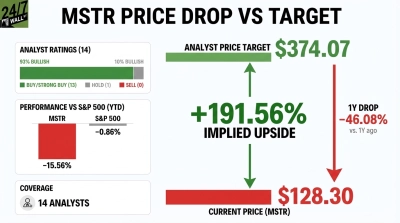

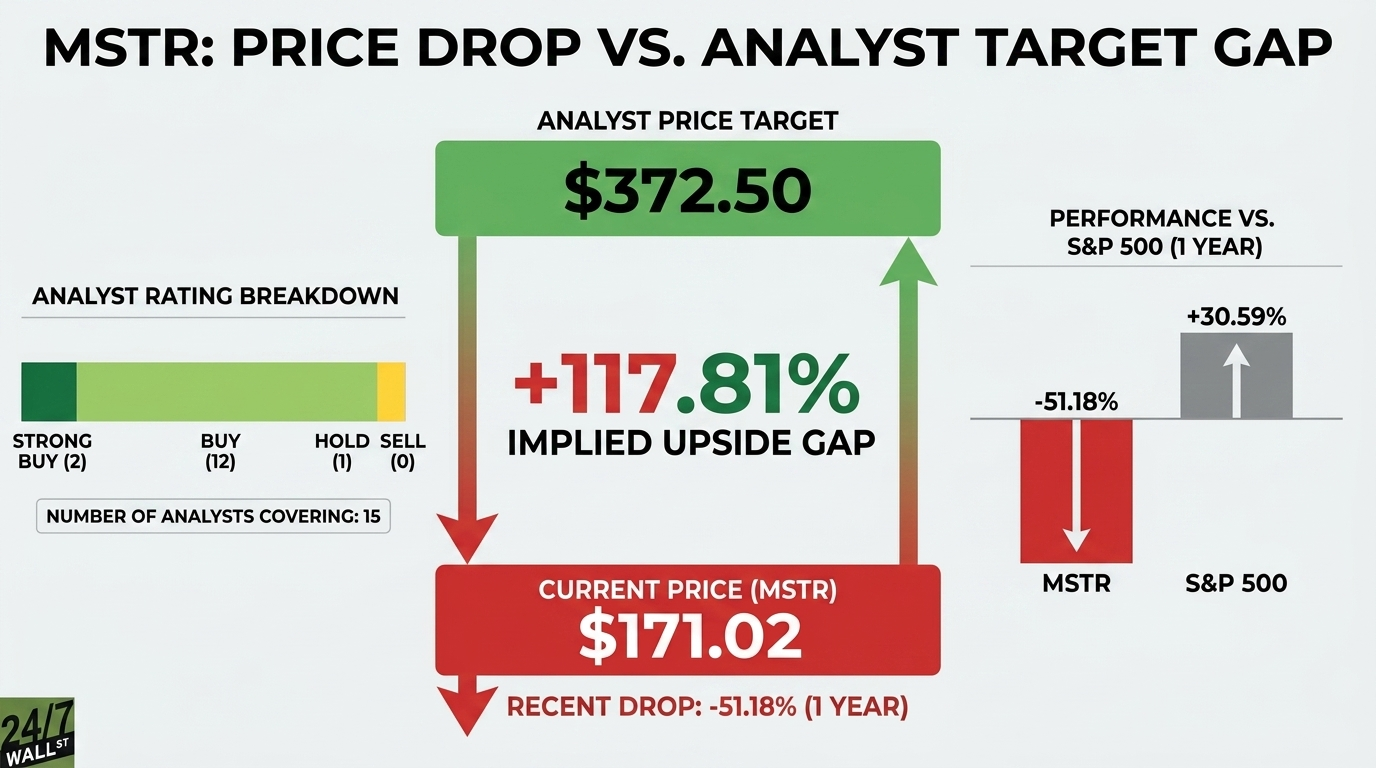

MicroStrategy (NASDAQ:MSTR | MSTR Price Prediction), now operating as Strategy, currently trades at $171.02 against an average analyst price target of $372.50, implying analysts see roughly 118% upside.

Strategy is the world’s largest corporate bitcoin treasury, holding roughly 713,502 BTC as of early February and approximately 762,099 BTC by late March after a $2.54 billion, 34,164 BTC purchase. Wall Street covers the name as a leveraged proxy on Bitcoin. The gap between the stock’s current price and analysts’ price target implies the stock trades well below the value sell-side analysts see.

A Bitcoin-Driven Crash That Halved the Stock

Strategy has lost 51.18% over the past year, a violent drawdown from a 52-week high of $457.22. The trigger was bitcoin’s slide and the accounting that now flows through the income statement. Under ASU 2023-08 fair value rules, Q4 2025 produced a $17.44 billion unrealized loss on digital assets, which dropped reported EPS to -$42.93 against a consensus of -$15.66, a miss of 174.14%. Net loss for the quarter was $12.44 billion.

Bitcoin itself sits around $77,474, down 11.46% year to date and 18.16% over twelve months. Layer in dilution from $25.3 billion raised in 2025 alone, perpetual preferred dividend obligations, and persistent debates around MSCI index exclusion, and it’s no wonder the stock is down 50% in the past year.

Why Analysts Remain Bullish

With implied upside above 100%, the stock deserves a closer look. Of the 15 analysts covering Strategy, 2 rate it a Strong Buy, 12 a Buy, 1 a Hold, and zero a Sell. Recent analyst actions have leaned toward reiterations and upgrades after the April 22 bitcoin acquisition, with Clear Street earlier reiterating Buy while trimming its target.

The bull case rests on three factors. First is Strategy’s capital-raising ability, which continues to fund Bitcoin accumulation at scale. Second is growth in Bitcoin per share, the key metric analysts use to value the business despite GAAP volatility. Third is the underlying software segment, where subscription revenue grew over 60% year over year.

The forward-looking catalyst analysts watch is Bitcoin moving back above $100,000. CEO Phong Le has publicly anchored a $1 million seven-year bitcoin target, and Polymarket assigns a 64.5% probability to Strategy holding 1M+ BTC by year-end 2026. Margin call risk is priced at just 8.5%. Targets, of course, are projections, not guarantees.

Where I Land on Strategy

The bull case rests on Bitcoin recovering and Strategy continuing to compound its holdings through capital markets activity. The bear case rests on structural risks, such as continued dilution, competition from spot Bitcoin ETFs, and the possibility that the premium to net asset value will compress further.