributions from mature, profitable companies. FDL paid $1.79 per share in 2025, up 5.6% from the prior year. Quarterly payments fluctuate from $0.36 to $0.55 based on underlying portfolio dividend timing. Over five years, the fund gained 91%, edging out the S&P 500’s 84% while generating significantly more income.

The Venezuela Catalyst

Energy Secretary Chris Wright confirmed January 7 that the U.S. will market Venezuelan crude indefinitely, with proceeds settling in U.S.-controlled accounts. Venezuela holds the world’s largest proven oil reserves but currently produces only 800,000 barrels daily. The administration’s plan redirects this supply from China to American markets and invites U.S. oil companies to rebuild Venezuelan infrastructure.

For FDL’s top holdings, this creates multiple tailwinds. Exxon and Chevron could access new reserves, benefit from redirected supply flows, and potentially participate in infrastructure rebuilding. The policy shift supports oil prices by maintaining supply discipline while opening long-term growth opportunities.

The Concentration Tax

Retirees accepting FDL’s 26% energy weighting must understand the tradeoffs. Energy stocks move with commodity prices, geopolitical events, and production cycles. When oil falls, FDL’s income advantage shrinks as capital losses offset distributions. The fund’s 46% annual turnover suggests active rebalancing but also potential tax inefficiency in taxable accounts.

Dividend growth has been modest at 5.6% annually, lagging inflation in some periods. Quarterly payment variability complicates budgeting for retirees drawing fixed monthly expenses. VYM’s more stable quarterly distributions and broader diversification may suit conservative income planners better, despite its lower 2.4% yield.

Wrong Tool for These Jobs

Growth-focused investors under 50 should skip FDL entirely. The 4.35% yield creates tax drag in accumulation years, and energy concentration limits participation in technology-driven market rallies. Retirees requiring absolute capital preservation cannot accept 26% exposure to a cyclical sector, regardless of current policy tailwinds.

FDL works best for retirees who need income now, understand energy sector dynamics, and believe the Venezuela policy shift creates a multi-year tailwind, but the 26% energy concentration means this fund rises and falls with oil prices regardless of how many other dividend payers it holds.