SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) screens as a potential buy candidate at $16 for long-term, growth-oriented investors who can stomach volatility. The stock has fallen nearly 50% from its 2025 peak, driven by a contested short-seller report and broad market rotation, yet the underlying business compounds at a rate the current price no longer reflects.

SoFi operates a one-stop digital financial services platform offering banking, lending, investing, and financial planning through a single app. It holds a national bank charter, providing deposit funding access and regulatory standing pure fintechs lack. The company operates three segments: Lending, Financial Services, and Technology Platform (Galileo), which powers 128.5 million global accounts for third-party clients. After years of losses, SoFi has delivered nine consecutive profitable quarters.

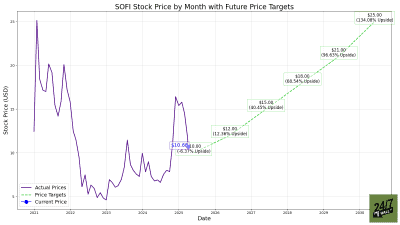

The stock entered 2026 at $26.18 and has fallen 38% year-to-date, closing at $16.22 as of the most recent session. The decline accelerated after Muddy Waters published a short report in mid-March alleging accounting irregularities.

The Business Is Compounding. The Price Has Not.

Q4 2025 earnings were exceptional. SoFi posted adjusted EPS of $0.13 against a $0.11 estimate, beating estimates, while revenue crossed $1 billion in a single quarter for the first time. Financial Services revenue grew 78% year-over-year and contribution profit doubled. Full-year 2025 revenue reached $3.613 billion, up 38% year-over-year. Fee-based revenue hit a record $443 million in Q4, up 53% year-over-year, reducing reliance on rate-sensitive net interest income.

Forward growth is compelling at this price. Management guided for approximately $4.655 billion in adjusted net revenue for 2026, implying roughly 30% growth, alongside adjusted EPS of approximately $0.60. The medium-term framework calls for adjusted EPS compounded annual growth of 38% to 42% through 2028. At $16, the stock trades at roughly 27x forward earnings, a steep discount to the trailing multiple and reasonable for a profitable fintech growing EPS at that rate. CEO Anthony Noto purchased 544,748 shares of common stock in March 2026, including a direct market purchase at $17.32 per share during peak selling pressure.

SoFi became the first nationally chartered bank to launch consumer crypto trading and issued the SoFiUSD stablecoin, positioning itself ahead of most traditional banks in a crypto-friendly regulatory environment. With total deposits of $37.5 billion and a capital ratio of 22.9% against a regulatory minimum of 10.5%, the balance sheet is solid.

Short-Seller Report and Rising Charge-Offs Create Real Uncertainty

Muddy Waters alleged SoFi approximately $312 million of unrecorded debt from a JPMorgan loan deal and inflated EBITDA. Carson Block compared SoFi’s accounting to Enron. Even if unfounded, reputational damage and regulatory scrutiny are real costs. Analysts at Barclays and KBW trimmed price targets following the report. Short-seller pressure on a high-beta, thinly profitable bank matters.

Credit quality deserves scrutiny. The personal loan annualized charge-off rate rose to 2.80% in Q4, up from 2.60% sequentially, with the estimated all-in net charge-off rate closer to 4.4%. Management attributes this to portfolio seasoning rather than deterioration, but in a slowing macro environment with unemployment potentially rising toward 4.5% to 5.0%, prime borrowers can miss payments. Net interest margin compressed 19 basis points year-over-year to 5.72%, and the Technology Platform segment saw accounts fall 23% year-over-year due to a large client departure.

The stock carries a beta of 2.25, amplifying both rallies and selloffs. With macro uncertainty elevated and tariff risks unresolved, broader market weakness will hit SOFI disproportionately. The stock’s five-year return of -9% reminds investors this name has repeatedly disappointed those who paid up for growth that took longer to materialize.

Fundamentals Are Strong. The Short Report Needs Resolution.

The hold case is straightforward: fundamentals are intact, but the Muddy Waters overhang remains unresolved. SoFi called the report factually inaccurate and misleading and announced potential legal action. A denial is not a rebuttal. Investors await a detailed accounting response. Until Q1 2026 earnings arrive with substantive management disclosures, uncertainty persists.

Nine consecutive quarters of GAAP profitability, a Rule of 40 score of 68% in Q4, and a cross-buy rate of 40% of new products from existing members point to a working flywheel. Investors holding through this period await accounting noise to clear, not abandoning a broken thesis.

The catalyst is Q1 2026 earnings on April 29. If SoFi meets guided $1.04 billion in Q1 adjusted net revenue and $0.12 in adjusted EPS while providing substantive rebuttal to Muddy Waters, the thesis strengthens materially. If credit deteriorates beyond seasoning or accounting allegations gain regulatory traction, the risk-reward shifts unfavorably.

At $16, SoFi Screens as a Buy Candidate

At $16, SoFi screens as a buy candidate. The stock trades at roughly 27x forward earnings, a modest forward P/E for a company growing revenue at 30% annually and expanding EBITDA margins toward 34%. CEO insider buying at higher prices signals conviction. The Muddy Waters report explains the discount and may also represent the opportunity for investors with a longer horizon.

Invalidating factors: regulatory confirmation of unrecorded debt, sustained charge-off deterioration beyond seasoning, or a meaningful Q1 miss would warrant reassessment. Watch deposit growth and net interest margin trajectory closely.

This is high-beta with real short pressure and rising charge-offs. Size positions accordingly. But at $16, with tangible book value of $8.9 billion, a 30% revenue growth trajectory, and Q1 earnings weeks away, risk-reward tilts toward buyers who can wait out the noise.