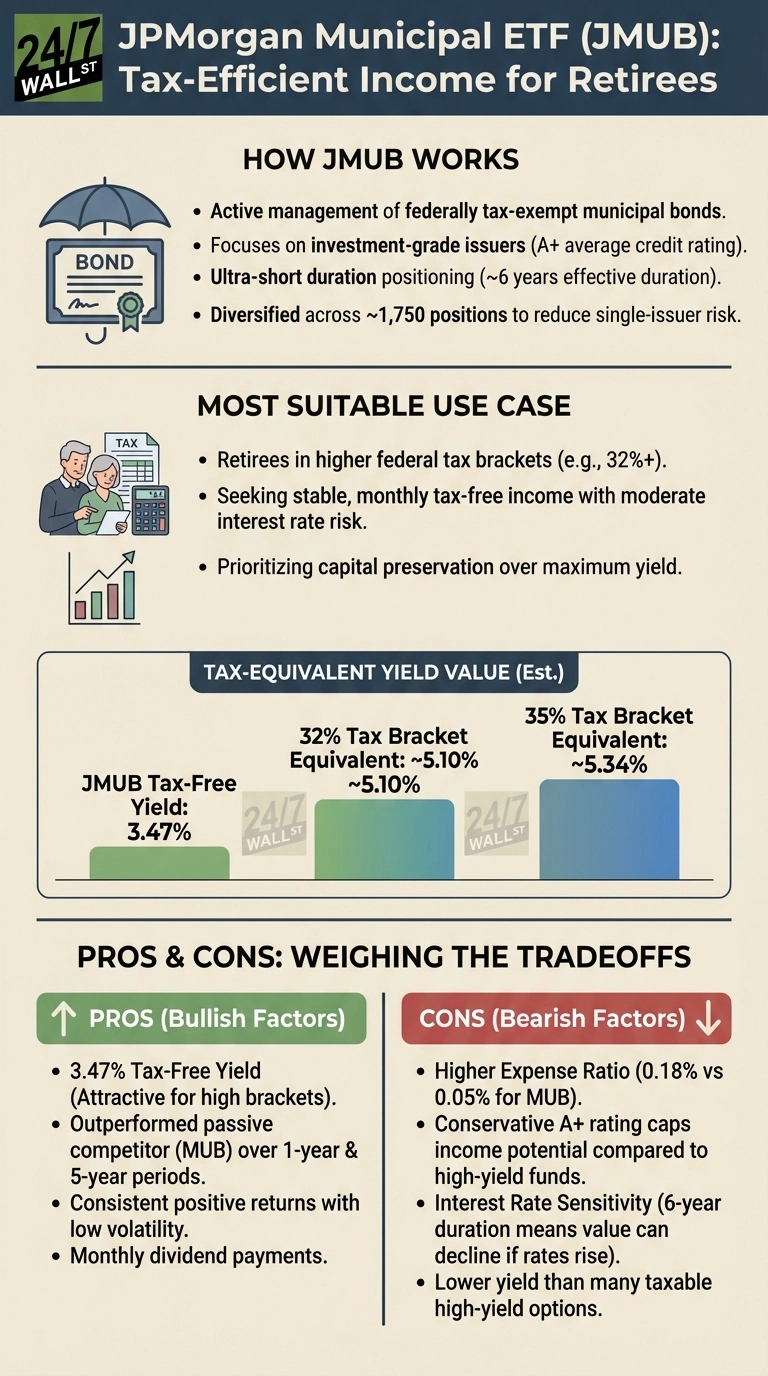

When retirees face higher tax brackets from pension income, Social Security, and portfolio withdrawals, every percentage point of yield eaten by taxes matters. JPMorgan Municipal Bond ETF (NASDAQ:JMUB | JMUB Price Prediction) addresses this challenge through federally tax-exempt municipal bond income. For retirees in the 32% bracket, the fund’s 3.5% yield delivers the equivalent purchasing power of a 5.1% taxable return. This tax efficiency became even more accessible following a 2025 merger that created the largest active municipal bond ETF with enhanced liquidity and scale.

What JMUB Does for Tax-Conscious Income Seekers

JMUB generates monthly tax-free income while preserving capital through a balanced approach to credit quality and duration. The fund maintains an A+ average credit rating by focusing on investment-grade issuers, avoiding the default risks that come with reaching for yield in lower-rated municipal debt. With roughly six years of effective duration, the fund occupies a sweet spot that offers more yield than money market funds while remaining less volatile than long-duration portfolios. This positioning makes sense for retirees who need income stability without excessive interest rate sensitivity.

Municipal bonds pay interest exempt from federal taxes, and JPMorgan’s active management adjusts credit quality and duration based on relative value opportunities. The fund holds approximately 1,750 positions across state and local government debt, providing broad diversification that reduces single issuer default impact.

Performance Tells a Nuanced Story

JMUB’s five-year track record demonstrates how active management can add value in municipal bonds. The fund’s credit selection and duration positioning delivered a 6.3% return over that period, outpacing the passive iShares National Muni Bond ETF by over 200 basis points. This outperformance continued over the past year, suggesting JPMorgan’s active approach justified the higher 0.18% expense ratio for investors seeking tax-efficient returns.

For retirees, the critical question isn’t whether JMUB beat benchmarks, but whether tax-free income justifies the tradeoff. For someone in the 32% bracket, JMUB’s 3.5% yield equals 5.1% on a taxable basis, making it competitive with many taxable bond funds.

The Tradeoffs You Accept

JMUB’s conservative approach prioritizes safety over yield maximization. With an A+ average credit rating, the fund avoids higher-yielding but riskier municipal debt, capping income potential compared to funds that venture into BBB-rated or high-yield municipal bonds. The six-year effective duration means JMUB will decline if interest rates rise meaningfully, though less dramatically than longer-duration funds.

The 0.18% expense ratio costs 13 basis points more annually than MUB. While this difference seems small, it compounds over the decades-long retirement horizons many investors face. The fund’s active management also generates 39% annual portfolio turnover, which can create tax consequences in taxable accounts, though the municipal bond interest itself remains federally tax-exempt.

Who Should Avoid JMUB

Retirees in the 12% or lower federal tax bracket gain little from tax-exempt income. Taxable bond funds offering higher pre-tax yields would deliver better after-tax returns. Investors seeking maximum current income should look elsewhere. JMUB’s 3.5% yield trails many high-yield municipal funds and dividend-focused equity ETFs.

Consider MUB as a Lower-Cost Alternative

The iShares National Muni Bond ETF (NYSEARCA:MUB) offers similar exposure with a 0.05% expense ratio and $41.5 billion in assets. MUB’s 3.4% yield nearly matches JMUB’s 3.5%, and its passive approach tracking the Bloomberg Municipal Bond Index costs 73% less annually. While JMUB has outperformed over recent periods, MUB’s lower fees and deeper liquidity make it worth considering for retirees who prefer index-based municipal bond exposure.

JMUB works best for higher-bracket retirees seeking tax-efficient income with moderate interest rate risk, but the tax benefit only matters if you’re paying meaningful federal taxes on investment income.