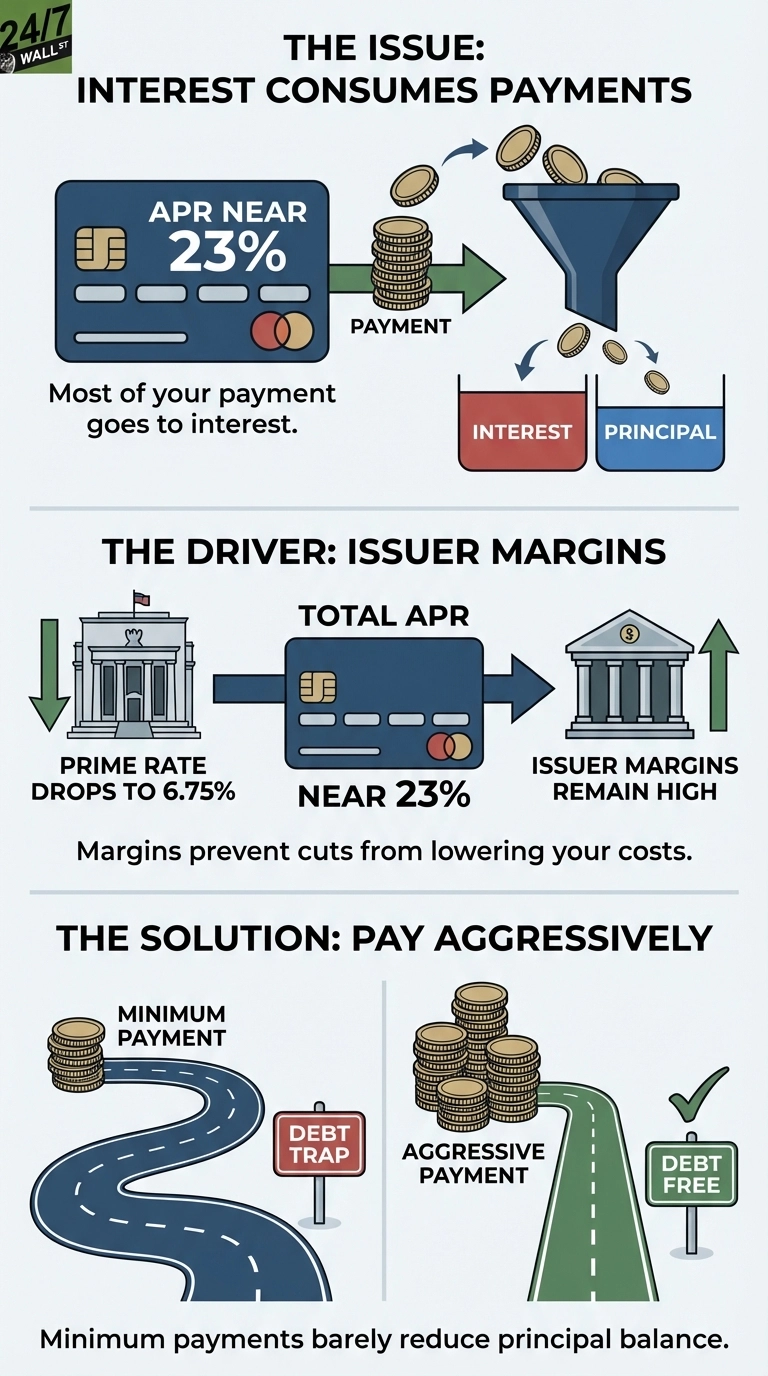

Credit card debt has reached crisis levels, with the average American cardholder now owing $7,886. When combined with interest rates near 23%, this creates a situation where monthly interest charges consume most payments, making it nearly impossible to reduce the actual balance owed.

Why Credit Card Rates Stay High When the Fed Cuts

The Federal Reserve cut rates multiple times throughout 2025, yet credit card holders haven’t seen meaningful relief. The reason is simple: while the prime rate dropped to 6.75%, card issuers maintain substantial margins that keep total APRs near 23%. These issuer margins act as a buffer that prevents Fed rate cuts from translating into lower costs for consumers.

Credit cards use daily compounding, which means interest builds on itself every 24 hours rather than monthly. This mathematical reality transforms what looks like a manageable annual rate into a powerful wealth drain. A cardholder with $5,000 in debt faces roughly $95 in monthly interest charges before touching the principal balance.

The Minimum Payment Trap

Card issuers design minimum payments to feel manageable, typically requiring just 1-3% of your balance each month. But this creates a dangerous trap: on a $5,000 balance, a $100 minimum payment might seem responsible, yet nearly all of it goes to interest rather than reducing what you owe. Without aggressive payments well above the minimum, balances can take years or decades to eliminate.

What This Means for Your Finances

The most important factor is whether you’re making progress on your balance or just covering interest. Calculate your monthly interest charge by multiplying your balance by your APR, then dividing by 12. If your payment is close to or below this number, you’re not making meaningful headway. The costly mistake is assuming minimum payments represent a sustainable path forward. They don’t. At current rates, carrying a balance month-to-month can easily cost thousands in interest annually, money that could otherwise build savings or reduce other debt.

This article is for educational purposes and does not constitute personalized financial advice.