Microsoft (NASDAQ:MSFT | MSFT Price Prediction) trades around $408, while Wall Street’s consensus target sits at $576.42, meaning analysts see a significant 41% upside for the stock today. Microsoft is one of the world’s most valuable companies, with a $3.16 trillion market cap and a software empire that leans heavily on Azure cloud and its OpenAI partnership. The stock’s performance today is largely tied to the market’s interpretation of the company’s AI infrastructure spending, as we’re seeing the market reward companies seeing good returns from capex spending while punishing companies that appear to be losing money on infrastructure spending.

Why Microsoft’s Strong Q3 Earnings Still Led to a Selloff

Microsoft stock fell roughly 4% after third-quarter earnings despite reporting results that largely reinforced the bull case. Revenue rose 18% to $82.9 billion, while operating income increased 20% to $38.4 billion. Net income reached $31.8 billion, and EPS came in at $4.27, all ahead of expectations. Growth remains concentrated in cloud and AI. Microsoft Cloud revenue reached $54.5 billion, up 29%, while Intelligent Cloud revenue grew 30% to $34.7 billion. Azure and other cloud services increased 40%, showing continued strength in enterprise demand.

The AI business is scaling quickly. Management said it has surpassed a $37 billion annual revenue run rate, growing 123% year over year. At the same time, backlog remains strong. Commercial remaining performance obligation rose 99% to $627 billion, providing visibility into future revenue. The takeaway is that the demand Microsoft is seeing is keeping pace with the company’s AI investment.

Why 55 of 58 Analysts Still Rate the Stock a Buy

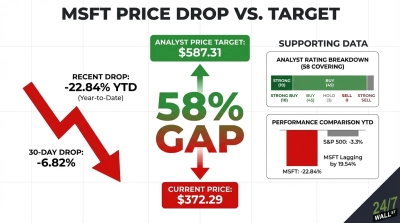

Despite the earlier selloff, analyst sentiment has not changed. Out of 58 firms, 55 rate the stock a Buy or Strong Buy, with just 3 Holds and no Sell ratings. The thesis centers on visibility and scale. A nearly $630 billion backlog, 40% Azure growth, and a rapidly expanding AI business suggest Microsoft is still early in the monetization cycle.

CEO Satya Nadella told investors “We are only at the beginning phases of AI diffusion and already Microsoft has built an AI business that is larger than some of our biggest franchises.”

The OpenAI restructuring sweetens the math. Microsoft holds a ~27% stake valued at roughly $135 billion, and OpenAI committed an incremental $250 billion in Azure services, with IP rights extended through 2032. Analysts are watching Q3 FY26 Azure guidance of 37-38%, which would confirm AI demand is absorbing the capex.

Where I Land on Microsoft Here

Microsoft remains below previous highs despite exhibiting strong fundamentals. The stock is down about 14% year-to-date while the S&P 500 is up modestly. At current levels, a move to the analyst consensus target price of $576 implies roughly 41% upside, which is pretty significant for a Magnificent 7 stock. The stock trades at about 22x forward earnings, which is a pretty reasonable multiple for a business growing earnings at nearly 20% annually.

At current levels, Microsoft looks undervalued and might warrant a closer look. The bull case rests on Azure sustaining growth around 40%, the $627 billion backlog converting into revenue, and the AI business continuing to scale from its $37 billion run rate. If those trends hold, the current CapEx cycle looks justified, and the path toward analyst targets becomes easier to underwrite.

Meanwhile, the bear case rests on capital intensity. Microsoft is spending heavily to build out AI infrastructure, and if monetization lags, that could pressure free cash flow and margins. At the same time, competition from Google and Amazon could limit pricing power before the investment fully pays back.