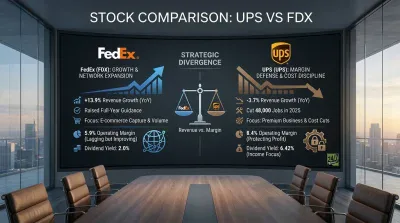

Still one of the most notable vehicles on the road, United Parcel Service (NYSE:UPS | UPS Price Prediction) has shed 18.48% over the past month, with shares near $97 after briefly touching $116.63 in the 30 days following January earnings. The catalyst: UPS is deliberately shrinking its revenue base to rebuild around higher-margin customers.

Shrinking on Purpose, and Investors Are Skeptical

UPS CEO Carol Tome confirmed the company is in the final six months of its Amazon-accelerated glide-down, targeting another 1 million pieces per day reduction across 2026. In addition, U.S. Domestic Package volume has declined every quarter in 2025: down 3.5% in Q1, 7.3% in Q2, 12.3% in Q3, and 10.8% in Q4. Management’s thesis is that replacing low-margin Amazon parcels with healthcare and SMB customers improves long-term profitability. Analysts expect the healthcare logistics segment to double its revenue run rate to approximately $20 billion by late 2026. Investor sentiment remains skeptical that the transition will happen cleanly.

- Full-year 2025 revenue fell 2.46%, while operating income dropped 9.42% year over year, indicating cost cuts have not yet fully offset lost volume.

- The $6.56 annualized dividend creates real cash flow pressure, with UPS guiding for approximately $6.5 billion in free cash flow against a planned $5.4 billion dividend payout in 2026, leaving little buffer for execution missteps.

- FedEx surpassed UPS in market capitalization for the first time in March 2026, a milestone reflecting a multiyear divergence in how investors view each carrier.

FedEx Is Winning the Optics War

FedEx is up ~22% year-to-date in 2026 as investors reward its restructuring progress, while UPS is down on the year. FedEx (NYSE:FDX) also surpassed UPS in market capitalization for the first time in March 2026, a significant milestone in the shipping world and one that reflects a multiyear divergence in how investors view the two carriers.

CFO Brian Dykes described 2026 as a “bathtub effect”: a painful first half followed by a second-half recovery. Tome put the inflection point at June 2026. The key number when Q1 2026 results arrive is domestic operating margin. If it holds flat against the volume decline, the pivot thesis gains credibility. If it compresses further, the dividend question moves to the front of every conversation.

Data Sources

- UPS Q4 2025 earnings press release: SEC Exhibit 99.1, Accession 0001628280-26-003510

- UPS Q4 2025 earnings call transcript sourced via Alpha Vantage, including direct management commentary on Amazon glide-down and 2026 guidance

- Healthcare revenue trajectory and dividend sustainability context