When bond investors chase yield, they often overlook the engine that drives total returns: price appreciation from interest rate movements. The iShares MBS ETF (NYSEARCA:MBB | MBB Price Prediction) demonstrates this dynamic perfectly. While its 4% yield attracts income seekers, the fund has benefited from mortgage-backed securities price movements in recent periods.

What MBB Actually Does

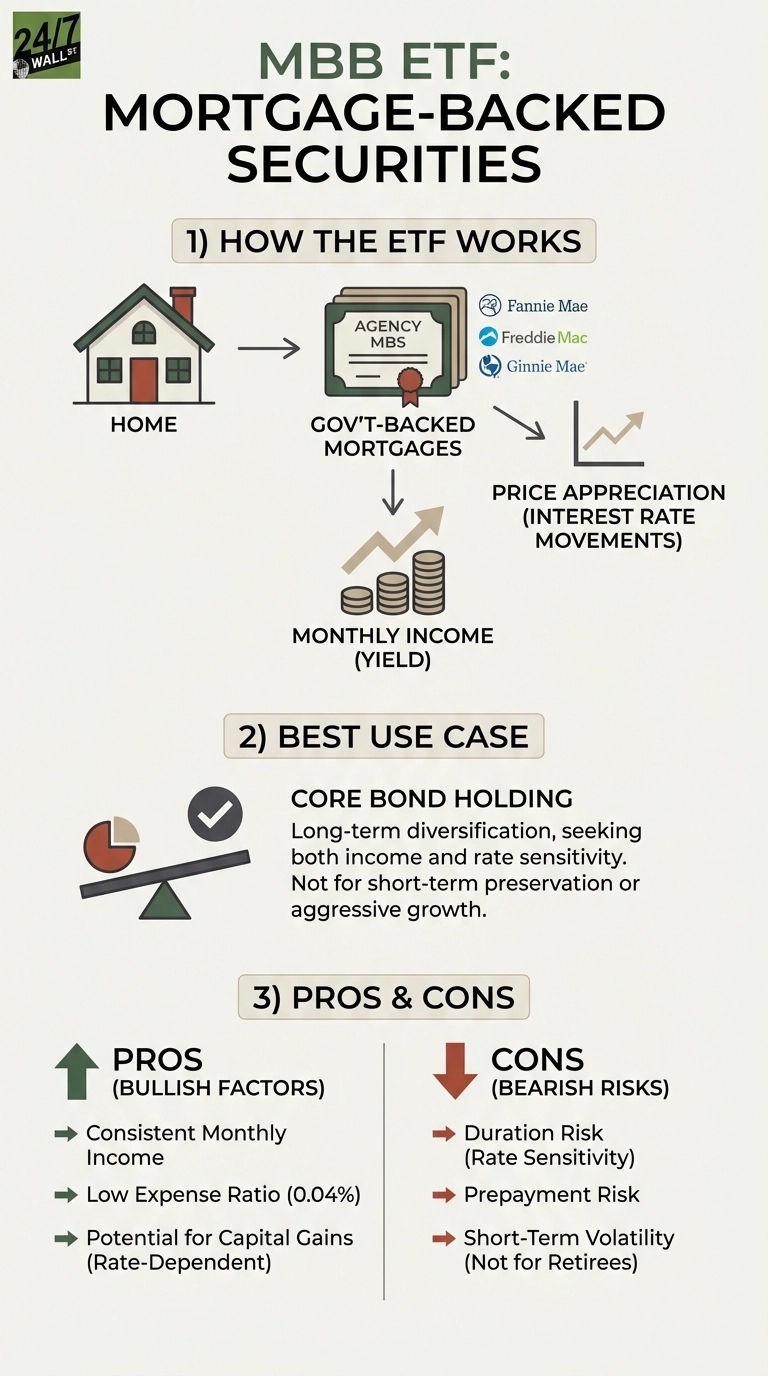

MBB provides exposure to agency mortgage-backed securities, the bonds backed by Fannie Mae, Freddie Mac, and Ginnie Mae. These aren’t the risky subprime mortgages from 2008. They carry implicit or explicit government guarantees, eliminating credit risk. What remains is interest rate sensitivity and prepayment risk.

MBB’s scale creates meaningful advantages for investors. The fund manages $39 billion in assets, allowing institutional-level efficiency that translates to a 0.04% expense ratio among the lowest in fixed income. This cost structure compounds over time, ensuring more mortgage interest flows through as monthly dividends rather than being consumed by fees.

The Return Engine Beyond Yield

The past year illustrates how MBB generates returns beyond its yield. The fund delivered strong total returns, with the majority coming from price appreciation as mortgage spreads compressed. This demonstrates the dual benefit: steady monthly income from the 4% yield combined with capital gains when rate environments cooperate.

The Tradeoffs You Accept

Duration cuts both ways, and MBB’s track record shows this clearly. The fund has delivered strong performance in recent periods and over the long term, but experienced challenges during the 2022 rate spike. When the Federal Reserve aggressively tightened policy, bond values compressed across the market, illustrating how duration risk materializes during hiking cycles.

Prepayment risk also matters. When rates fall sharply, homeowners refinance, returning principal to MBB earlier than expected. The fund must reinvest at lower yields, dampening future income. This caps upside in aggressive rate-cutting scenarios.

Who Should Avoid This

Investors with short time horizons or those prioritizing capital preservation should look elsewhere. MBB can swing 2% to 3% in a month during rate volatility. Retirees who need stable principal values may find this unsettling, even with monthly income.

Growth-focused investors will also find MBB limiting. Over longer periods, this fixed-income allocation tool serves portfolio diversification rather than wealth-building objectives, making it unsuitable for those seeking equity-like growth.

Consider Vanguard’s Lower-Cost Alternative

Cost-conscious investors should examine Vanguard’s alternative. The Vanguard Mortgage-Backed Securities ETF (NASDAQ:VMBS) charges 0.03% annually, undercutting MBB by one basis point. While this difference appears trivial, it compounds meaningfully over decades—a $100,000 allocation held 30 years saves approximately $3,000 in cumulative fees, making VMBS worth considering for buy-and-hold investors.

MBB works best as a core bond holding for investors who understand that mortgage-backed securities deliver returns through both income and rate sensitivity, but only when rates cooperate and prepayment risk stays contained.