Tank warfare defined World War II. German blitzkrieg tactics showed how armored columns could slice through lines when supported by air power and infantry. Today, drones play that same disruptive role in Ukraine and the Middle East. Low-cost, expendable systems overwhelm expensive defenses, deliver precision strikes, and provide persistent intelligence. Battle-tested swarms and loitering munitions have already shifted tactics. Investors wonder which companies will supply the next decisive edge.

Not all drones are created equal. Large Reaper-style platforms offer long-endurance surveillance but come with high costs and vulnerability. Textron (NYSE:TXT | TXT Price Prediction) and others produce medium systems for specific missions. The real action for retail investors sits in lightweight, attritable, and disposable categories — systems cheap enough to lose in volume but smart enough to matter. AeroVironment (NASDAQ:AVAV), Kratos Defense & Security Solutions (NASDAQ:KTOS), and Ondas (NASDAQ:ONDS) each target slices of this market, so let’s see which one be worth leading your portfolio

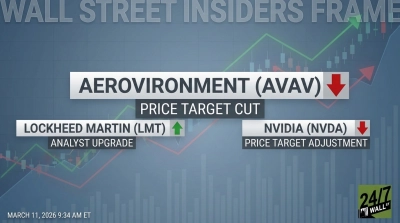

AeroVironment (AVAV)

AeroVironment specializes in small, man-portable loitering munitions like the Switchblade 300, 400, and 600 families. These tube-launched “kamikaze” drones loiter, identify targets, and strike with precision. The Switchblade 300 handles personnel and light vehicles; the 600 tackles armor. Recent variants like the 400 bridge the gap for medium-range anti-armor work.

The dronemaker has delivered strong growth. Fiscal 2025 revenue reached $821 million, up 14.5% year-over-year. Trailing 12 months results through early 2026 hit roughly $1.61 billion after the BlueHalo acquisition boosted scale. Fiscal Q3 revenue jumped 143% to $408 million, though the company later adjusted full-year guidance downward to $1.85 billion to $1.95 billion amid funding delays. AeroVironment’s funded backlog stood at $1.1 billion.

The stock’s performance has reflected defense momentum. AeroVironment’s shares rose about 57% in 2025 and showed solid YTD gains into 2026 before recent volatility caused it to shed half its valuation from last year’s high. A pricey valuation and acquisition-related losses created market worry, but organic demand for Switchblades remains robust.

Is AeroVironment a buy? Yes, for investors comfortable with premium pricing on proven, battle-tested systems. Contracts and backlog support continued expansion, though margins and integration costs bear watching. Smart investors see the Switchblade ecosystem as a moat in the disposable drone wave.

Kratos Defense & Security Solutions (KTOS)

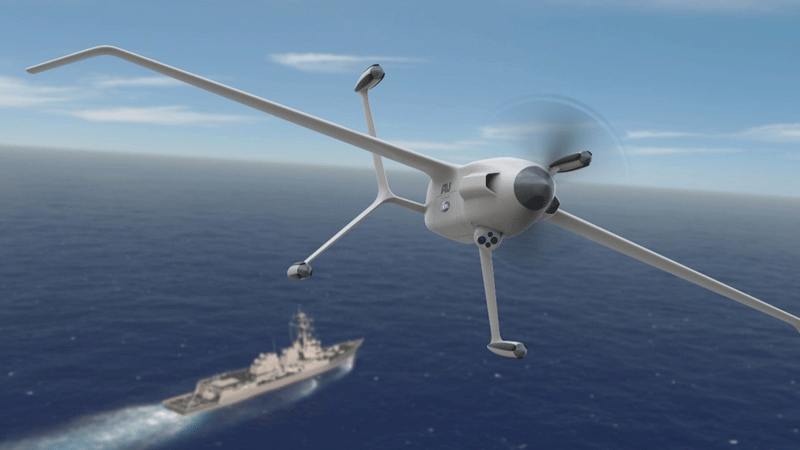

Kratos Defense & Security Solutions focuses on higher-performance, attritable platforms, or systems that are low-cost, reusable, and replaceable. Its XQ-58 Valkyrie serves as a stealthy collaborative combat aircraft — essentially a loyal wingman for F-35s and other manned jets. Runway-independent, high-subsonic, and capable of carrying weapons, Valkyrie targets mass production at lower costs than traditional fighters.

The defense contractor reported 2025 revenue of $1.35 billion, up 18.5%. Q4 revenue grew 21.9% to $345.1 million with 20% organic growth. The Unmanned Systems segment, which includes the Valkyrie, posted 12.1% organic growth in the quarter. Management guided fiscal 2026 revenue to $1.595 billion to $1.675 billion, while its book-to-bill ratio remained healthy at 1.3:1 in Q4.

Shares trade around $62 with a market cap near $11.6 billion. Kratos has delivered positive returns year to date, and benefits from broader unmanned spending tailwinds. Valuation appears stretched on GAAP earnings, but growth in Valkyrie and related programs provides visibility.

Is the dronemaker a buy? It suits investors betting on collaborative “loyal wingman” concepts scaling with next-gen air combat. Organic growth and Marine Corps momentum add additional tailwinds, though execution on fixed-price contracts bears monitoring. Still, Kratos offers a compelling mix of tactical drones and broader defense exposure.

Ondas Holdings (ONDS)

Ondas Holdings brings a different flavor — autonomous “drone-in-a-box” systems, counter-UAS, and integrated robotics via subsidiaries like American Robotics, Airobotics, and others. Its Optimus platforms enable persistent surveillance and operations with minimal human intervention. The company also addresses counter-drone needs critical in contested airspace.

Growth exploded in 2025, with revenue reaching $50.7 million, up roughly 605% year-over-year. Ondas raised 2026 guidance significantly to at least $375 million as Q1 forecasts point to $38 million to $40 million. Its recent Mistral acquisition could expand gains further as it now has a direct pipeline into prime defense contractor wins. Ondas’ own order book spans counter-UAS, border protection, and critical infrastructure.

Its market cap sits around $5 billion with shares near $10, up over 1,200% over the past year, as Ondas delivered on both execution and hype. However, it remains unprofitable with a high cash burn that has been offset by recent capital raises. Its valuation multiples underscore the growth expectations the market has.

Is Ondas a buy? Yes, but it’s probably best-suited for aggressive growth investors who can tolerate volatility and execution risk. The trajectory from a tiny base to hundreds of millions in revenue is exciting if deployments scale, but competition and profitability timelines remain open questions. It offers pure-play exposure to autonomous infrastructure.