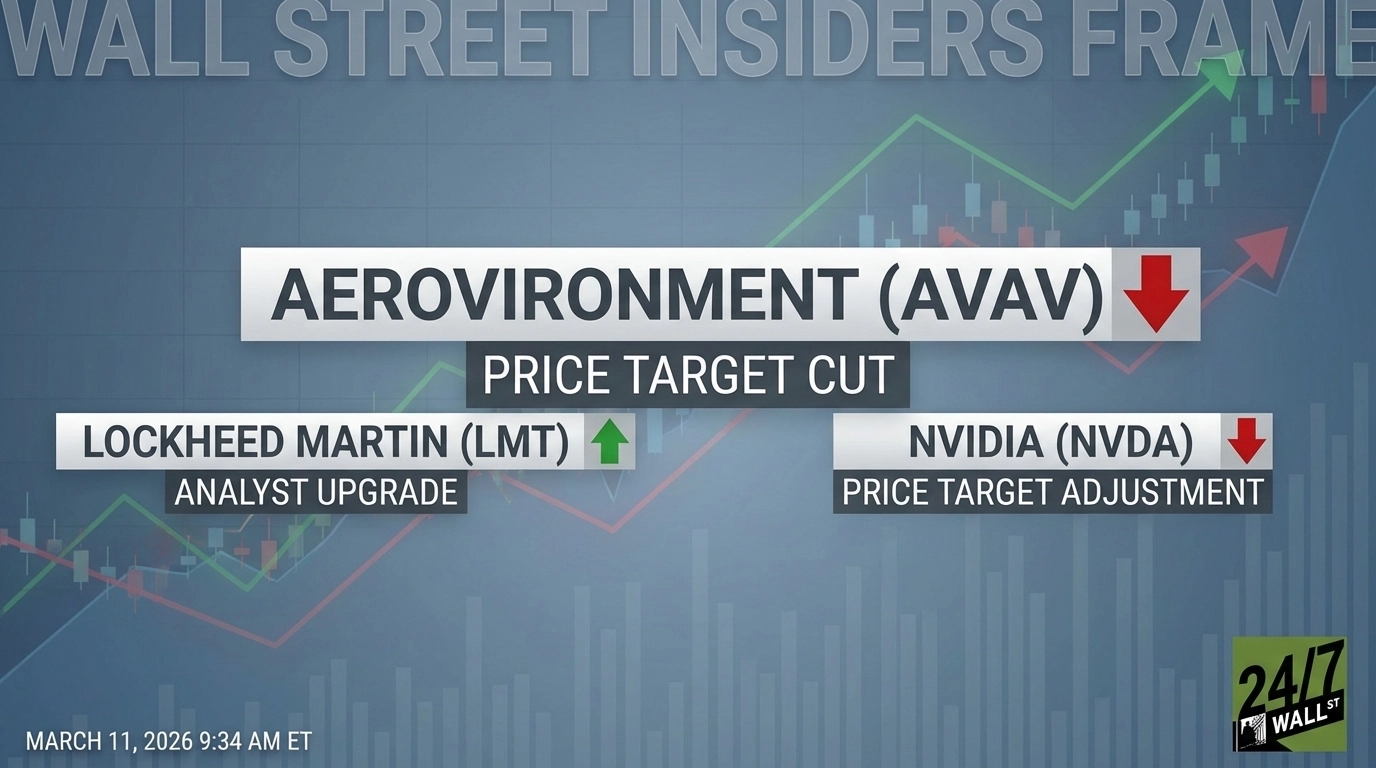

KeyBanc Capital Markets trimmed its price target on AeroVironment (NASDAQ:AVAV | AVAV Price Prediction) to $295 from $330 following the company’s fiscal third-quarter 2026 earnings report, while maintaining an Overweight rating on the shares. The cut reflects fallout from a stop-work order on the BADGER SCAR program and contract timing disruptions in the Space, Cyber and Directed Energy segment – though KeyBanc sees the core drone and defense thesis intact, particularly if tensions with Iran escalate further.

| Ticker | Company Name | Firm | Old → New Rating | New Price Target | Implied Upside | One-Line Takeaway |

|---|---|---|---|---|---|---|

| AVAV | AeroVironment Inc. | KeyBanc | Overweight (maintained) | $295 (from $330) | ~33% | Rating held; target trimmed on SCAR disruption and timing headwinds |

The Analyst’s Case

KeyBanc lowered its price target to $295 from $330 and kept its Overweight rating after adjusting estimates post-earnings. The firm attributes the target reduction to recent changes to the SCAR program and timing in contract awards. Despite the revision, KeyBanc’s broader conviction on AeroVironment is unchanged: the firm maintains that AeroVironment is positioned to capitalize on the proliferation of UAS/cUAS and increased government spending in defense and space-related programs.

The geopolitical angle is central to KeyBanc’s bull case. Should the conflict in Iran intensify, AeroVironment is positioned as one of the top beneficiaries, in KeyBanc’s view. That view is grounded in the company’s Switchblade loitering munitions franchise and its growing uncrewed aircraft systems portfolio, both of which have seen surging demand.

Company Snapshot & Recent Performance

AeroVironment is a defense technology company specializing in autonomous systems and loitering munitions, with products including the Switchblade, Puma, BADGER, Titan, and Defender ROV. In May 2025, the company acquired BlueHalo for approximately $1.35 billion, adding Space, Cyber and Directed Energy capabilities and significantly expanding its revenue base.

Fiscal Q3 2026 results, reported after the close on March 10, 2026, disappointed on both top and bottom lines. Revenue came in at $408.05 million, missing the $475.65 million consensus estimate by 14.21%, though it still represented 143.4% growth year-over-year. Non-GAAP EPS of $0.64 missed the $0.69 estimate by 7.39%, marking the third consecutive quarterly miss.The headline numbers were distorted by a single event: a stop-work order on the BADGER SCAR program triggered a $151.31 million goodwill impairment, and $1,493.2 million of SCAR-related unfunded backlog options are no longer expected to be awarded. That drove operating income to -$179.04 million and net income to -$156.55 million for the quarter.The stock has reflected the pressure. AVAV is down 8.4% year-to-date and off 13.85% over the past month as of March 10, 2026. The immediate post-earnings reaction was sharp: shares dropped roughly 9.9% intraday in the hour following the filing. Over the past year, however, the stock is still up 79.63%, underscoring how much the longer-term defense demand narrative has driven the valuation.

Why the Move Matters Now

The SCAR program disruption is the crux of the price target cut. The BlueHalo acquisition brought with it a significant Space Force contract that is now being rebid, and the stop-work order has effectively removed nearly $1.5 billion in expected future revenue from the backlog. That forced management to lower full-year fiscal 2026 guidance: revenue guidance was trimmed to $1.85 billion to $1.95 billion from $1.90 billion to $2.00 billion, with non-GAAP EPS now guided to $2.75 to $3.10.

The analyst consensus, while still broadly constructive, has grown more cautious. The consensus price target sits at $355.17, with 17 buy ratings and 2 hold ratings and no sells. KeyBanc’s revised $295 target is notably below that consensus, suggesting the firm is pricing in more execution risk than the Street average. At the current price of $221.57, KeyBanc’s target still implies meaningful upside, but the path depends heavily on SCDE segment stabilization and contract re-award outcomes.There are genuine offsets to the SCAR headwind. Funded backlog reached a record $1.10 billion with a book-to-bill ratio of 1.6x, and year-to-date bookings reached $2.1 billion with total FY2026 awards of $4.5 billion. The Autonomous Systems segment continues to perform: Uncrewed Aircraft Systems revenue grew 50.3% year-over-year and Precision Strike & Defensive Systems rose 21.4%. CEO Wahid Nawabi framed the setup as constructive: “Strong order flow and growth in funded backlog during the quarter are setting the stage for record fourth quarter revenue and a solid start to fiscal year 2027.”Management also flagged an upcoming investor engagement: CEO Nawabi and CFO Kevin McDonnell are scheduled to participate in a fireside chat at the J.P. Morgan 2026 Industrials Conference on March 18 at 1:35 p.m. ET, which could provide additional clarity on the SCAR re-competition timeline and SCDE recovery trajectory.

Key Factors to Watch

The KeyBanc note signals a recalibration rather than a reversal in analyst sentiment. The core autonomous systems business is growing, the funded backlog is at record levels, and the geopolitical backdrop for drone and loitering munitions demand remains supportive. The SCAR program disruption is a real setback, but it is concentrated in the BlueHalo-derived SCDE segment and does not appear to have affected the underlying UAS franchise.

The key variables to watch are the outcome of the SCAR re-competition, whether management can deliver on its Q4 revenue recovery guidance, and how the SCDE segment stabilizes as BlueHalo integration continues. The stock trades at a forward P/E of approximately 60x, which leaves little room for further estimate reductions. Analysts will be watching order momentum against execution and contract uncertainty as key variables going forward, particularly given three consecutive quarterly misses.