UiPath (NYSE:PATH | PATH Price Prediction) declined approximately 6% in today’s session, trading below $12 midday on Thursday. The selloff is puzzling on the surface. UiPath just posted a quarter that beat expectations on every major metric and crossed a profitability threshold it had never crossed before.

The stock is now down 29% year-to-date. Underneath the price action, however, there’s a real argument building that UiPath is setting up for the kind of inflection that Palantir Technologies (NYSE:PLTR) experienced before the market finally rewarded its AI platform story.

The question isn’t whether UiPath is a good business. Rather, it’s whether the market is pricing in what happens when agentic AI automation goes from enterprise experiment to enterprise standard.

Strong Quarter, Weak Reaction

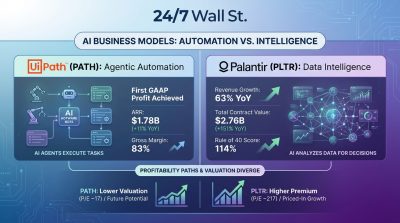

UiPath’s most recent quarter, Q4 of FY2026, was genuinely impressive. Revenue came in at $411 million, up 15.9% year-over-year, beating the consensus estimate of $392.87 million. Non-GAAP EPS of $0.16 beat the $0.146 estimate.

The profitability story is what stands out. UiPath posted GAAP operating income of $13 million, compared to a loss of $43 million in the same quarter last year. Non-GAAP operating income nearly doubled to $88 million, with non-GAAP operating margin expanding to 21% from 14% a year ago.

Annual recurring revenue reached $1.782 billion, up 11% year-over-year, with a dollar-based net retention rate of 107%. That retention figure means existing customers are spending more, not less. Moreover, Q4 guidance calls for revenue of $462 to $467 million and non-GAAP operating income of approximately $140 million.

CEO Daniel Dines framed the opportunity succinctly on the earnings call:

“Enterprises are accelerating their AI and automation strategies, and they’re looking for a unified platform rather than standalone tools. Our ability to bring deterministic automation, agentic automation, and orchestration together in one trusted, governed system is a true differentiator. It’s delivering meaningful outcomes for customers and positions us well as we close out the year.”

The Palantir Parallel

Here’s where the comparison gets interesting. Palantir Technologies spent years being dismissed as overvalued, opaque, and government-dependent before its AI platform narrative finally clicked with the market. PLTR stock is up 94.23% over the past year and 463.15% over five years; in contrast, UiPath stock’s one-year return is basically flat.

The gap is stark, but the underlying setup has real similarities. Both companies built enterprise AI platforms with government and commercial customers, and both have deep integration ecosystems.

Besides, the valuation case is hard to ignore as UiPath trades at a P/E of around 24x against a software industry average of roughly 94x. Additionally, the company carries $1.6 billion in cash and zero debt, and the analyst consensus price target for PATH stock implies 34.9% upside from current levels.

As for the bear case, it centers on the company’s growth rate. UiPath is growing at 16%, not 70%. Palantir’s Q4 2025 revenue grew 70% year-over-year, with U.S. commercial revenue up 137%. That’s a different league.

Yet, Palantir wasn’t always growing at 70% either, and the market didn’t reward it until it did. The key question analysts are watching is whether the agentic automation wave accelerates its growth trajectory the way AIP did for Palantir.

On top of all that, PLTR stock short interest is elevated at 57.18 million shares; this represents 15.59% of the float, up 10.18% from the prior report. That’s a meaningful short position, and it’s part of what’s driving today’s share-price pressure.

What to Watch

For UiPath’s loyal shareholders, the next earnings report is months away but could be make-or-break. Guidance calls for strong sequential improvement in both revenue and operating income, and any acceleration in ARR growth would go a long way toward closing the gap between what the business is doing and what the stock is pricing in.

For now, though, UiPath’s 6% drop today reflects the tension between near-term growth concerns and longer-term AI automation potential. The business is profitable, growing, and deeply integrated into enterprise AI infrastructure. Whether this translates into a Palantir-style market rerating remains an open question that will likely be answered by future ARR growth trends.