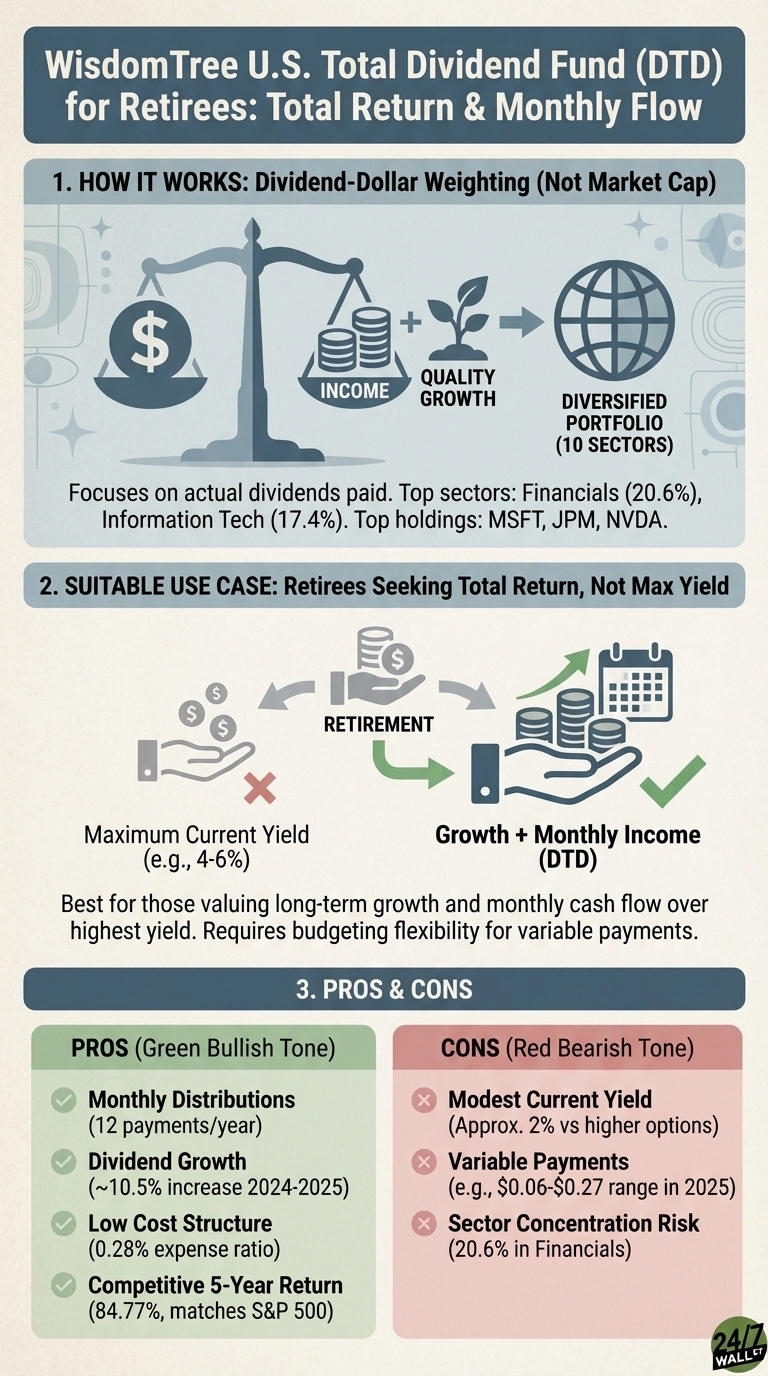

Retirees face a dilemma: they need income today but can’t afford to sacrifice growth for tomorrow. Most dividend strategies force a choice between high current yield and capital appreciation. WisdomTree U.S. Total Dividend Fund (NYSEARCA:DTD) attempts to solve this by weighting holdings based on actual dividend dollars paid rather than market capitalization, creating a portfolio that balances income with quality.

Built for Total Return, Not Just Yield

DTD’s role in a retirement portfolio centers on delivering competitive total returns alongside regular income. The fund’s dividend-weighting methodology naturally tilts toward companies paying substantial dividends without chasing the highest yields, which often signal financial distress. This approach has produced a 10-year return of 204% while maintaining a nearly 2% yield and monthly distribution schedule.

The return engine combines dividend income with capital appreciation from quality dividend growers. Unlike market-cap-weighted funds that concentrate in mega-cap tech stocks with minimal yields, DTD allocates 20.6% to Financials and limits Information Technology to 17.4%. Top holdings include Microsoft (NASDAQ:MSFT | MSFT Price Prediction), JPMorgan Chase (NYSE:JPM), and NVIDIA (NASDAQ:NVDA), companies that have consistently raised dividends while delivering price appreciation. The fund distributed $1.69 per share in 2025, up 10.5% from $1.53 in 2024, demonstrating dividend growth that helps retirees maintain purchasing power.

Performance Meets Expectations

DTD has largely fulfilled its promise of matching broad market returns while providing superior income. The fund’s five-year return of 84.8% essentially matches the S&P 500’s 85.1%, while delivering roughly double the yield. Over 10 years, DTD returned 204% versus the S&P 500’s 232%, a reasonable tradeoff for investors prioritizing current income. The 0.28% expense ratio and 17% portfolio turnover keep costs low and tax efficiency high, important considerations for retirees in taxable accounts.

The Tradeoffs Retirees Accept

Monthly distributions vary significantly, ranging from $0.06 to $0.27 in 2025, with December typically including year-end special distributions. Retirees accustomed to fixed pension checks need flexibility in their budgeting. The fund’s 20.6% Financial sector allocation creates concentration risk, as bank dividends can face pressure during economic downturns. Additionally, the nearly 2% yield falls short for retirees seeking maximum current income, as some high-dividend ETFs offer 4% to 6% yields.

Who Should Avoid DTD

Retirees requiring predictable monthly income of a fixed amount will struggle with DTD’s variable distributions. Those needing maximum current yield to cover living expenses should consider higher-yielding alternatives. The fund suits retirees with supplemental income sources who can tolerate payment fluctuations in exchange for dividend growth and capital appreciation potential.

Consider SCHD for Dividend Quality

Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) offers a compelling alternative with a 3.8% yield and 0.06% expense ratio. SCHD screens for dividend quality and growth rather than simply weighting by dividend dollars, resulting in more consistent payments and lower concentration in Financials. The higher yield provides more immediate income, though SCHD’s returns have slightly lagged DTD’s over longer periods.

DTD works best for retirees seeking total return with monthly cash flow rather than maximum current income, but the variable payment structure requires financial flexibility most fixed-income retirees lack.