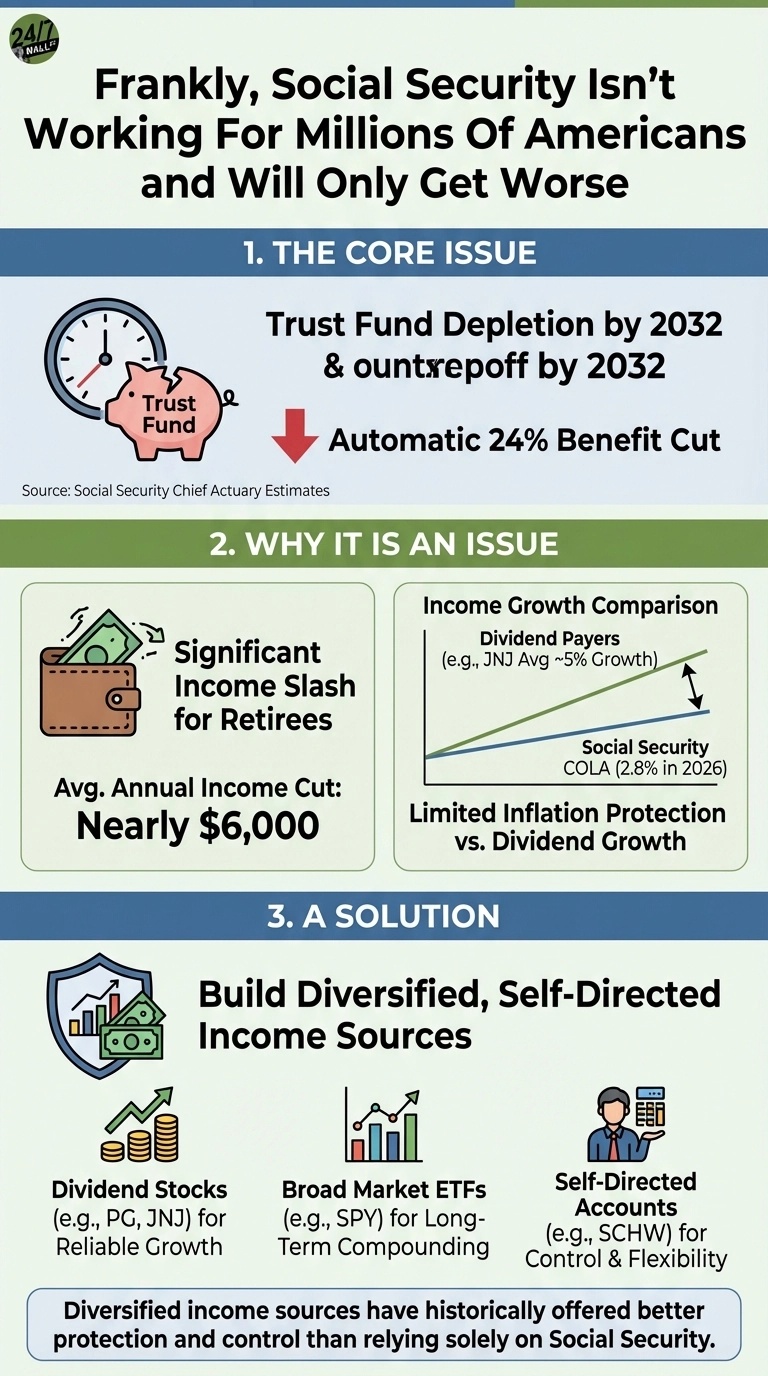

Social Security faces a fundamental problem that millions of Americans will soon confront directly. The program’s retirement trust fund is projected to deplete by late 2032, just seven years away, according to estimates from the Social Security Chief Actuary. When that happens, the law requires an automatic 24% benefit cut across the board unless Congress acts first.

The average retiree’s monthly check of approximately $2,071 represents their primary income source in 2026. When the trust fund depletes in 2032, that dependence becomes dangerous—the automatic 24% benefit cut would slash annual income by nearly $6,000, forcing difficult choices about healthcare, housing, and basic expenses. This vulnerability stems from Social Security’s structure as a defined benefit plan that depends entirely on political decisions rather than individual control.

Why the Current Structure Creates Risk

The 2026 cost-of-living adjustment illustrates a deeper issue. Benefits increased just 2.8% this year, barely keeping pace with essential expenses. Meanwhile, established dividend payers like Johnson & Johnson and Procter & Gamble have grown their payouts at rates averaging around 5% annually, demonstrating how different income sources have performed historically in protecting purchasing power over time.

The difference matters because defined benefit plans like Social Security lack flexibility. Recipients cannot control when benefits start without permanent reductions, cannot adjust for individual circumstances, and face political risk with every budget cycle. Financial advisors note that retirees with self-directed retirement accounts have adaptability that a government program cannot match.

How Different Income Sources Compare

Dividend income provides a different kind of security than government benefits. A retiree who built a $350,000 position in Procter & Gamble receives roughly $10,000 annually in dividends that have grown consistently for over six decades, demonstrating how private income streams have historically provided inflation protection that government adjustments have not matched.

Broad market exposure offers a different wealth-building approach than fixed income. The S&P 500 ETF has delivered substantial long-term returns, demonstrating how equity ownership compounds wealth over decades. While the current yield appears modest at around 1%, the total return over time has historically provided accumulation that fixed benefits cannot match.

The fundamental issue is that Social Security was designed for a different demographic reality. Longer lifespans and fewer workers per retiree create mathematical challenges no COLA adjustment can solve. Self-directed accounts through platforms like Charles Schwab give retirees control over asset allocation, withdrawal timing, and investment selection—flexibility that becomes critical when government benefits face uncertain futures.

Social Security will likely continue in some form, but relying on it exclusively means accepting whatever benefits politicians decide to provide. The data shows that retirees with diversified income sources have historically experienced different outcomes than those relying solely on Social Security’s fixed payments.