SoFi Technologies (NASDAQ:SOFI | SOFI Price Prediction) has whipsawed investors over the past six months, riding from the low teens to a 52-week high of $32.73 before sliding back to the high teens. With Q1 2026 earnings on deck, our proprietary model points to a stock that has already done most of the work of finding fair value.

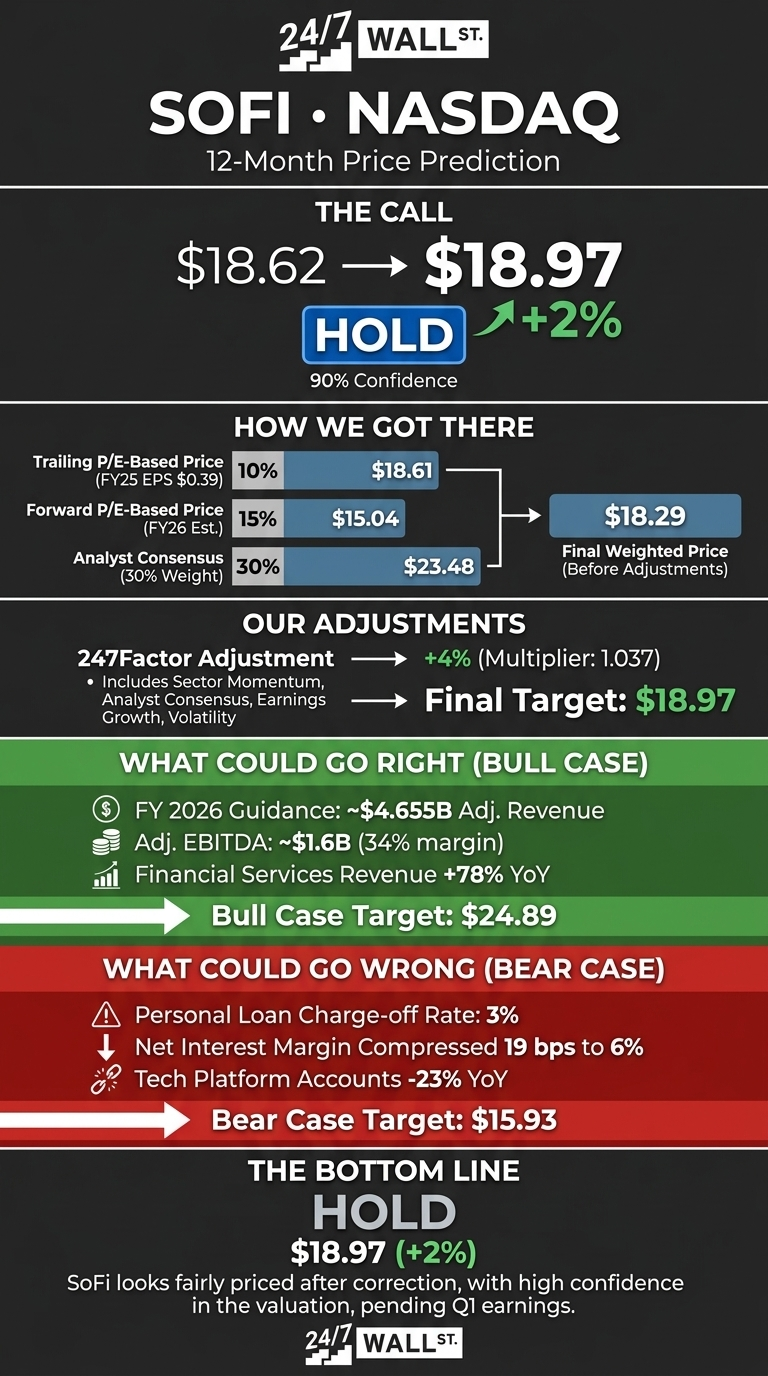

Our 24/7 Wall St. price target for SoFi is $18.97, which sits roughly 2% above the current price of $18.62. The recommendation is hold, with a confidence reading of 90%. In plain English: SoFi looks fairly priced after the recent correction, and the next leg likely waits on Q1 results.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $18.59 |

| 24/7 Wall St. Price Target | $18.97 |

| Upside | 2% |

| Signal | HOLD |

| Confidence | 90% |

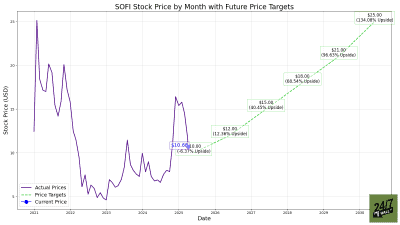

From $32 to $18: How SoFi Reset This Spring

The chart tells the story. SoFi has fallen 28% year-to-date after peaking near $27 last September, yet still sits up 46% over the trailing year and 23% over the past month as buyers stepped in below $16.

The fundamentals behind that volatility are strong. Q4 2025 produced $1.025 billion in revenue, SoFi’s first billion-dollar quarter, with adjusted EPS of $0.13 beating the $0.11 consensus. Members hit 13.7 million, up 35% YoY, and FY 2025 revenue grew 38% to $3.61 billion. The drag has been credit-related: the personal loan charge-off rate ticked up to 3%, and net interest margin compressed 19 bps YoY to 6%.

The Case for $25+

Bulls have a clean thesis. Management guided FY 2026 to $4.65 billion in adjusted revenue, $1.6 billion adjusted EBITDA at a 34% margin, and $0.60 in adjusted EPS. Medium-term EPS CAGR is targeted at 38% to 42% through 2028.

Financial Services revenue grew 78% YoY in Q4, fee-based revenue jumped 53%, and the Loan Platform Business is now running at a $15 billion annualized origination pace.

New crypto, stablecoin, and remittance rails widen the optionality. Wall Street’s average target of $23.48 reflects that view, with 8 buy-side ratings. Our internal bull case puts SoFi at $24.89 within 12 months if execution holds.

What Could Go Wrong

The bear case rests on credit and multiple compression. The personal loan charge-off rate moving from 3% to 3% sequentially deserves attention, asset yields fell 74 bps YoY, and Technology Platform accounts dropped 23% YoY as a large client transitions off.

Bulls would counter that the platform decline is one client-specific, charge-offs remain below 2024 levels, and SoFi is investing through cycle to capture share. Still, at a P/E near 48x and beta of 2.25, any FY 2026 stumble could pull SoFi to our bear case of $15.93.

Holding Through the Earnings Report

The data points to a fairly valued setup here with high conviction. The 24/7 Wall St. price target of $18.97 sits within a percent of where the stock trades, and the 90% confidence reflects how cleanly the data converges.

I would get more constructive on a clean Q1 2026 earnings report that hits the $0.12 adjusted EPS bar with credit metrics stable. I would step back if charge-offs climb above 3% or 2026 guidance gets trimmed. Polymarket traders are nearly split at 48% odds of an earnings beat, which is the right way to think about the setup.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $18.97 |

| 2027 | $19.65 |

| 2028 | $20.35 |

| 2029 | $21.08 |

| 2030 | $21.83 |

These projections extend the model’s base-case 4% annualized return path, which lands SoFi at $22.18 by April 2031. Significant upside or downside could come from credit normalization, Galileo client wins, or interest-rate shifts.