If you’ve looked at the price chart for the JPMorgan Ultra-Short Income ETF (NYSEARCA:JPST | JPST Price Prediction), you’ve probably noticed something odd. The chart looks jagged and volatile, with regular drops creating a staircase pattern. But this visual volatility is actually a feature, not a bug, revealing exactly why this ETF works well for retirees seeking steady income.

The Chart Mystery Explained

The dramatic appearance comes from JPST’s monthly dividend distributions. Each month, when the fund pays its dividend, the share price drops by that amount on the ex-dividend date, creating 12 visible “steps down” annually on unadjusted charts. Actual price volatility is minimal, with daily movements of just pennies. The fund’s adjusted returns show the real story: stable total returns combining modest price appreciation with consistent income.

What JPST Actually Does

JPST functions as a sophisticated cash alternative by investing in ultra-short duration, investment-grade debt securities. The fund collects interest payments from these holdings and passes that income to shareholders monthly, creating a predictable income stream. The fund’s massive $35.4 billion in assets provides institutional scale that drives down costs to just 0.18% annually, meaning more of the interest income flows to investors rather than being consumed by fees.

Monthly Income for Predictable Cash Flow

Retirees benefit from JPST’s monthly distribution schedule, which provides regular cash flow for living expenses. This consistency matters when drawing income rather than accumulating wealth. The distributions track short-term interest rates closely, so as the Federal Reserve adjusts policy, JPST’s yield responds accordingly, though the underlying share price remains remarkably stable compared to longer-duration bond funds.

The Tradeoffs You’re Accepting

JPST isn’t a growth vehicle. Nearly all gains come from income rather than price appreciation, with modest capital gains over time. You’re also accepting rate sensitivity in the opposite direction most investors worry about. If the Fed cuts rates aggressively, JPST’s yield will decline, reducing your income stream.

Additionally, those monthly distributions create monthly taxable events. Unless you hold JPST in a tax-advantaged account like an IRA, you’ll owe taxes on that income annually, making it less efficient in taxable accounts.

Who Should Avoid This ETF

If you’re a younger investor with a 20-plus year time horizon, JPST doesn’t belong in your portfolio. The opportunity cost of earning income-focused returns when equities historically deliver higher long-term growth is substantial over decades. If you’re seeking inflation protection or real wealth building, ultra-short income strategies won’t keep pace with rising costs over time.

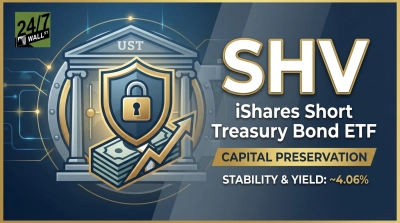

Consider SHV as an Alternative

The iShares Short Treasury Bond ETF (NASDAQ:SHV) offers a more conservative approach for investors who prioritize Treasury backing above all else. SHV’s exclusive focus on U.S. Treasury bills provides maximum safety, though this comes at a cost: the fund currently delivers lower income than JPST. This yield difference reflects a fundamental tradeoff—investors choosing SHV pay a premium for Treasury-only exposure, while JPST investors accept broader investment-grade credit exposure in exchange for higher income.

JPST serves retirees exceptionally well as a cash alternative that generates monthly income with minimal price volatility, though the visual chart appearance and modest yield sensitivity to Fed policy are tradeoffs to understand before investing.