Most investors chase the same megacap names. But sometimes the most interesting setups are hiding in plain sight: a micro-cap media company quietly becoming a digital business, a uniform rental operator working through a real turnaround, and a specialty chemicals company with a much healthier balance sheet. Here are three stocks worth watching, ranked from interesting to most compelling.

#3: Townsquare Media

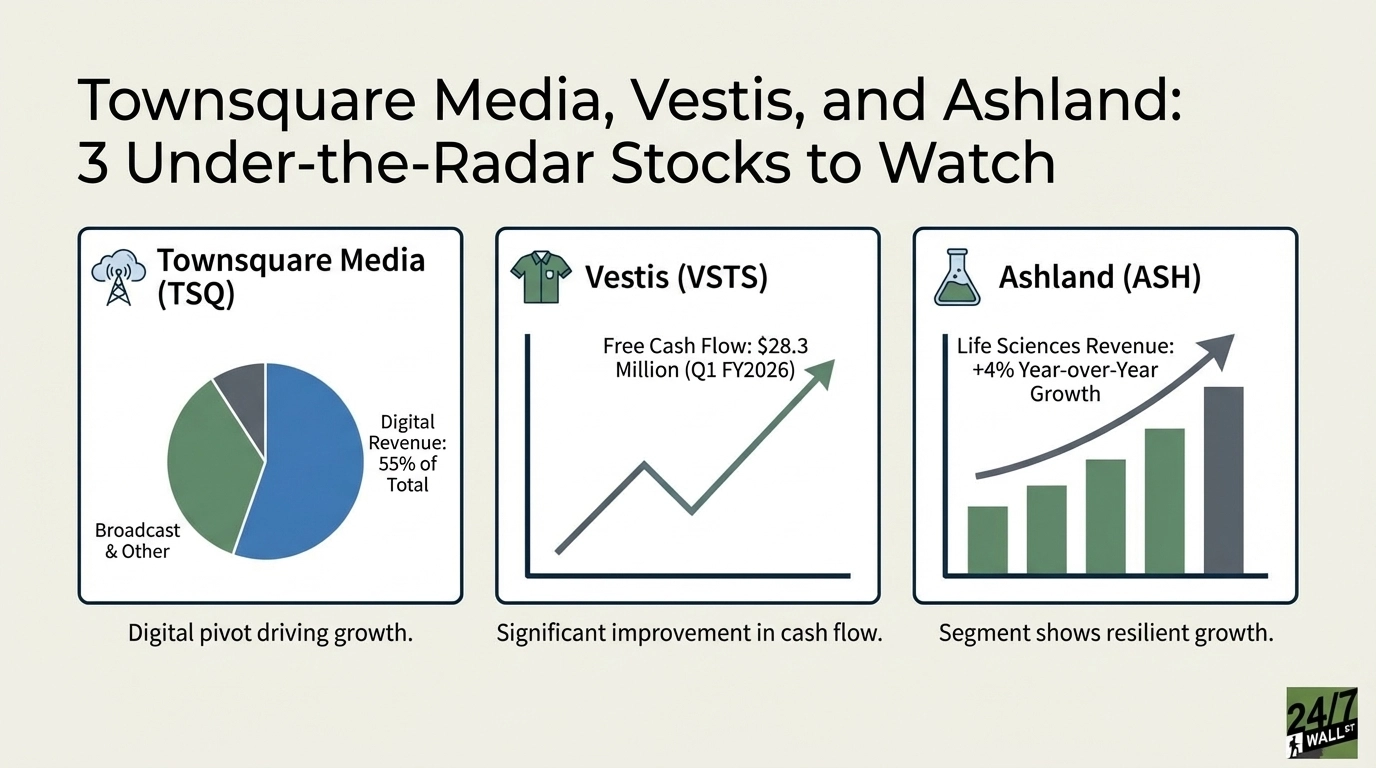

Townsquare Media (NYSE:TSQ) is a local radio and digital marketing company operating in small and mid-sized U.S. markets, which insulates it somewhat from competition facing big-city broadcasters.

The headline numbers from Q3 2025 look messy. Revenue fell 7.4% year-over-year to $106.76 million, but strip out political advertising, which collapsed 95.4% due to election cycle comparisons, and the real decline was -4.5%. The EPS beat was genuine: $0.05 against a $0.03 estimate.

The real story is the digital pivot. Digital now represents 55% of total net revenue, and the Townsquare Interactive subscription segment delivered segment profit growth of 21.1% year-over-year in Q3. Direct digital advertising revenue grew +7% year-over-year in the same period. Broadcast is still declining but becoming a smaller piece each quarter.

The risks are real. Net leverage sits at 4.74x and shareholders’ equity is negative at -$33.96 million. Cash on hand is thin at $3.2 million. That said, management has been buying. On January 14, CEO Bill Wilson and the full board made a coordinated purchase at $5.41 per share, with Wilson acquiring over 700,000 units in total. The stock trades at $7.17, up 43.45% year-to-date. Analysts carry a consensus target of $13.50, and the trailing P/E is just 6x. The ~10.8% dividend yield is eye-catching but carries leverage risk.

#2: Vestis

Vestis (NYSE:VSTS) rents uniforms and workplace supplies to businesses across the U.S. and Canada. Spun out of Aramark in late 2023, it has had a rough run since, but the trajectory is finally turning.

The turnaround thesis rests on one number: free cash flow jumped to $28.3 million in Q1 FY2026, compared to nearly nothing in the prior year period. Operating cash flow was $37.69 million. Adjusted EBITDA grew sequentially from $64.66 million in Q4 2025 to $70.38 million in Q1 FY2026. Plant productivity improved 7% year-over-year, on-time deliveries were up 3%, and customer complaints fell 12%.

CEO Jim Barber laid out the path clearly: “We have made meaningful progress advancing our operational excellence priorities. During the quarter we saw significant improvements in plant productivity, on-time deliveries and customer satisfaction.” The company is targeting at least $75 million in annual cost savings by end of FY2026.

Challenges remain. Revenue fell 3% year-over-year to $663.39 million and net leverage remains elevated at 4.83x. Business retention at 91.2% is still declining. Analysts lifted their consensus price target roughly 29% after the Q1 FY2026 print, but the stock at $7.53 is still down 31% over the past year. This is a show-me story, not a done deal.

#1: Ashland

Ashland (NYSE:ASH | ASH Price Prediction) makes specialty chemicals used in pharmaceuticals, personal care, and industrial applications. Pricing power and formulation expertise create durable competitive advantages.

The most recent quarter showed a company regaining its footing. Life Sciences revenue grew 4% year-over-year to $139 million, with segment adjusted EBITDA climbing 11% to $31 million. Free cash flow came in at $111 million in Ashland’s seasonally weakest quarter, boosted by a $103 million tax refund from the Nutraceuticals divestiture. Cash on hand stood at $304 million.

CEO Guillermo Novo narrowed FY2026 adjusted EBITDA guidance to $400 million to $420 million and reiterated targets for double-digit-plus adjusted EPS growth. The manufacturing optimization program is expected to deliver roughly $30 million in savings in FY2026 alone from a $90 million total program.

Headwinds exist. Specialty Additives revenue fell 11% and a Calvert City facility outage dragged results by roughly $10 million. Asbestos litigation reserves stand at $372 million. The stock has pulled back sharply, trading at $50.98, down 12.53% year-to-date, well below the analyst consensus target of $68. The forward P/E sits at roughly 13x.

The Bottom Line

All three companies are navigating real operational challenges. Townsquare trades at a low valuation with recent insider purchases and a digital segment growing faster than headline revenue suggests. Vestis is showing improving cash flow metrics and management is executing against a stated cost savings plan. Ashland has a strong balance sheet, a growing Life Sciences segment, narrowed guidance, and a forward P/E of roughly 13x. Its consensus analyst price target stands at $68, compared to its current price of $50.98, down 12.53% year-to-date.