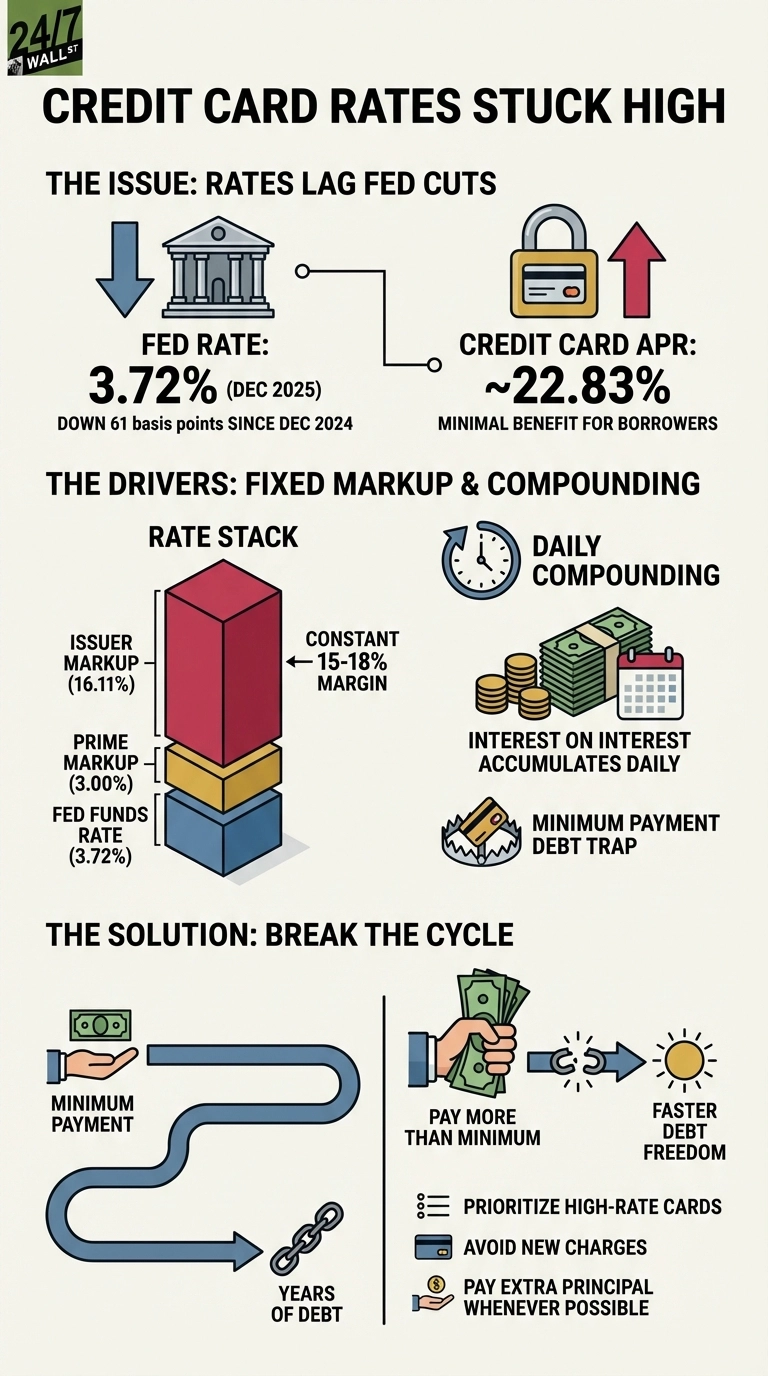

Americans collectively owe $1.233 trillion in credit card debt, with nearly half of all cardholders carrying balances month to month at an average APR of 22.83%. Despite recent Federal Reserve rate cuts, borrowers face a persistent financial squeeze because credit card issuers maintain their markup regardless of policy changes, meaning lower Fed rates don’t translate to meaningful relief for consumers paying double-digit interest on revolving debt.

The Federal Reserve cut its benchmark rate to 3.72% in December, down substantially from the 2025 peak. Yet credit card borrowers have seen minimal benefit because the structural relationship between rates remains unchanged: issuers add a consistent 15 to 18 percentage point markup over the prime rate, which itself sits about 3 percentage points above the Fed’s rate. This cascading markup structure means that even as the Fed lowers rates, the absolute cost of credit card borrowing stays elevated—the entire rate structure simply shifts downward while maintaining the same expensive gap between what the Fed charges banks and what consumers pay on their cards.

How Credit Card Interest Actually Works

Most credit cards charge variable APRs tied to the prime rate, which moves with Fed policy. When the Fed adjusts rates, the prime rate typically follows within days. Credit card rates should adjust just as quickly, but the issuer’s margin remains constant, keeping absolute rates elevated even as the Fed cuts.

The daily compounding mechanism makes credit card debt particularly expensive compared to other forms of borrowing. Card issuers apply interest charges every single day to your average balance, meaning a typical $5,000 balance accumulates over $3 in new interest daily. This creates a compounding effect where interest accumulates on previous interest, accelerating debt growth faster than many borrowers expect.

Minimum payments create a debt trap that’s difficult to escape. Consider a $5,000 balance with a typical $150 minimum payment: the majority of that payment goes to interest rather than principal, meaning the balance declines painfully slowly while total interest paid over time can exceed the original amount borrowed. This structure isn’t accidental—it’s precisely how issuers profit from revolving debt, keeping borrowers paying interest for years on purchases long forgotten.

Why Rates Stay High Despite Fed Cuts

Credit card lending carries more risk than secured loans like mortgages or auto financing. Issuers price in default risk, fraud losses, and operational costs, which explains the persistent margin above prime. The recent proposal for a 10% federal rate cap, floated by the Trump administration in January 2026, has sparked debate but faces uncertain prospects.

For borrowers carrying balances, the math is unforgiving. Paying only minimums on significant debt can stretch repayment timelines to decades while multiplying the total cost several times over. The most effective strategy remains paying more than the minimum whenever possible, prioritizing high-rate cards first, and avoiding new charges until balances decline.

This content is for educational purposes and does not constitute personalized financial advice.