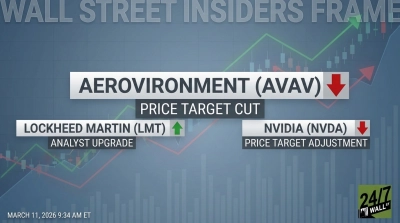

AeroVironment (NASDAQ:AVAV | AVAV Price Prediction) appeared set for liftoff when the U.S.-Israeli conflict with Iran erupted, thrusting its battle-tested Switchblade loitering munitions and reconnaissance drones into the spotlight. Demand for these precision systems was expected to surge as the Pentagon leaned harder into unmanned operations to limit troop exposure.

Yet that momentum evaporated overnight when the U.S. Space Force announced it would recompete the Satellite Communication Augmentation Resource (SCAR) program — AeroVironment’s single largest contract. The rebid immediately cast a shadow over a sizable slice of the company’s backlog.

Compounding the blow, AeroVironment’s just-reported fiscal third-quarter results fell short of Wall Street expectations while management prudently trimmed full-year guidance to reflect ongoing uncertainty. That caused shares to tumble again, leaving the stock down roughly 50% from its recent high.

Is the selloff appropriate for the circumstances or is this dip a genuine buying opportunity?

Unmanned Arsenal Remains Battle-Ready

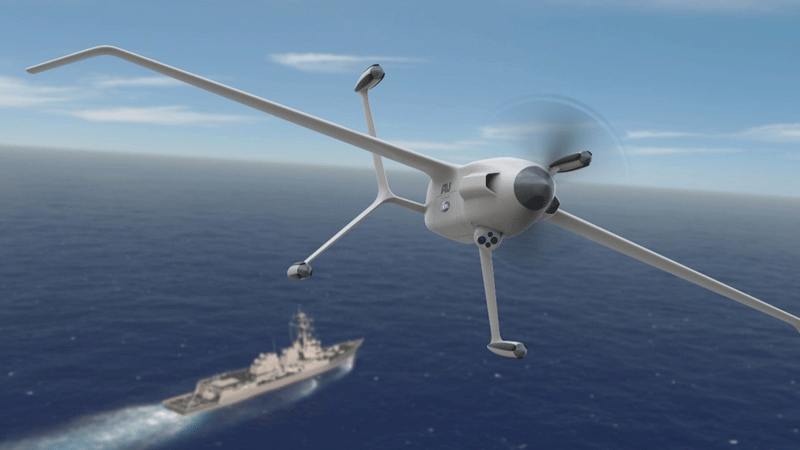

AeroVironment has carved out a commanding niche in the Pentagon’s accelerating pivot to drone-centric warfare. Its Switchblade family delivers portable, precision strikes against high-value targets, while Puma and Raven systems provide persistent intelligence, surveillance, and reconnaissance in contested airspace. These platforms have already demonstrated their value in Ukraine and are now drawing fresh interest amid the current Middle East operations.

The 2025 BlueHalo acquisition layered in space and counter-drone technologies, including the BADGER phased-array antennas originally tied to SCAR. That expansion positioned AVAV across air, space, and cyber domains — precisely where the Defense Department wants integrated solutions. Recent multi-million-dollar Army orders for upgraded Switchblades underscore that core demand is intact, independent of any single contract.

The SCAR Rebid Is a Setback, Not Surrender

The Space Force’s move to reopen SCAR stems from legitimate goals: fixing supply-chain weaknesses, shifting from cost-plus to fixed-price structures, and inviting multiple suppliers for greater resilience and surge capacity. A temporary stop-work order followed, and the program’s future structure is still evolving.

Importantly, the rebid does not equate to a total loss for AeroVironment. The company remains eligible to compete under the revised requirements and has already signaled its intent to offer a commercialized, lower-cost solution. Management is simultaneously expanding manufacturing capacity in New Mexico to support both existing and potential new awards.

While Wall Street initially punished the stock — triggering a high-profile downgrade — several analysts countered that SCAR represents a modest slice of projected revenue and that AeroVironment’s technology remains highly competitive. Management’s guidance reduction, while disappointing, reflects prudent conservatism rather than a collapse in fundamentals; it could easily be revisited upward once visibility improves or rolled into next fiscal year’s growth trajectory.

Even without SCAR’s full original scope, AVAV’s diversified drone portfolio continues to generate strong bookings and a record backlog. The ongoing Iran conflict, which shows signs of lasting longer than initial projections, could accelerate procurement decisions across U.S. and allied forces. Loitering munitions and small unmanned aircraft systems (UAS) are exactly the tools needed for sustained, low-risk operations — areas where AeroVironment already leads.

Key Takeaway

AeroVironment’s drone business stays fundamentally robust, backed by proven products and rising global demand. Prolonged tensions in the Middle East may yet spark a fresh wave of orders that more than offsets any SCAR-related haircut.

While this is not the moment for aggressive, all-in buying — the near-term uncertainty is real — the steep 50% discount creates a compelling entry point for investors willing to establish or add a position. AeroVironment’s track record of innovation and execution suggests it will remain a cornerstone player in defense technology for years to come. At today’s levels, patient investors could be well rewarded once the market refocuses on the company’s broader growth runway.