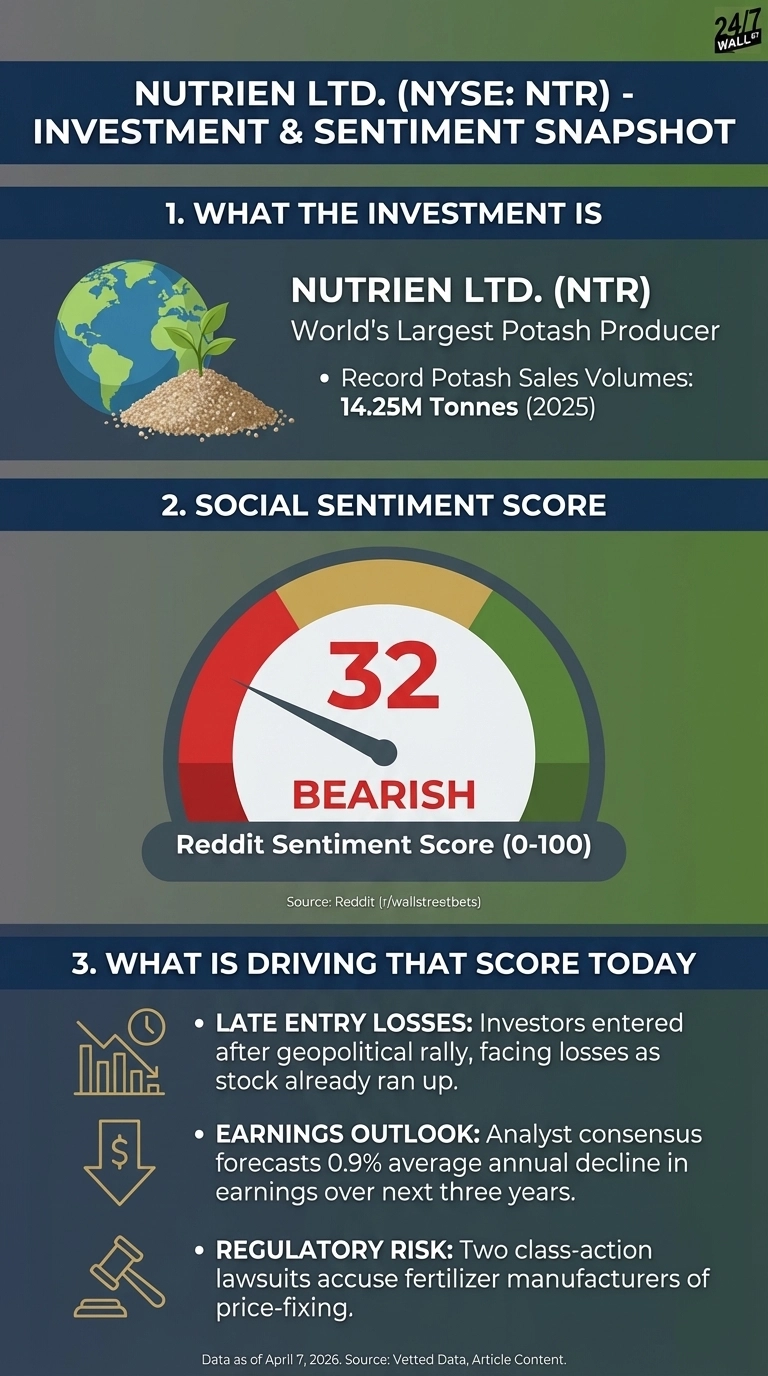

Operating across four different segments in the agricultural space, Nutrien Ltd. (NYSE:NTR | NTR Price Prediction) shares are up roughly 23% year-to-date and have surged nearly 62% over the past year, yet Reddit’s social sentiment score is bearish at 32 out of 100. Nutrien posted record potash sales volumes of 14.25 million tonnes in 2025 and grew full-year free cash flow to $2.002 billion, yet Q4 adjusted EPS came in at $0.83, missing the consensus of $0.92. The earnings miss coincided with a geopolitical supply shock that lifted fertilizer prices, and Reddit sentiment remains bearish at 32 out of 100 despite share price gains.

Operating across four different segments in the agricultural space,v shares have shown resilience with a 52-week high near $85.36, yet retail sentiment on platforms like Reddit remains cautious. Nutrien posted record potash sales volumes of 14.25 million tonnes in 2025 and maintained a steady free cash flow of approximately $2 billion, yet Q4 adjusted EPS came in at $0.83, missing the consensus of $0.92. The earnings miss coincided with a geopolitical supply shock that lifted fertilizer prices, but some retail observers remain skeptical of the stock’s cyclical nature despite strong institutional confidence.

A Jefferies upgrade on March 12 raised the price target to $96, citing fertilizer price spikes driven by Middle East supply disruptions. UBS downgraded Nutrien to Sell on March 26, flagging valuation concerns and expected potash price declines. The consensus analyst target sits near $78, close to where shares trade today, leaving little spread between the current price and the consensus target unless the geopolitical premium holds.

The Reddit Thread Driving NTR Bearish Sentiment

Reddit discussion around Nutrien is thin. All qualified mentions originate from r/wallstreetbets, with just one dominant post generating activity across multiple time windows on April 7, 2026. That post, titled “Options saved my portfolio” by user u/Totalets, describes a loss on NTR options.

Options saved my portfolio

by u/Totalets in wallstreetbets

The author describes “recently thought it’d be a good idea to bet on fertilizers (NTR) even though it already ran up since the start of the war, which dropped my account to near zero”. The post reflects the dominant sentiment across observation windows, where retail investors weigh a score of 32 against three primary headwinds:

- The stock already ran sharply on geopolitical news, leaving late-entry retail traders facing significant losses as momentum from the Iran conflict began to stall.

- Analyst consensus forecasts a 0.8% average annual decline in earnings over the next three years, severely limiting the case for further multiple expansion in a cyclical peak.

- A federal class-action lawsuit filed in Colorado accuses Nutrien and its peers of price-fixing NPK fertilizers, adding a DOJ-linked regulatory tail risk not yet reflected in price targets.

Potash Pricing and the Credibility Gap

Global potash demand is projected at 74-77 million tonnes in 2026, marking the fourth consecutive year of growth. CEO Ken Seitz noted on the earnings call that low channel inventories in major markets are supporting shipments, pointing to a balanced rather than oversupplied market. Potash benchmark prices are approximately 13% higher compared to 12 months ago, with Brazil spot prices currently near $375 per tonne.

The phosphate strategic review, expected to progress through 2026, adds near-term uncertainty as the company seeks to optimize its portfolio. Nutrien’s forward P/E of roughly 12x, against a trailing P/E of 16x, implies the market expects a steady earnings recovery ahead. The geopolitical premium in fertilizer prices and the outcome of the phosphate strategic review will both factor into whether that earnings gap closes by mid-2026.