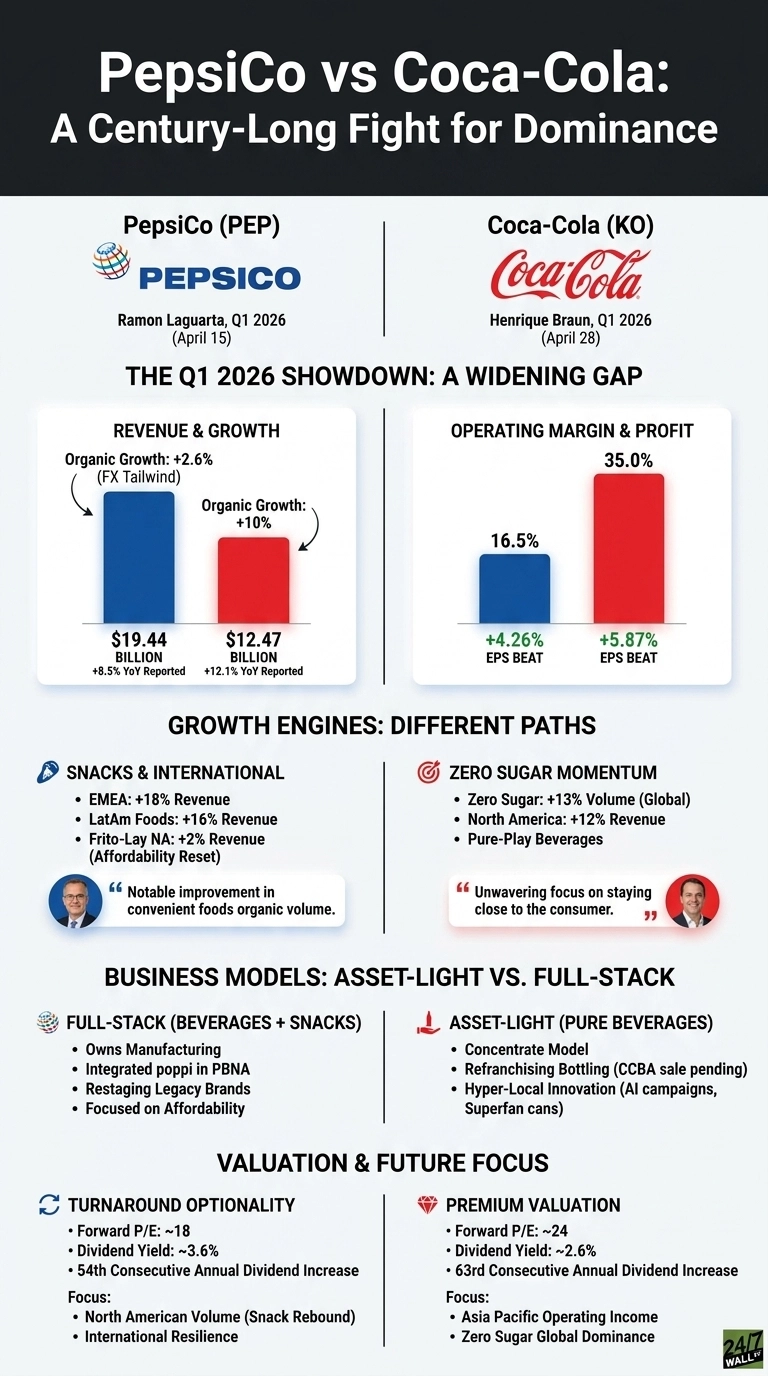

PepsiCo (NASDAQ: PEP | PEP Price Prediction) and Coca-Cola (NYSE: KO) just delivered first quarter results that expose a widening gap between the two beverage giants. Coke leaned on Zero Sugar momentum and a near pure-play concentrate model. Pepsi leaned on snacks, international resilience, and an affordability reset to nudge North American volumes back to life.

Zero Sugar Lifts Coke. Snacks and EMEA Lift Pepsi.

Coca-Cola posted $12.47 billion in revenue, up 12.07% year over year, with organic growth of 10%. That is a remarkably clean number for a company this size. The standout: Coca-Cola Zero Sugar grew volume 13% across every geographic segment, a rare uniform result that suggests the brand has crossed into genuine global staple status. EPS of $0.86 beat the $0.81 estimate, the fourth consecutive beat.

Pepsi delivered core EPS of $1.61 against a $1.54 estimate on revenue of $19.44 billion, up 8.5%. Organic revenue grew only 2.6%, with a 3.4 percentage point currency tailwind doing real work.

The bright spots sat outside North America: EMEA revenue jumped 18% and LatAm Foods rose 16%, while Frito-Lay North America inched up just 2%. CEO Ramon Laguarta called out “a notable improvement in convenient foods organic volume”, an early but fragile sign the snack reset is working.

| Business Driver | Coca-Cola | PepsiCo |

| Main Growth Engine | Zero Sugar, Sprite, premium packs | EMEA, LatAm Foods, poppi |

| Operating Margin | 35.0% | 16.5% |

| North America Revenue Growth | +12% | PFNA +2%, PBNA +9% |

Asset-Light Coke vs. Full-Stack Pepsi

The structural divergence is sharper than the headline numbers. Coke is doubling down on its concentrate model, refranchising bottling and pursuing the pending sale of Coca-Cola Beverages Africa expected to close in H2 2026.

New CEO Henrique Braun said the quarter reflects “our unwavering focus on staying close to the consumer, executing locally and managing complexity.” Innovation is hyper-local: an AI-enabled connected-packaging campaign in China, a Premier League 500ml “Superfan” can in the UK, and ultra-lightweight bottles in South Africa and India.

Pepsi is doing the opposite. It owns its snack manufacturing, integrated poppi into PBNA, and is restaging legacy brands while running affordability promotions to win back lower-income shoppers. That keeps margins capped near 17% but gives Pepsi two engines instead of one. The snack business is a moat Coke simply does not have.

The Next Test Is North American Volume

The next test is whether Frito-Lay’s volume green shoots translate into pricing power without resorting to deeper discounts. For Coke, the question is Asia Pacific, where comparable currency-neutral operating income fell 17% on costs and mix, and whether 8% to 9% comparable EPS growth guidance survives a stronger dollar.

BofA has raised the firm’s price target to $90 from $88 and keeps a Buy rating on the shares after the company delivered “impressive” 10% organic sales growth in Q1.

Pepsi’s 54th consecutive annual dividend increase at a 3.59% yield is a real cushion if the turnaround stalls.

Valuation Setup: Coke Premium, Pepsi Turnaround Optionality

On valuation, Coke trades at a 24 forward P/E after a 12.61% year-to-date run, supported by expanding margins and a Zero Sugar franchise growing in every region.

Pepsi screens cheaper for turnaround-oriented investors at a forward P/E near 18, with a fatter dividend and clear international momentum that translate to asymmetric upside if Frito-Lay volumes stick. The key signpost for Pepsi remains whether next quarter confirms the snack rebound is durable.