Dave Ramsey, the personal finance radio host and author, has long compared credit cards to cigarettes, calling them “the cigarette of the financial world” in his 2003 book The Total Money Makeover. His argument: both products are socially acceptable, heavily marketed, and financially destructive over time. With Americans now carrying $1.233 trillion in credit card debt and average interest rates exceeding 22%, his warning deserves a closer look.

Where Ramsey Gets It Right

The debt crisis has intensified as cardholders struggle under the weight of growing balances. The typical American now owes nearly $8,000 on their cards, and with interest rates exceeding 22%, that debt compounds rapidly. What starts as manageable monthly charges transforms into a multi-year trap when borrowers can only afford minimum payments, illustrating exactly the cycle Ramsey warns against.

The mathematics of minimum payments reveal the true danger. Recent analysis shows how a typical balance at standard interest rates can keep borrowers trapped for over a decade, with interest charges nearly doubling what they originally spent. This compound interest effect is precisely what makes the debt cycle so difficult to break.

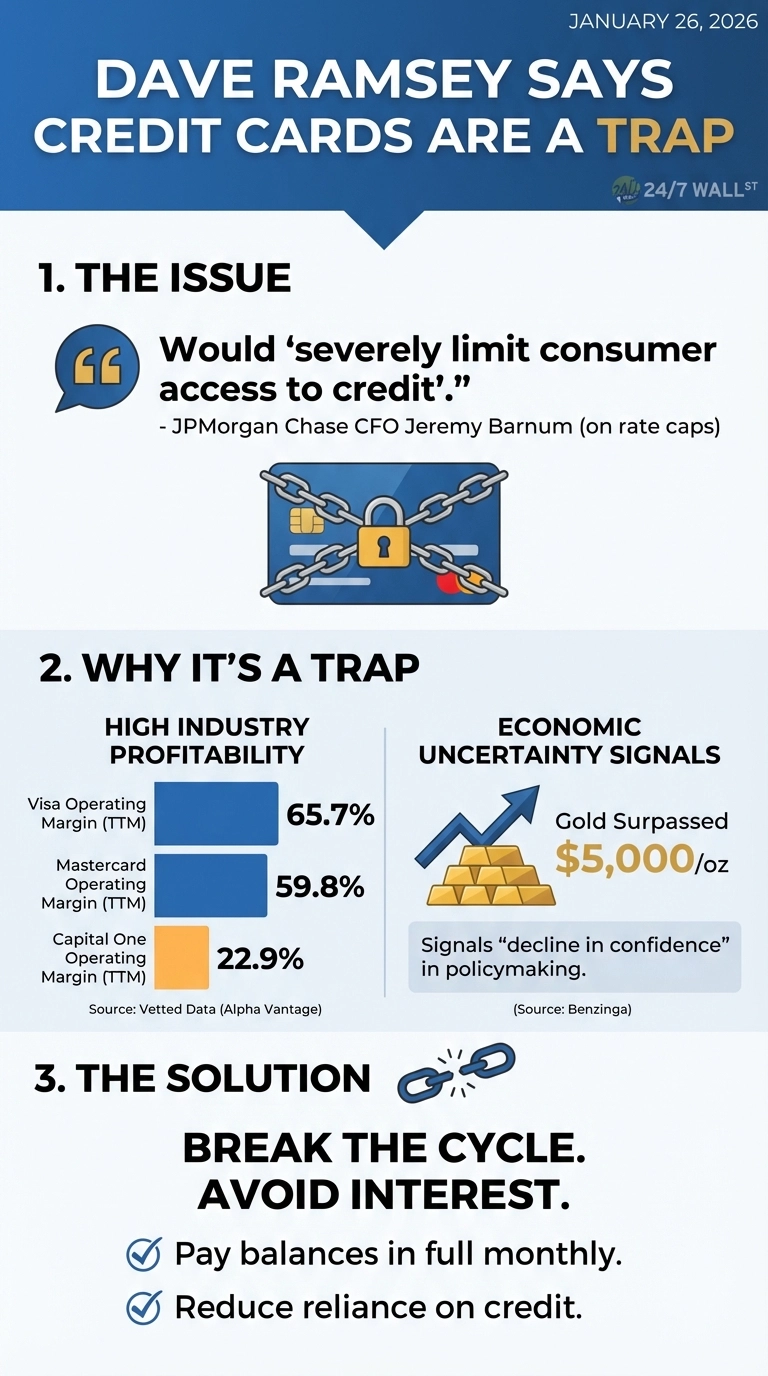

The industry’s business model depends on consumers carrying balances. Payment processors like Visa and Mastercard achieve profit margins near 50%, while card issuers extract returns above 20% from interest and fees. This profitability comes at the expense of Americans trapped in the revolving debt cycle that Ramsey criticizes.

What the Advice Oversimplifies

Ramsey’s analogy breaks down in one important way: credit cards aren’t inherently harmful. Unlike cigarettes, which damage health with every use, credit cards only become problematic when balances aren’t paid in full. Cardholders who pay monthly avoid interest entirely while earning rewards and building credit history.

The Consumer Financial Protection Bureau documented how APRs for general purpose cards climbed to 25.2% in 2024, creating an expensive burden for the millions of Americans who carry revolving balances. This rate increase reflects the growing cost of consumer credit as the Federal Reserve maintained higher interest rates throughout the period.

The Trump administration’s recent proposal for a 10% APR cap highlights another complexity: restricting credit card terms could reduce access for higher-risk borrowers, potentially pushing consumers toward less regulated lending options.

How to Think About This Advice

Ramsey’s warning works best for people who struggle with spending discipline or already carry revolving balances. If you’re paying interest month after month, his advice to cut up cards and pay cash makes practical sense. The math doesn’t lie: 22% interest compounds quickly.

But the cigarette comparison doesn’t fit cardholders who use credit strategically. The question to ask yourself: do you pay your balance in full each month? If yes, cards are tools. If no, Ramsey’s concerns about the debt trap apply directly to your situation.

Financial advice from well-known personalities often uses strong language to break through consumer complacency. Ramsey’s metaphor succeeds at that. Whether it applies to your circumstances depends entirely on how you use the product.