Live: Will Apple Soar After Q1 Earnings Tonight?

Quick Read

-

Apple (AAPL) reports Q1 fiscal 2026 earnings today after beating estimates four straight quarters. Wall Street expects the company to report $2.67 in EPS. We expect Apple’s earnings to hit newswires at 4:30 tonight and will begin providing updates and analysis the moment they report. Simply stay on this page and new updates will load automatically below.

-

Higher iPhone component costs threaten Apple’s gross margins. Jefferies warned of significant App Store revenue growth slowdown.

-

Aletheia Capital cut its price target to $205 on margin concerns. Apple trades at a premium 34x trailing earnings.

Live Updates

Apple Trading Up .7% as of 5:45 p.m. ET

Apple’s conference call is winding down. Analysts have attempted to get more details on their arrangement with Google (without luck) and have pressed on margins.

At the end of the day, Apple is reporting surprisingly strong margins in Q2, yet shares are below where they traded shortly after Apple announced earnings.

To be frank, we’re fairly surprised. These were very good earnings that we’d expect to drive gains more around 2 to 3%. Instead, Apple is trading for slightly more than where it closed today.

If you enjoyed today’s coverage, make sure to check back to 24/7 Wall St. We publish earnings live blogs every day with real analysts digging into company reports.

Tim Cook Addresses Memory Prices Says Expect More Impact in Q2

Apple delivered revenue guidance that topped expectations and said margins would exceed Wall Street targets, but shares aren’t budging. They’re currently up .5%.

Not surprisingly, the first question on the Q&A portion of the call is about memory. Here it is in full:

Amit Daryanani Evercore ISI Institutional Equities, Research Division

Yes, I have 2. Maybe to start with — there’s a lot of focus on the impact of memory to hosted companies and I’d love to kind of get your perspective when you folks are guiding gross margins up into the March quarter. Just talk about, a, your comfort in securing the bits that you need for shipment? And b, how do we think about memory inflation flowing through Apple’s model over time?

Timothy Cook Chief Executive Officer

Yes, Amit, it’s Tim. Let me back up a bit and talk about the constraints that Kevin referred to in his remarks and memory try to get both of these out at once. First of all, we were thrilled with the customer response on the latest iPhone lineup. It exceeded our expectations to say the least.

And iPhone grew 23%. And what the result of that was that we exited the December quarter with very lean channel inventory due to that staggering level of demand. And based on that, we’re in a supply chase mode to meet the very high levels of customer demand. We are currently constrained. And at this point, it’s difficult to predict when supply and demand will balance. The constraints that we have are driven by the availability of the advanced nodes that our SoCs are produced on.

At this time, we’re seeing less flexibility in supply chain than normal, partly because of our increased demand that I just spoke about. From a memory point of view, to answer your question, memory had a minimal impact on the Q1, so the December quarter gross margin. We do expect it to be a bit more of an impact to the Q2 gross margin and that was comprehended in the outlook of 48% to 49% that Kevin gave earlier.

Beyond Q2, we don’t obviously provide outlooks beyond the current quarter. But we do continue to see market pricing for memory increasing significantly. As always, we’ll look at a range of options to deal with that. So hopefully, that gives you the full view.”

More on Apple's Guidance

Apple just issued guidance of between 13% and 16% growth next quarter.

Wall Street expected 12.5% growth, so that’s a beat.

Wall Street was expecting gross margins of 47.6%, so their guidance of 48.5% at the midpoint is a beat.

This is good news that should benefit shares.

Apple Delivers Revenue Guidance for Q2 On Tonight's Earnings Call

Here’s what Apples CFO just said on tonight’s conference call:

“Importantly, the color we’re providing assumes that global tariff rates, policies and their application remain in effect as of this call, and the global macroeconomic outlook does not worsen from today. We expect our March quarter total company revenue to grow by 13% to 16% year-over-year, which includes our best estimates of constrained iPhone supply during the quarter. We expect services revenue to grow at a year-over-year rate similar to what we reported in the December quarter. We expect gross margin to be between 48% and 49%. We expect operating expenses to be between $18.4 billion and $18.7 billion, which is at a similar level to what we reported in the December quarter and driven by higher R&D on a year-over-year basis. We expect OI&E to be around $100 million, excluding any potential impact from the mark-to-market of minority investments and our tax rate to be around 17.5%.”

Still Waiting for Margin Discussion

We’re on Apple’s call and waiting for the promised margin discussion and guidance but it hasn’t arrived yet.

Shares are currently up just .4% as investors wait on this commentary.

Apple's CFO is Talking Now

I’d expect gross margin discussion to happen shortly…

Apple CEO Tim Cook Addresses Incredible iPhone Demand on Tonight's Conference Call

Here’s what Tim Cook had to say about iPhone demand on tonight’s conference call:

“As I mentioned earlier, it was a fantastic quarter for iPhone with an all-time revenue record of $85.3 billion, up 23% year-over-year. This is the strongest iPhone lineup we’ve ever had and by far, the most popular. Throughout the quarter, customer enthusiasm for iPhone was simply extraordinary. Users were incredibly excited about everything enables them to do. iPhone 17 Pro and 17 Pro Max delivered the ultimate iPhone experience. They feature the best ever performance in battery life on an iPhone, the most advanced camera system and a striking design. iPhone Air, our slimmest and lightest smartphone yet, as powerful capabilities into an ultra slim and sleek design.

And iPhone 17 is a truly fantastic upgrade and an incredible value.”

Apple's Conference Call is Starting Now

We’ll continue updating this live blog throughout it.

As a reminder, what Apple says about gross margins about memory pricing on this call will determine if shares rise or fall tomorrow. Simply leave this page open and new updates should post automatically.

Gains Are Fading

Apple delivered blowout earnings, so why aren’t shares up 5%?

Likely the biggest reason (that we immediately identified in this live blog) is that the company is withholding margin guidance for its conference call.

That call starts in about 7 minutes.

Which is to say, leave this blog open if you want commentary and analysis on Apple’s conference call. It will likely shape where shares trade tomorrow. We will post updates with Apple’s specific commentary on memory prices from the call.

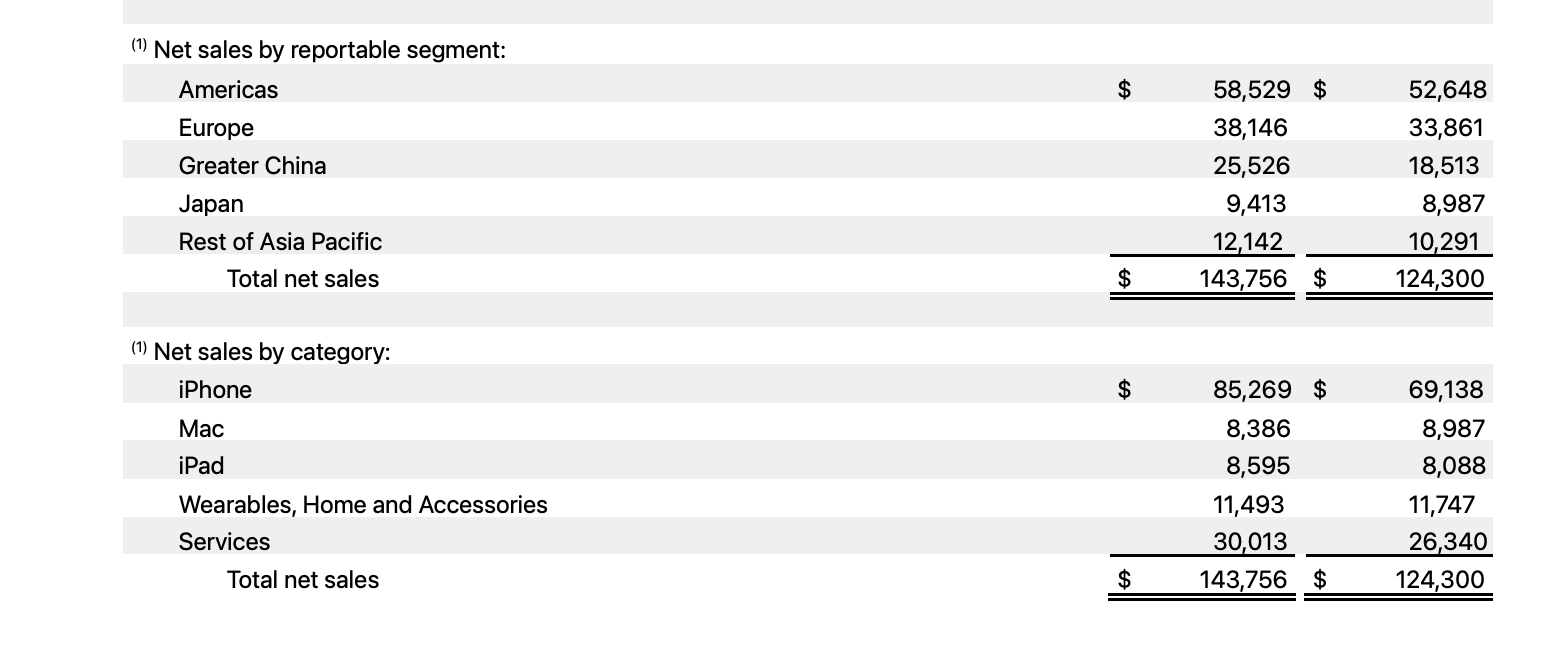

Apple's China Sales Up 38%

One massive reason for Apple’s beat is China performance. The company’s ‘Greater China’ region grew 38%. That was a $7 billion improvement from last year.

The biggest reason for Apple’s beat was iPhone sales. But sales to China are the second biggest ‘bright spot’ from today’s earnings. We’re waiting on Apple’s conference call for clarity on future gross margins to see where shares will head next.

As of 4:47 p.m. ET, shares are up moderately, about .8%.

Apple Q1 Earnings Scorecard: Revenue Gets an 'A'

Overall Grade: A

Apple delivered one of its strongest quarters in years, crushing estimates across every major metric while demonstrating exceptional operational execution. The 15.7% revenue growth marks a significant acceleration from the 4% pace in Q1 2025, driven by record iPhone demand and robust Services momentum. Cash generation improved dramatically, enabling $32B in shareholder returns.

| Category | Grade | Notes |

|---|---|---|

| Revenue Performance | A | $143.8B beat estimates by $5.4B; 15.7% YoY growth accelerated from 4% in Q1 2025 |

| Earnings Beat/Miss | A | $2.84 EPS crushed $2.67 estimate by 6.4%; up 18% YoY |

| Guidance Quality | B+ | Deferred margin guidance to call; awaiting clarity on memory cost pressures |

| Margin Trends | A- | Gross margin 48.1%; operating margin expansion despite elevated component costs |

| Cash Flow | A+ | $53.9B operating cash flow surged 80% YoY; exceptional conversion |

| Management Confidence | A | Tim Cook called results “remarkable” and “well above expectations” |

Apple Growth Rate by Geography and Categories

Gains Holding

As we just noted, Apple is waiting for their conference call to address forward guidance on margins. That could shift narrative.

This is likely causing share gains to fade, as Apple’s after-hours gains have fallen from an immediate jump off nearly 3% down to 1.2% gains.

We expect shares will continue bouncing around as investors digest these earnings.

More Figures On Apple's Quarter

Wow, we’re blown away by the 23% growth in iPhone revenues. Clearly, Wall Street is happy too.

Other figures to note:

Revenue: $143.76 billion vs. expectations of $138.40 billion.

Apple CEO Tim Cook just told CNBC they’ll address surging memory prices on their conference call.

One note – the company is waiting to give guidance on their margins for their call. So there could be a large shift in sentiment when those numbers are announced.

Apple Earnings Are Out

The headline is a blowout quarter.

- EPS of $2.84 (versus expectations of $2.67)

iPhone revenues were up 23% (!!!).

Services revenue largely inline with Wall Street expectations.

Shares are jumping right now, up 2.6%

Stay here for more updates and analysis.

Apple's Setup Headed Into Earnings

Apple enters tonight’s earnings call trading at $258.42, down 4.9% year-to-date but up 4% over the past week. The stock sits roughly 10% below its 52-week high of $288.62, positioning it within striking distance of analyst consensus targets near $287.

Recent volatility shows investor caution: shares fell to $248 last week before recovering. Institutional activity signals confidence—Strategic Planning Group increased its stake 24% in Q3 2025, making Apple its largest holding.

Semiconductor suppliers are surging: Micron jumped 52% year-to-date and TSMC gained 11.5%. The question is whether their gains are a sign of demand that’s bullish for Apple or gives them pricing pressure that can prove very bearish.

Five Minutes to Earnings

We are five minutes away from Apple’s earnings. Leave this page open and new updates will post automatically. The moment Apple’s earnings hit newswires we will begin posting news and analysis.

SanDisk Just Reported Earnings and is Up 15%

One of the greatest pressures on Apple headed into earnings is the pricing on its supplies, especially in memory. SanDisk just reported and their earnigns were stunning. The company delivered $6.20 in EPS versus estimates of $3.44. Shares are up 15%.

That’s an ominous sign for Apple headed into tonight’s earnings.

Top 5 Questions Analysts Will Ask

As we wait for Apple to report earnings tonight, here are some areas we’d expect Wall Street to ask about on Apple’s conference call.

- iPhone Demand & China Recovery: How are current iPhone sales trending? What improvements are you seeing in Greater China after recent weakness?

- AI Strategy & Development: What’s the timeline for your AI product roadmap and Siri enhancements? How will this differentiate Apple’s AI from competitors?

- Memory Cost Pressures: How are elevated storage component costs impacting gross margins? Are you seeing relief in the supply chain for Q2?

- Services Growth Momentum: Can you provide details on Services segment performance and your outlook for continued growth?

Key Phrases to Listen For

Bullish signals: “China stabilization,” “AI monetization roadmap,” “margin expansion.” Red flags: “supply chain headwinds,” “promotional activity,” vague AI timelines.

Key Areas to Watch Tonight When Apple Reports

Key metrics analysts are watching tonight: iPhone 17 demand trajectory, Services growth acceleration (targeting 15%+ annually), and China stabilization after recent weakness. Any mention of AI monetization timelines or the newly acquired Q.ai integration roadmap would likely draw analyst attention.

Prediction Markets Are Very Confident in Apple Beating Earnings

Prediction markets place 94% odds that Apple will beat EPS estimates of $2.67 tonight.

That’s on the higher end of probabilities this earnings season. Last night, prediction markets only gave Tesla a 40% chance of beating earnings.

However, Apple is slightly overshadowed by Visa, which is also reporting tonight. Prediction markets award them a 97% chance of beating earnings.

Apple (NASDAQ: AAPL | AAPL Price Prediction) reports first-quarter fiscal 2026 results today after the bell. After a strong run of consecutive beats and a stock that’s pulled back 6% over the past month, this report will test whether the iPhone maker can deliver on elevated expectations.

Momentum Meets Caution

Last quarter, Apple posted revenue of $102.47 billion, up 7.9% year-over-year, with earnings per share of $1.85 that beat estimates by 5.1%. The company has now beaten consensus estimates in each of the past four quarters, with surprise margins ranging from 1.85% to 9.79%. That consistency matters because investors have learned to expect outperformance.

Since that October report, the stock climbed to $288 before retreating to current levels near $256. The pullback reflects a broader rotation out of mega-cap tech, but it also creates room for the stock to move on a solid print. Prediction markets are pricing in a 94.5% probability of a beat, which tells you sentiment is confident but not euphoric.

Consensus Estimates

| Metric | Q1 FY2026 Estimate | YoY Growth | Full Year FY2026 |

|---|---|---|---|

| EPS | $2.67 | +11.3% | $8.27 |

| Revenue | $138.5B (implied) | ~9% | $430.4B |

All Eyes on iPhone and Margins

Three key areas will be closely watched. First, iPhone revenue and unit trends. Analysts are calling this an “iPhone 17 supercycle” driven by AI features, but supplier weakness from Qorvo and Skyworks suggests demand may be normalizing after the holiday quarter. If iPhone sales disappoint, Apple shares will face pressure.

Second, gross margins. Memory shortages are driving up component costs, and the iPhone 17’s bill of materials is reportedly higher than prior models. Aletheia Capital flagged this risk explicitly, cutting their price target to $205 on margin compression concerns. The key question is whether Apple’s pricing power can offset these headwinds or if margins compress as feared.

Third, Services growth. This segment has been Apple’s margin expansion engine, but Jefferies warned of a “significant slowdown in App Store revenue growth.” If Services decelerate while product margins compress, the bull case weakens fast. Services revenue holding above 10% growth would be needed to keep the narrative intact.

China revenue will also matter. Wedbush’s Dan Ives has been bullish on a China rebound, but Norway’s sovereign wealth fund reduced tech stakes last quarter, signaling some institutional caution. Any commentary on China demand trends will move the stock.

An Important Earnings Tonight

Apple trades at 34x trailing earnings, a premium valuation that assumes continued margin expansion and AI monetization. The company has earned that multiple through consistent execution, but today’s report needs to prove the story still works. If management delivers on iPhone strength, margin stability, and Services growth while providing confident guidance, the stock could reclaim $270 quickly. If any of those three pillars crack, expect the market to reassess whether Apple deserves to trade at this valuation.

Eric Bleeker has been investing for more than 20 years. He began his career working at Microsoft before joining Motley Fool, one of the largest publishers of financial research. In his 15 years at Motley Fool Eric served as the General Manager for Fool.com and led coverage in the Technology & Telecom sector. In addition, he was a featured columnist and has hosted dozens of investing seminars attended by more than a million total investors. Eric has more than 1,000 financial bylines to his name and has been featured in The Wall Street Journal, CNBC, Fox Business, and many other leading publications. He is currently focused on artificial intelligence investing and is a CFA Charterholoder.

© 24/7 Wall St