Fintech stocks entered 2026 riding high on hopes for lower rates and a digital finance boom. Then reality hit: persistent inflation worries, a Fed rate pause, and sector-wide jitters sent the KBW Nasdaq Financial Technology Index down about 11% year-to-date.

SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) got hammered hardest. Shares opened 2026 near $26 after peaking at $32.73 in November, but now trade at $15.85 per share. That’s a 51.57% drop from the 52-week high and a 41% year-to-date plunge.

This price just doesn’t make any sense. The market is overlooking a company that just posted its first $1 billion revenue quarter and launched a game-changing enterprise platform. Here’s why SoFi stock is a buy despite the market disconnect.

A Brutal Slide

SoFi didn’t stumble on weak numbers. The selloff stemmed from broader fintech fatigue. Personal-loan charge-offs ticked up to 2.80% in Q4, a figure that spooked some after earlier rate-cut optimism faded. Valuation compression followed: the stock had run hard on growth expectations, and when macro headlines turned cautious, investors rotated out. No single earnings miss triggered it — in fact, Q4 results crushed estimates — but the sector traded at a discount to growth potential.

That said, the drop created an entry point. Shares now sit below half their peak while the business is accelerating. Believe it or not, this reset happened after SoFi delivered record results and unveiled its biggest strategic leap yet.

Recent Expansions Make the Business Far More Attractive

SoFi’s earnings painted a picture of scale and diversification most fintechs envy. Adjusted net revenue hit a record $1.013 billion, up 37% year-over-year — the first time quarterly revenue crossed $1 billion. GAAP net revenue reached $1.025 billion, up 40%. Adjusted EBITDA climbed 60% to $318 million for a 31% margin. GAAP net income totaled $174 million, delivering a 17% margin and marked the ninth straight profitable quarter.

Members grew 35% to 13.7 million, while products rose 37% to 20.2 million, helping fee-based revenue jump 53% to $443 million. Full-year adjusted revenue reached $3.6 billion, up 38%, and management’s 2026 guidance calls for adjusted net revenue of roughly $4.655 billion (30% growth), adjusted EBITDA of $1.6 billion (34% margin), and adjusted EPS around $0.60. Q1 2026 targets already point to $1.04 billion in adjusted revenue (35% growth).

Yesterday, though, SoFi made an announcement that should change how the market looks at the company. The fintech launched Big Business Banking, which allows enterprises to now manage fiat USD deposits, crypto assets, and the proprietary SoFiUSD stablecoin — all inside one FDIC-insured, nationally chartered bank with direct Fed access. Real-time, 24/7 API-driven payments, and instant fiat-to-crypto conversions via SoFiUSD mint-and-burn sit on Solana and other chains. Initial partners include Cumberland, Bullish (NYSE:BLSH), BitGo (NYSE:BTGO)(custody), Fireblocks, Wintermute, Galaxy (NASDAQ:GLXY), Jupiter, Mesh Payments, and Mastercard (NYSE:MA).

This isn’t a side project. It extends SoFi’s December SoFiUSD launch (the first stablecoin from a U.S. national bank) into institutional territory. Legacy banks run 9-to-5. Pure crypto players lack bank rails. SoFi now offers both under one regulated roof — creating sticky enterprise deposits, transaction fees, and stablecoin seigniorage on its balance sheet.

Why the Stock Pressure at $15 Makes No Sense

Smart investors compare numbers, not headlines. SoFi trades at roughly 41x trailing earnings and about 19x estimates. That sits above some consumer-finance peers like Regional Management (NYSE:RM) (7x P/E) but reflects 30%+ revenue growth and 38% to 42% medium-term EPS growth guidance — metrics peers such as Upstart (NASDAQ:UPST)and Affirm (NASDAQ:AFRM) have struggled to match consistently.

The enterprise platform adds high-margin, 24/7 revenue streams that reduce reliance on consumer lending. Deposit growth from corporate clients should lower funding costs. Network effects from partners accelerate SoFiUSD adoption and platform usage.

In short, SoFi evolved from a retail disruptor into a full-spectrum player bridging TradFi and crypto — at precisely the moment institutional demand surges.

Naturally, risks remain. Charge-off rates bear watching, and macro shifts could slow originations. Execution on Big Business Banking will take time. Yet the numbers show a company that grew members 35%, revenue 37%, and EBITDA 60% while turning consistently profitable. The market’s doubts look priced in at $15.

Key Takeaway

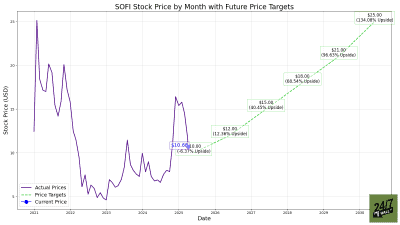

When all is said and done, SoFi at $15 offers a rare combination: proven execution, accelerating diversification, consistent profitability, and a first-mover regulatory edge in enterprise crypto banking. Analysts’ consensus price target sits at $25.91 per share, implying 63% upside. No one can predict the exact bottom, but the data say the business has never looked stronger.

For patient retail investors, this reset isn’t a warning — it’s an invitation. Consider buying now and adding on further weakness. I might not go all-in, but SoFi Technologies looks like an opportunity too good to pass up, making it worth having at least some skin in the game.