When bond yields were near zero a few years ago, retirees hunting for income had to venture into riskier territory. Now that high-yield bonds are delivering around 7% while rates remain elevated, the question shifts: is this the right kind of risk for someone living off their portfolio?

Built for Income With a Safety Net

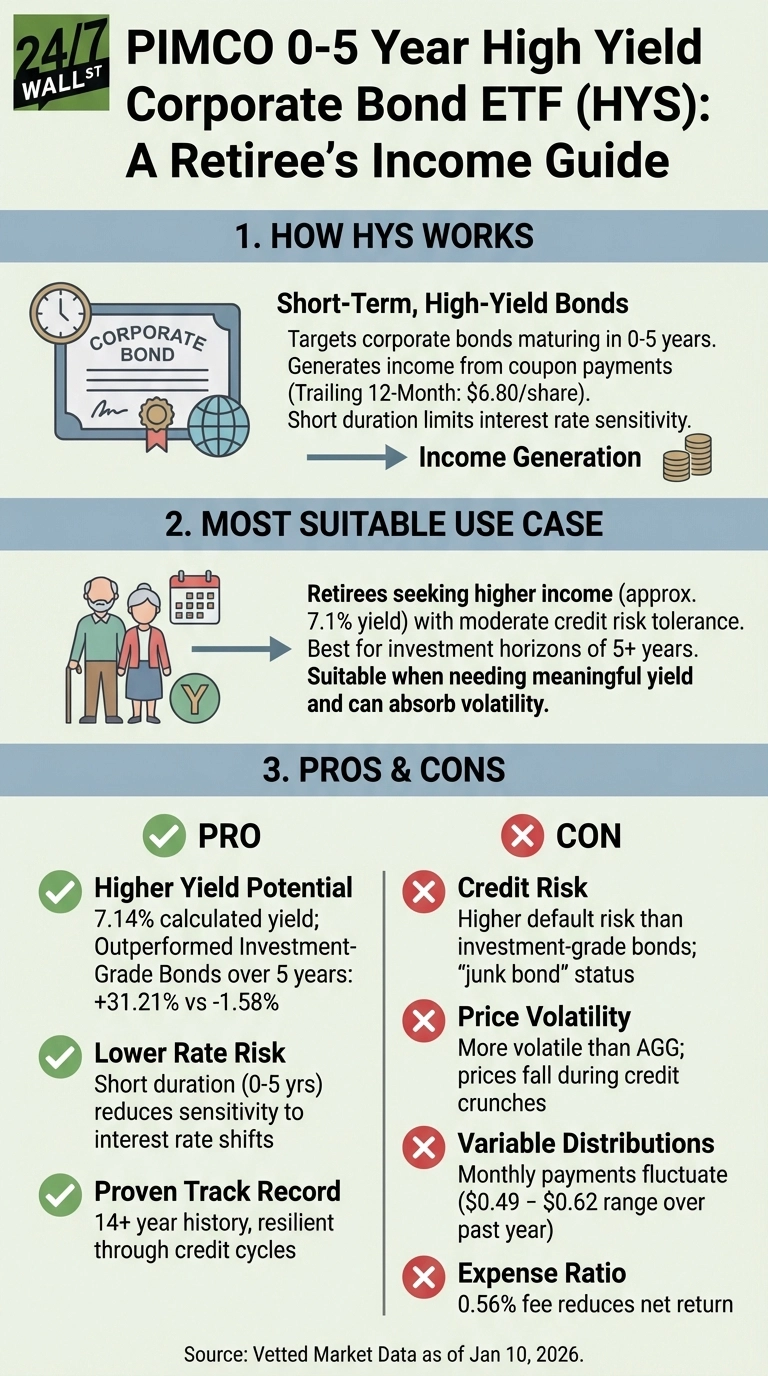

PIMCO 0-5 Year High Yield Corporate Bond Index Exchange-Traded Fund (NYSEARCA:HYS) targets high-yield corporate bonds maturing within five years. The short duration limits sensitivity to interest rate swings. While these bonds carry credit risk (rated below investment grade), their brief maturity means more predictable pricing even when the Fed shifts policy.

The fund generates income from bond coupon payments, currently distributing around $6.80 annually per share. Based on the recent price near $95, that translates to roughly 7.1% yield.

Does It Deliver on the Promise?

With $1.5 billion in assets and a 14-year track record, HYS has proven resilient through multiple credit cycles. Over five years, HYS returned 31% while investment-grade bonds (AGG) lost 1.6%. That outperformance reflects the yield advantage of high-yield debt during a period when rate volatility punished longer-duration bonds.

The fund fulfills its mandate of delivering steady income with controlled rate risk, but retirees expecting equity-like growth will be disappointed.

The Tradeoffs You’re Accepting

Credit risk is the primary concern. High-yield bonds earn their nickname (junk bonds) because issuers have weaker balance sheets. During recessions or credit crunches, defaults rise and prices fall. The short maturity helps but doesn’t eliminate this risk.

The 0.56% expense ratio is reasonable for active management but higher than broad bond index funds. That cost compounds over time, eating into net yield. Monthly distributions vary from $0.49 to $0.62, which can complicate budgeting for those relying on consistent income.

Who Should Avoid HYS

Conservative retirees who prioritize capital preservation over yield should skip this fund. The credit risk and price volatility, while muted compared to longer-duration high-yield funds, still exceed what investment-grade bonds offer.

Retirees with shorter time horizons (under five years) should also think twice. If you need to liquidate during a credit market downturn, you could face losses that erode your principal at the wrong time.

A Lower-Cost Alternative Worth Considering

The Janus Henderson AAA CLO ETF (NYSEARCA:JAAA | JAAA Price Prediction) offers a different approach to income generation. With a 5.3% yield and a 0.20% expense ratio, JAAA invests in AAA-rated collateralized loan obligations rather than junk bonds. The lower yield reflects higher credit quality, and the dramatically lower fee structure means retirees keep more of what they earn. For those willing to trade some yield for better credit ratings and lower costs, JAAA presents a compelling alternative.

HYS works best for retirees who need meaningful income, understand credit risk, and have other assets to cushion potential downturns, but the premium yield comes with volatility that not every retirement portfolio can absorb.