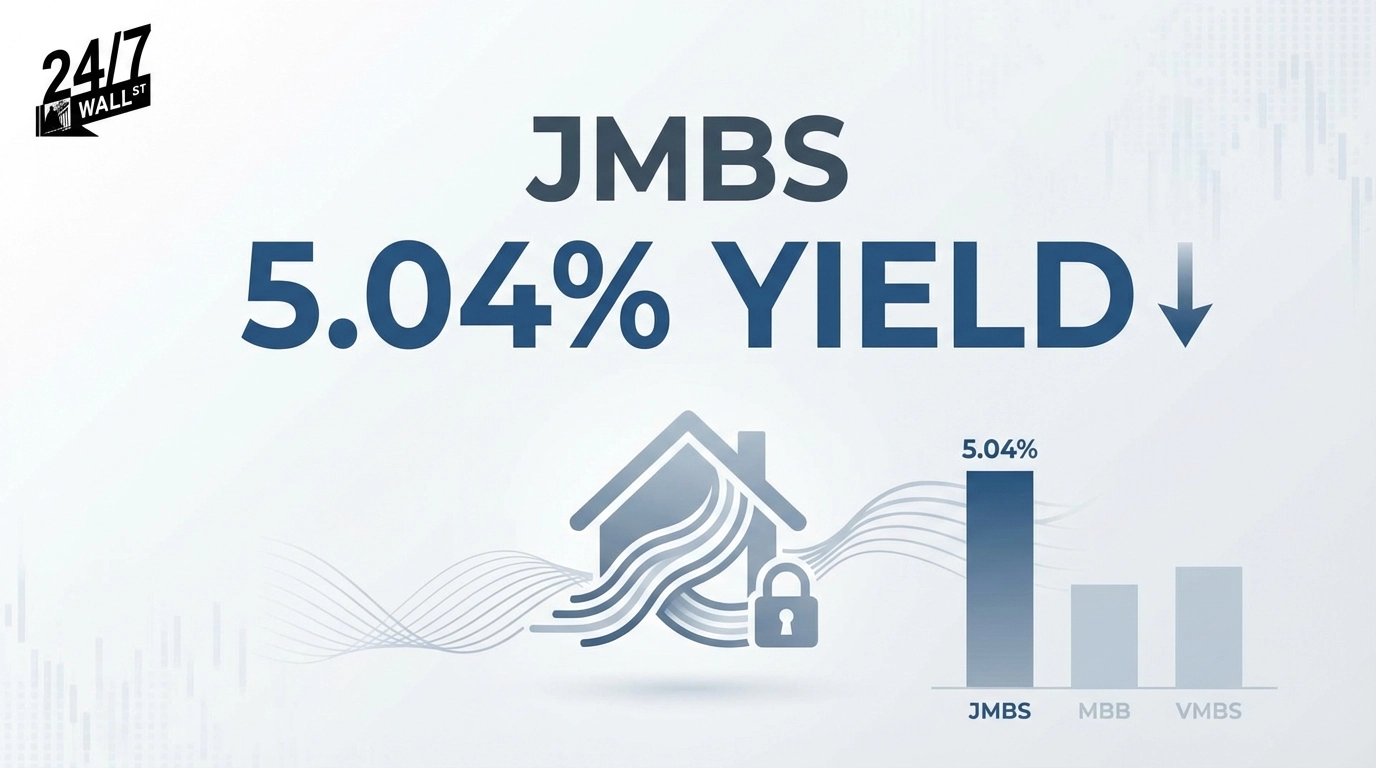

The Janus Henderson Mortgage-Backed Securities ETF (NYSE:JMBS | JMBS Price Prediction) offers retirees a monthly income stream with a 5.04% yield, positioning itself as a compelling alternative to traditional bond funds. Unlike equity-based income strategies that expose investors to market volatility, JMBS generates its yield from coupon payments on agency and investment-grade mortgage-backed securities. These are pools of residential mortgages, primarily backed by Fannie Mae and Freddie Mac, providing an additional layer of security.

The ETF’s income comes from homeowners making monthly mortgage payments. As these payments flow through to the fund, JMBS distributes them to shareholders as monthly dividends. This structure creates predictable cash flow that retirees can count on, with the fund maintaining an unbroken payment history since its 2018 inception.

Evaluating Dividend Sustainability

JMBS has demonstrated remarkable dividend resilience through varying interest rate environments. Monthly distributions have remained stable, recently paying around $0.20 per share. This consistency reflects the fund’s professional management approach, with a team possessing deep mortgage market expertise overseeing the portfolio’s strategy and security selection.

The fund’s dividend safety rests on several factors. First, the underlying securities are predominantly agency-backed, meaning the U.S. government effectively guarantees the principal and interest payments. This eliminates most credit risk. Second, the current interest rate environment supports robust income generation. With mortgage rates elevated compared to 2020-2021, prepayment risk remains low as homeowners have little incentive to refinance, creating more stable cash flows.

JMBS carries a 0.22% expense ratio, reflecting its active management strategy. While higher than passive alternatives, this approach has enabled the fund to deliver a 5.04% yield – meaningfully above comparable passive MBS funds. For retirees, this yield advantage translates into tangible additional income that can help cover living expenses without depleting principal, justifying the active management premium for investors prioritizing cash flow generation.

Retirees need both income and capital preservation – making total return a critical metric beyond just yield. JMBS has delivered strong performance, combining price appreciation with its distribution payments. The fund has also outperformed the broad bond market over a five-year period, demonstrating its ability to generate returns across different market conditions.

The primary risk is interest rate sensitivity. If rates decline significantly, increased refinancing activity could reduce the fund’s income stream. Conversely, if rates spike, the fund’s net asset value could temporarily decline, though higher yields would eventually benefit distributions.

Alternative Income Option

Investors seeking similar exposure might consider the Vanguard Mortgage-Backed Securities ETF (NASDAQ:VMBS), which offers a rock-bottom 0.03% expense ratio and 3.96% yield. While VMBS delivers lower current income than JMBS, its minimal fees preserve more capital over time. The fund provides access to the same agency MBS market with Vanguard’s index-tracking approach, making VMBS an efficient core holding for cost-conscious retirees who prioritize expenses over maximizing yield.