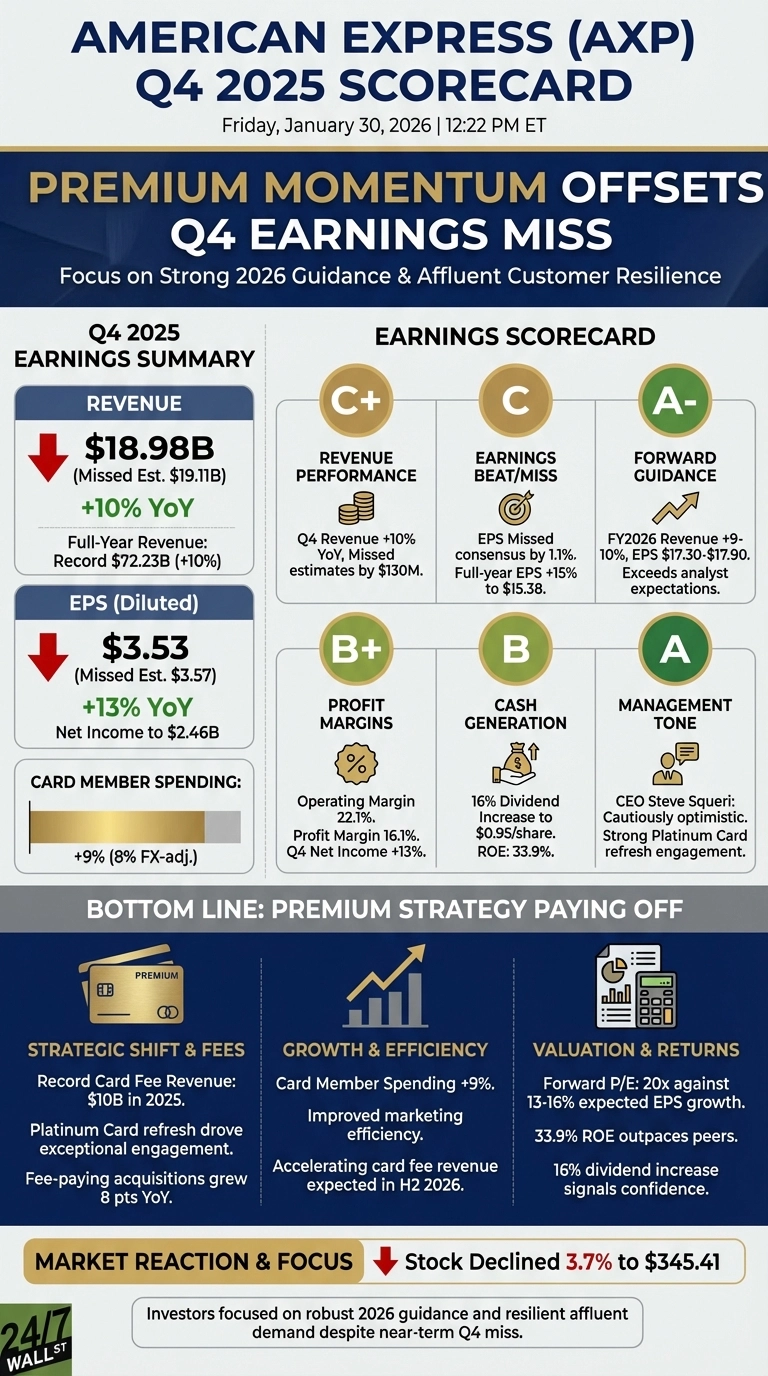

American Express (NYSE: AXP | AXP Price Prediction) reported Q4 2025 results that fell short of Wall Street expectations, with EPS of $3.53 missing the $3.57 consensus by 1.1% and revenue of $18.98 billion missing estimates of $19.11 billion. Despite the misses, shares declined only 3.7% to $345.41 in Friday trading as investors focused on robust 2026 guidance and the company’s premium customer momentum.

Earnings Scorecard

Bottom Line: Premium Strategy Paying Off Despite Near-Term Miss

The Q4 miss masks underlying strength in American Express’s premium customer strategy. The September 2025 Platinum Card refresh drove exceptional engagement, with management noting “some of the lower cost of acquisition for Platinum in the last 2 years” despite raising the annual fee to $325. Card fee revenue reached a record $10 billion in 2025 and is expected to accelerate in H2 2026 as renewals hit at higher price points.

The company’s strategic shift toward fee-paying premium products improved marketing efficiency, with fee-paying acquisitions growing 8 percentage points year-over-year. Card member spending grew 9% (8% FX-adjusted) in Q4, demonstrating resilient affluent consumer demand even as the broader economy faces uncertainty.

With a forward P/E of 20x against expected 13-16% EPS growth, American Express trades at a valuation that reflects its expected earnings growth trajectory. The 16% dividend increase signals management confidence in cash generation, while the stock’s 34% ROE outpaces financial services peers.

Investors should monitor whether the Platinum Card momentum sustains through 2026 renewal cycles and whether marketing efficiency gains continue. The company’s ability to grow card fees while maintaining retention rates will be critical to achieving the upper end of guidance. The Q4 miss appears tactical rather than structural, with the premium positioning intact.