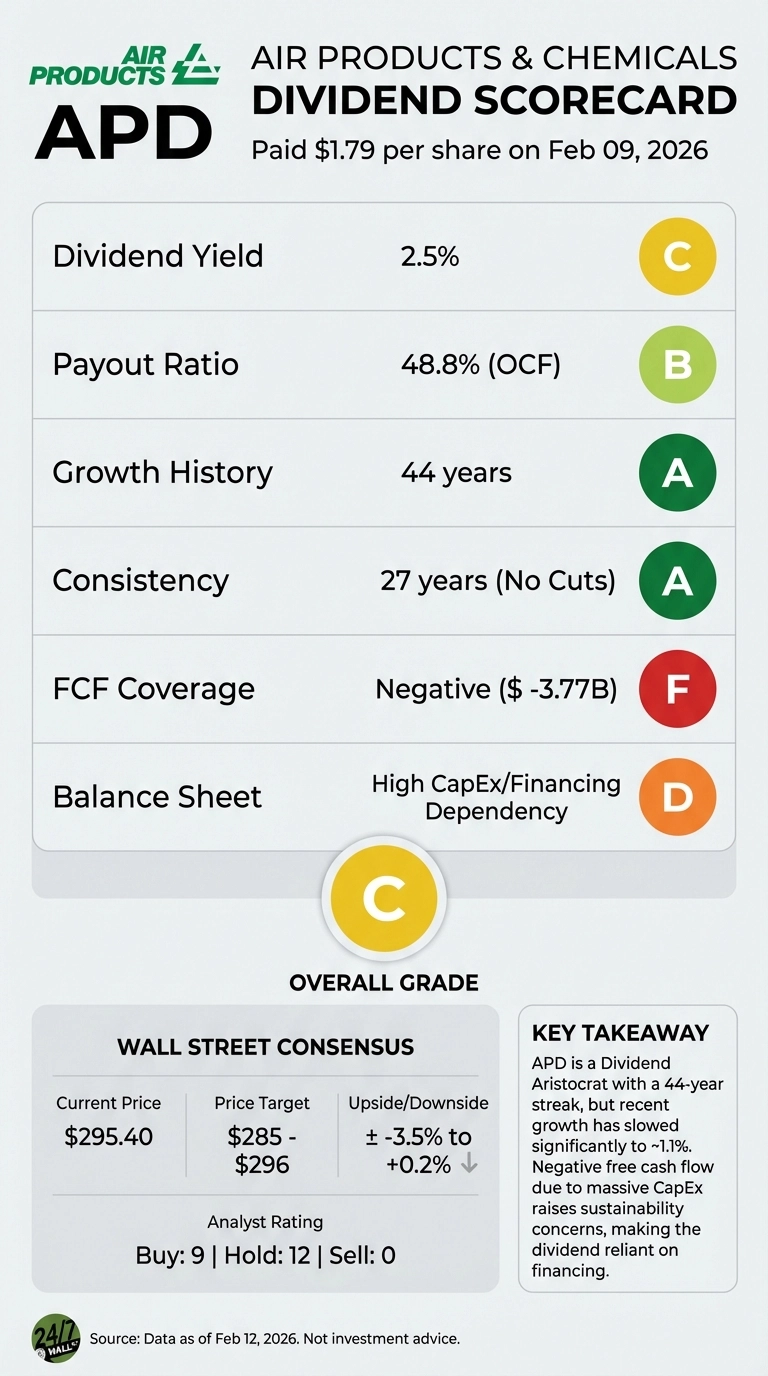

Air Products & Chemicals (APD) just delivered its $1.79 per share quarterly dividend on February 9, 2026, marking another milestone in a streak that few industrial companies can match. With 44 consecutive years of dividend increases, APD has earned its Dividend Aristocrat status, but the latest payment arrives against a backdrop of mounting operational pressures that deserve closer scrutiny.

The Dividend That Just Hit Your Account

The $1.79 quarterly payment represents the final installment before the company’s recently announced increase. On January 27, 2026, management declared the next quarterly dividend at $1.81 per share, a 1.1% increase that continues the growth trajectory but at a noticeably slower pace than the company’s historical standard.

At the current stock price of $295.40, that translates to a forward yield of approximately 2.5%. That’s respectable for an industrial giant, though hardly compelling in isolation. The real question investors should ask: Can APD sustain this payout, let alone grow it, given what’s happening beneath the surface?

The Cash Flow Reality Check

Here’s where the dividend scorecard gets uncomfortable. In fiscal year 2025, APD generated $3.25 billion in operating cash flow—adequate to cover the $1.58 billion dividend payout at a ratio of 2.05x. That sounds safe until you account for capital expenditures.

The company spent $7.02 billion on capital projects last year, creating a negative free cash flow of $3.77 billion. This isn’t a one-year anomaly. Fiscal 2024 showed similar strain with negative free cash flow of $3.15 billion. APD is essentially funding dividends through financing activities rather than operational strength, a pattern that raises sustainability concerns despite the impressive 44-year streak.

The capital intensity surge tells the story: annual CapEx jumped from $2.93 billion in fiscal 2022 to $7.02 billion in fiscal 2025, reflecting major investments in hydrogen infrastructure and clean energy projects. Management has signaled discipline ahead, targeting approximately $4.0 billion in CapEx for fiscal 2026—a $1 billion reduction from prior plans—but the company remains in heavy build mode.

Operational Strength Meets Strategic Headwinds

The first quarter of fiscal 2026 offered encouraging signs. APD reported adjusted EPS of $3.16, up 10% year-over-year and beating analyst expectations of $3.04. Revenue reached $3.10 billion with operating income climbing 14% to $735 million. Regional performance showed resilience: Americas up 4% to $1.3 billion, Asia up 2% to $832 million, and Europe surging 12% to $782 million.

CEO Eduardo Menezes pointed to “strong base business performance” as the driver, though he acknowledged helium headwinds that continue to pressure margins in Asia. The helium segment faces a 3% expected decline for the full fiscal year, driven by increased Russian supply and the reshaping of the U.S. federal helium system.

The company’s $140 million NASA liquid hydrogen contract provides a bright spot, extending a 69-year partnership and validating APD’s positioning in the clean hydrogen economy. With the liquid hydrogen market projected to grow from $42.3 billion in 2024 to $65.9 billion by 2032, APD’s infrastructure investments target genuine long-term demand—but that doesn’t solve the near-term cash flow squeeze.

Insider Confidence vs. Market Skepticism

Insider activity tells a constructive story. On January 28, 2026, the board executed coordinated phantom stock acquisitions at $259.12 per share, with director Wayne Thomas Smith acquiring 1,698 shares valued at $439,866. Earlier in December, CEO Eduardo Menezes acquired 17,376 shares and CFO Melissa Schaeffer added 8,357 shares across two transactions. These acquisitions, primarily through equity compensation, signal management alignment with shareholders.

Yet external analysis offers a more cautious view. Simply Wall Street flagged concerns in a February 11, 2026 report, noting the company is “not generating profit or free cash flow” with “shrinking earnings per share” that could make “future dividend payments unsustainable.” The analysis carries a -0.333 sentiment score, reflecting skepticism despite the dividend increase announcement.

The Dividend Growth Deceleration

Historical context reveals a concerning trend. APD’s dividend grew at an average 8.5% annually over the past two decades, with particularly strong years like 2004 (+19.6%), 2008 (+15.8%), and 2011 (+18.4%). Recent growth has slowed dramatically: 2024 saw just 1.1% growth, 2025 managed 2.3%, and the latest increase registers 1.1%.

The payout ratio from operating cash flow sits at 48.8%—manageable in isolation—but the negative free cash flow forces a different calculation. APD paid out $1.58 billion in dividends against negative free cash flow of $3.77 billion, relying on $2.21 billion in financing cash flow to bridge the gap. This isn’t dividend coverage—it’s financial engineering.

Analyst Expectations and Market Positioning

Wall Street has responded to the Q1 beat with measured optimism. Bernstein raised its price target from $300 to $315 on February 2, 2026, while Deutsche Bank lifted its target from $255 to $300 on February 9. The consensus target across 22 analysts sits around $285-$296, implying modest upside from current levels.

The stock has shown recent strength, gaining 20.44% year-to-date and 10.98% over the past month. However, the one-year return of -2.3% reflects the operational challenges that have weighed on valuation. The forward P/E ratio of 22x prices in expectations for improved execution as capital spending normalizes.

What Dividend Investors Should Monitor

The next 12-18 months will determine whether APD’s dividend streak continues on solid footing or becomes increasingly dependent on financial maneuvering. Key metrics to watch include quarterly free cash flow generation, progress on the Louisiana blue hydrogen/ammonia complex, and whether helium headwinds stabilize as management expects.

Management’s full-year guidance of adjusted EPS between $12.85 and $13.15 suggests confidence in operational improvement. If achieved, that would represent solid growth from the prior year and provide breathing room for continued dividend increases, albeit modest ones.

For income-focused investors, APD offers a legitimate 44-year dividend growth record backed by a global industrial gas franchise serving essential markets. The 2.5% yield won’t excite anyone seeking high current income, but the Dividend Aristocrat pedigree carries weight. The concern isn’t whether APD will pay next quarter’s dividend—it will. The question is whether the company can return to generating genuine free cash flow that supports both the dividend and the growth investments management deems necessary for long-term competitiveness.

The $1.81 per share payment scheduled for May 11, 2026 will arrive as promised. What happens in the quarters beyond that depends on whether APD’s capital-intensive bet on the hydrogen economy starts generating returns that justify the current cash consumption rate.