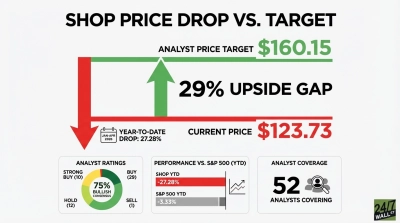

Shopify (NASDAQ:SHOP | SHOP Price Prediction) currently trades around $125.83, while Wall Street’s average price target sits at $159.70. This means Wall Street analysts, on average, see about 27% upside for the stock today. Shopify powers commerce for millions of merchants, from small businesses to large brands like SKIMS and Supreme. Its platform spans storefronts, payments, point-of-sale, capital, and increasingly AI-driven tools. The stock has long traded as a high-multiple bet on e-commerce growth, which makes the recent drawdown notable. The stock has sold off sharply, but the underlying business continues to grow at a strong pace.

A 31% Drawdown Built on AI Spending Fears, Not Broken Fundamentals

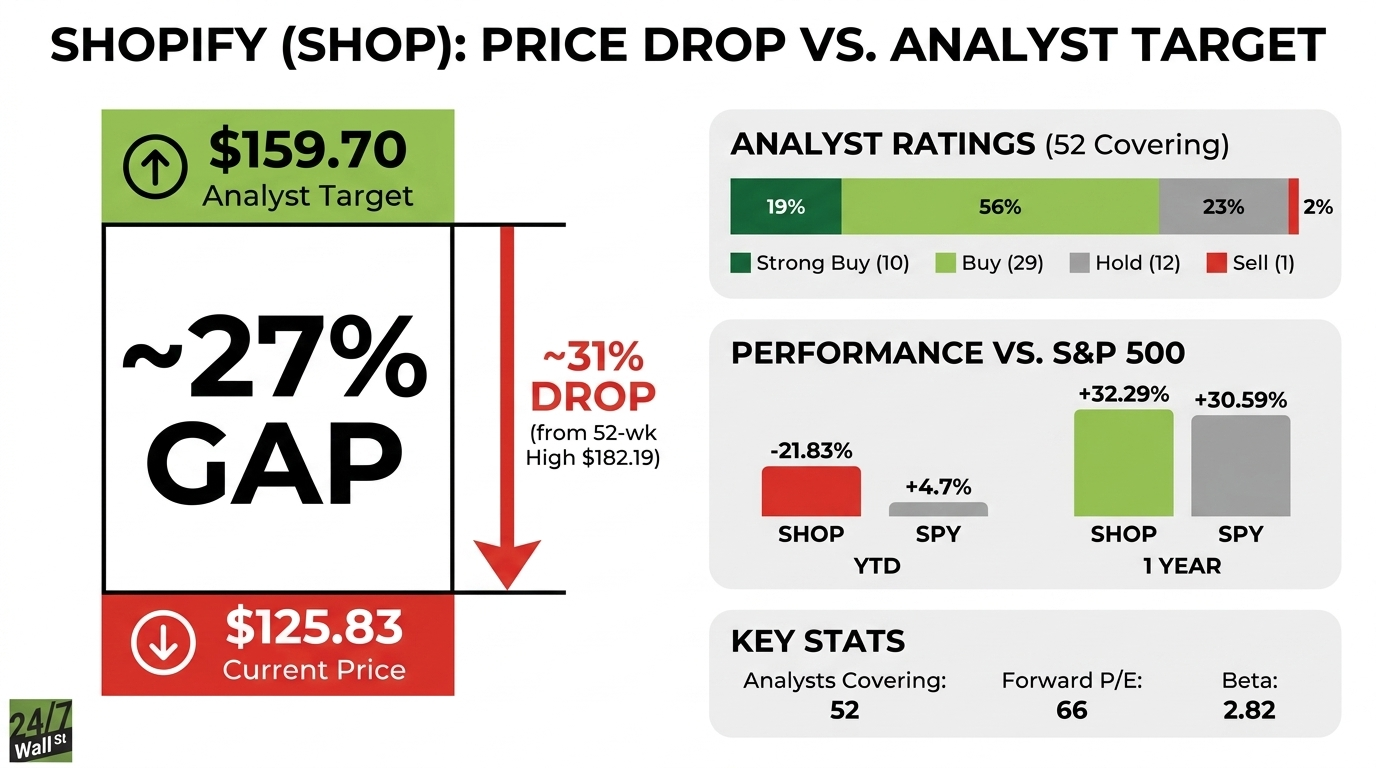

Shopify is down roughly 31% from its 52-week high of $182.19, a decline largely driven by profitability fears, with revenue actually beating consensus.

The Q4 results were solid on the surface. Revenue rose 30.6% to $3.67 billion, beating expectations. However, net income declined 42.5%, raising concerns about profitability. Guidance added to the pressure, with management indicating operating expenses would run at 37% to 38% of revenue, with free cash flow margins in the low-to-mid teens as AI investment ramps.

The selloff was company-specific, layered onto a broader rotation away from software names. Technical signals piled on, with one March note flagging a potential “Death Cross” as the 50-day moving average converged on the 200-day. Investors also priced in the risk that agentic commerce and AI-driven disruption could cannibalize Shopify’s storefront business.

Why Analysts Remain Bullish

Despite the pullback, analysts have largely maintained their stance. Shopify’s Q4 GMV increased 31% to $123.8 billion, Shop Pay GMV rose 62%, and B2B GMV nearly doubled. International revenue grew 36%, and full-year free cash flow reached $2.01 billion. The bull thesis hinges on Shopify becoming the infrastructure layer for AI-native commerce. Recent product launches embed merchants into ChatGPT, Microsoft Copilot, and Google Search AI.

JPMorgan reiterated Overweight with a $150 target, projecting 32% YoY GMV growth and 29% gross profit growth for Q1 2026, and RBC Capital carries a $170 target. President Harley Finkelstein framed the AI push as measured, telling investors the company is “leveraging our decades of experience to ensure that AI is carefully implemented”. The company’s $2 billion buyback program also reinforces management’s confidence.

Of the 52 analysts covering the stock, 10 rate it a Strong Buy, 29 a Buy, 12 a Hold, 1 a Sell, and none a Strong Sell.

What the Tape Actually Shows

Shopify trades at $125.83 against a consensus target of $159.70, implying roughly 27% upside if the sell-side is right. Coverage is deep, with 52 firms tracking the name and 75% rating it bullish.

Year-to-date, SHOP is down 21.83% while the S&P 500 is up 4.7%, stark relative underperformance. Over a full year, SHOP returned 32.29% versus 30.59% for the index, a reminder that the recent drawdown started from an elevated base.

Valuation remains the friction point. The stock trades at a forward P/E of 66 on EPS of $0.94, with a beta of 2.82. Analyst targets are one data point among many.

Where I Land on Shopify Here

The bull case rests on Shopify growing into its investments. If AI-driven features deepen merchant engagement, GMV continues compounding above 30%, and margins stabilize, the business can justify the current multiple and work its way back toward the $159 target range.

But, you can’t forget that at roughly 66x forward earnings, the stock is priced for strong execution. If AI spending weighs on margins longer than expected, or growth starts to normalize, that multiple is likely to compress before fundamentals fully catch up.

My view is that Shopify is still growing at a strong pace, but you’re paying a premium for it. Even after the sell-off, the upside for the stock may only materialize if Shopify proves it can balance growth and profitability over the next few quarters.