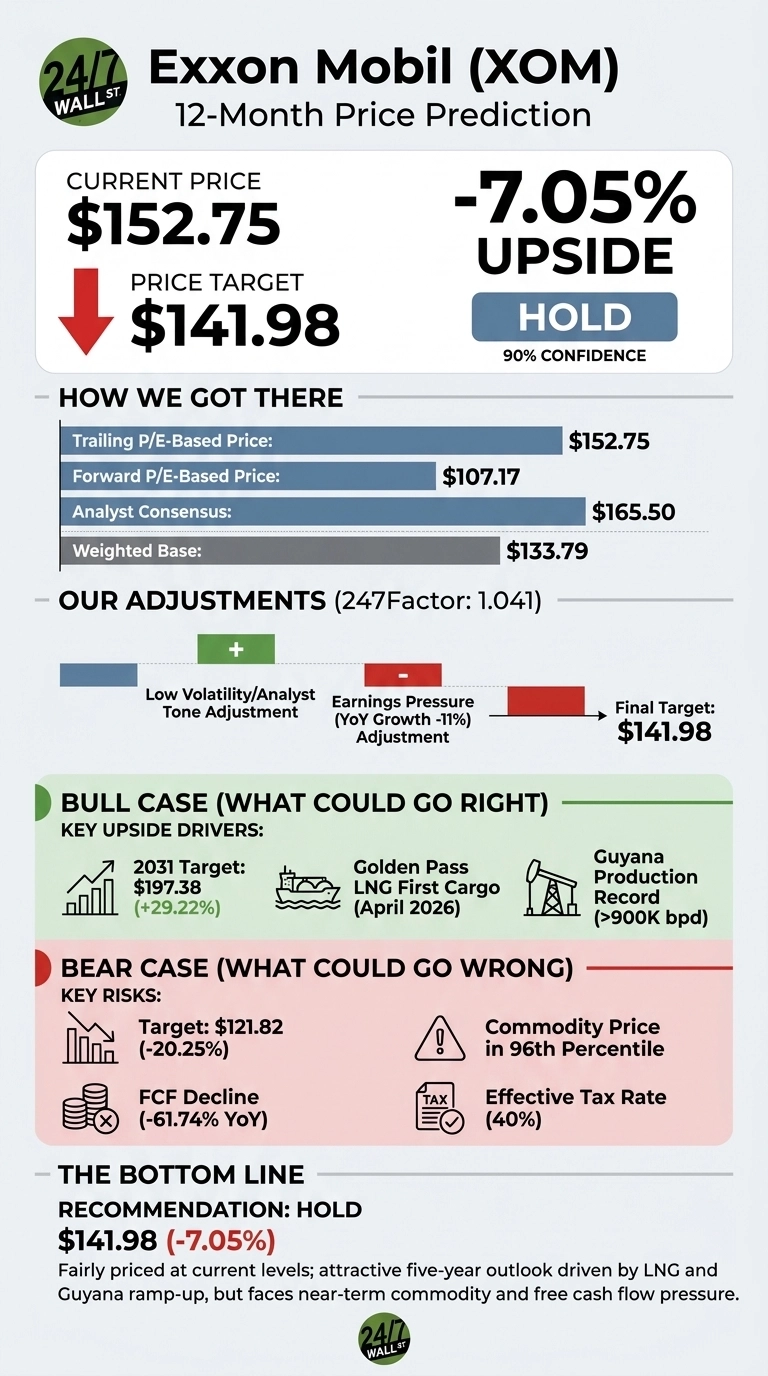

Exxon Mobil (NYSE:XOM | XOM Price Prediction) trades fairly priced at current levels. The 24/7 Wall St. price target points to $141.98 over the next 12 months, modestly below the current quote of $152.75. Our recommendation is hold, with a confidence level of 90%. The longer-dated bull case, however, points to $197.38 by 2031, driven by LNG and Guyana ramp-up.

| Metric | Value |

|---|---|

| Current Price | $152.75 |

| 24/7 Wall St. Price Target | $141.98 |

| Upside/Downside | -7.05% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

The price target sits below current trading levels. Two catalysts could prove us wrong: Golden Pass LNG Train 1, which loaded its first cargo in April 2026, and Guyana production already running at over 900,000 gross barrels per day. The full bull case below explains why shareholders may have the better hand.

A $100 Oil Market Meets Cleaner Earnings

XOM rose 49.36% over 12 months and 27.8% year to date, helped by WTI crude pushing to $99.89 after an early-April spike to $114.58.

Q1 2026 results, released May 1, 2026, delivered adjusted EPS of $1.16 against a $1.01 consensus, a 15.15% beat and the fourth straight quarter topping estimates. Revenue of $85.14 billion just missed by 0.18%. Reported net income of $4.18 billion looked weak, but underlying earnings rose to $8.77 billion from $7.58 billion a year ago after stripping a $3.88 billion mark-to-market timing hit and $706 million in Middle East disruption losses.

The Case for $197 by 2031

Exxon delivered 10 of 10 key 2025 projects, adding roughly $3 billion in earnings power, hit record upstream production of 4.7 million boed last year, and has logged $15.6 billion in cumulative structural cost savings since 2019 against a $20 billion target by 2030.

CEO Darren Woods called this a “durable platform to grow earnings, cash flow, and shareholder value through 2030 and beyond.” Capital returns are massive: $20 billion of buybacks planned for 2026, with $4.9 billion already executed in Q1, plus 43 consecutive years of dividend growth. Wall Street consensus target of $165.50 already implies upside. Our internal bull scenario points to $197.38 if LNG, Guyana, and Permian volumes compound as planned.

The Risks Worth Watching

Commodity exposure is the core bear case. WTI sits in the 96th percentile of its 12-month range, a level that historically does not hold. Free cash flow fell 61.74% year over year in Q1 to $2.70 billion, and the effective tax rate jumped to 40%. Insider activity skews to net selling.

The 24/7 Wall St. price target of $141.98 implies oil normalizes lower, putting the bear scenario at $121.82. Bulls counter that FCF compression reflects timing on derivatives and rising CapEx tied to high-return Guyana and Permian projects. Underlying earnings are growing.

Fair Value Today, Better Entry on a Pullback

Our price target of $141.98 with hold and 90% confidence reflects what the math says: XOM is fairly priced when oil is hot and the stock is six points off a 52-week high. The setup looks more attractive if WTI holds above $90 and Golden Pass ramps to full commercial operations on schedule. Risk rises materially if crude rolls back into the $60s and the FCF line keeps compressing. The five-year setup is attractive. The entry price today looks full.

Exxon Mobil Price Projection 2026-2030

Assuming current strategy executes and oil normalizes into the $70 to $85 range:

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $141.98 |

| 2027 | $148.50 |

| 2028 | $158.75 |

| 2029 | $168.40 |

| 2030 | $178.20 |

Significant upside or downside could result from sustained $100 oil, an OPEC+ shock, or accelerated electrification.