Wednesday night’s Fast Money panel on CNBC turned into a referendum on what an AI hyperscaler is supposed to look like in 2026. Amazon (NASDAQ:AMZN | AMZN Price Prediction) and Microsoft (NASDAQ:MSFT) reported on the same evening, and the panel zeroed in on one number that splits the bull case from the bear case: capital expenditures.

Amazon: Spend Now, Answer Questions Later

Amazon’s CapEx surged 77% year-over-year, with Q1 spending hitting $44.203 billion. The cash impact was severe. Free cash flow collapsed to $1.2 billion from $26 billion year-over-year, and long-term debt swelled to $119.1 billion from $65.6 billion.

However, the operational story held. Operating margins beat expectations at 13.1% vs. Street’s 11.7%, AWS grew 28% YoY (its fastest growth in 15 quarters), and Amazon’s chips business cleared a $20 billion annual revenue run rate. The panel host noted Amazon trades “about as cheap as you can” at 11 to 12 times EBITDA, adding, “I don’t know why the stock is lower here.”

One caller offered a thesis worth chewing on: Amazon “is the only of the Mag Seven, the only one that has a blue-collar workforce that has logistics business that could seriously benefit from AI efficiencies.” On the enterprise side, Amazon Copilot seats grew to 20 million from 15 million. You can read the full release on the company’s 8-K filing.

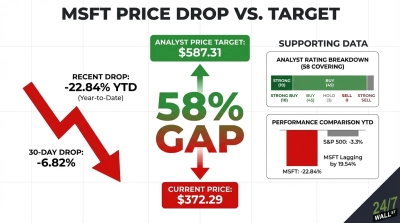

Microsoft: A Quiet Step Back

Microsoft went the other direction. CapEx dropped to $31.9 billion, “lower than what analysts were anticipating and down from last quarter, fueling speculation that Microsoft is curbing to Wall Street pressure.” Azure still posted 40% growth (39% constant currency), the AI run rate hit $37 billion, up 123%, and commercial RPO nearly doubled to $627 billion.

The complication is structural. Microsoft’s OpenAI relationship is in question following termination of their exclusive agreement, which had been a centerpiece of the Azure AI thesis. Investors took notice. MSFT shares fell 5.52% on Thursday, while Polymarket traders pegged a same-day decline at 0.988 probability.

Which Strategy Wins?

The panel framed it cleanly. Amazon is absorbing margin and balance-sheet pain to lock in compute supremacy, with landmark deals including approximately 2 GW of Trainium capacity for OpenAI and up to 5 GW for Anthropic. Microsoft is signaling discipline, returning capital, and protecting its 19.99% operating income growth.

The shared worry voiced on the panel was that eventually “it’ll just be a little too much debt” restricting traditional shareholder returns. For now, retail sentiment is leaning Amazon’s way, with Reddit’s bullish reading climbing to 60 by Thursday morning. Whether that conviction survives the next four quarters of free cash flow compression is the trade.