UiPath (NYSE:PATH | PATH Price Prediction) currently trades at $10.39, while the average analyst price target sits at $13.80, implying upside of roughly 33% from current levels.

UiPath sells enterprise automation software combining AI agents, robotic process automation, and human workflows into a single platform. The company has positioned itself at the center of the agentic AI wave, with integrations spanning Microsoft Azure AI Foundry, OpenAI, NVIDIA, Snowflake, and Google. A gap this wide typically signals a disconnect between current fundamentals and what analysts expect the business to become.

A 36% YTD Decline Driven by Guidance Concerns and Insider Selling

UiPath has shed 36.55% year-to-date. The most recent catalyst was a gut punch: the company delivered a Q4 beat on revenue and EPS but issued cautious fiscal 2027 guidance. Morgan Stanley, Mizuho, and Wells Fargo all lowered their price targets in response, sending shares down roughly 6%. When a company beats estimates and still gets punished, the market is signaling concern about forward expectations.

CEO Daniel Dines sold 122,734 shares in October 2025, followed by additional sales of 45,000 shares in October and another 45,000 shares in both December and January. Other executives sold alongside him. Markets interpreted the activity as a signal of a lack of confidence.

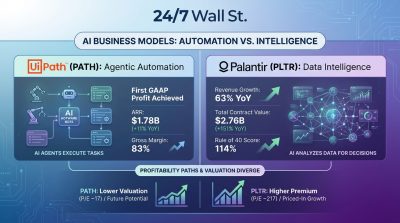

The bull thesis rests on UiPath’s improving profitability and positioning in agentic automation. The company delivered a strong Q4, with revenue of $481 million growing 14% year-over-year. Non-GAAP operating margin expanded to roughly 31%, while ARR reached $1.853 billion, up 11% year-over-year, and dollar-based net retention held at 107%. The company also achieved full-year GAAP profitability for the first time. The numbers point to a business that is still growing while showing real operating leverage.

Analysts Generally Give the Stock a “Hold”

Of the 21 analysts covering PATH, 3 rate it a Buy, 17 rate it a Hold, and 1 rates it a Strong Sell. The overwhelming Hold consensus reflects cautious optimism rather than full-blown conviction. Needham bucked the trend by raising its rating to Buy after the Q4 results, citing enterprise AI adoption tailwinds. D.A. Davidson and Wells Fargo held firm at Neutral and Equal-Weight, citing valuation and growth outlook concerns.

The Stock Trades Like the Business is Broken

PATH trades at $10.39, well below the analyst consensus target of $13.80. The stock is sitting near its 52-week low of $9.46 and far from its $19.84 high, which shows how much sentiment has reset. At roughly 14x forward earnings, the market is pricing in a meaningful slowdown.

The drawdown has been sharp. PATH is down 36.55% year-to-date, compared to just a 0.86% decline for the S&P 500, a gap of roughly 36 percentage points. That level of underperformance is hard to ignore. Over the past year, the stock is only up 5.37%, which reinforces the idea that momentum has faded.

Even so, institutional ownership still sits at 80.57%, which suggests larger investors have not fully walked away from the story despite the recent pressure.

Only Worth the Risk If the Guidance Story Changes

The bull case strengthens if fiscal 2027 guidance shows ARR growth reaccelerating back toward the mid-teens and management can prove that agentic AI adoption is translating into net new ARR. The profitability inflection looks real, the platform integrations are credible, and the stock still trades well below analyst consensus targets. A Reddit post in r/stocks summed up the tone: “Added to PATH after the drop, but keeping expectations low.” That kind of measured optimism feels representative of where sentiment sits today.

The bear case comes into focus if cautious FY2027 guidance marks the start of a longer deceleration cycle. Short interest at 15.59% of float is a meaningful overhang, the legal situation has not fully cleared, and CEO selling at much higher prices removes an important confidence signal. The market has repeatedly sold off the stock even after earnings beats, which suggests the issue is expectations around growth rather than execution. If ARR growth slips into the low single digits, the current valuation leaves little room for error. The gap between price and target may be real, but so is the skepticism reflected in the 17 Hold ratings from analysts who follow the company closely.